Swap rates and market sentiment have played a role in reversing an established trend.

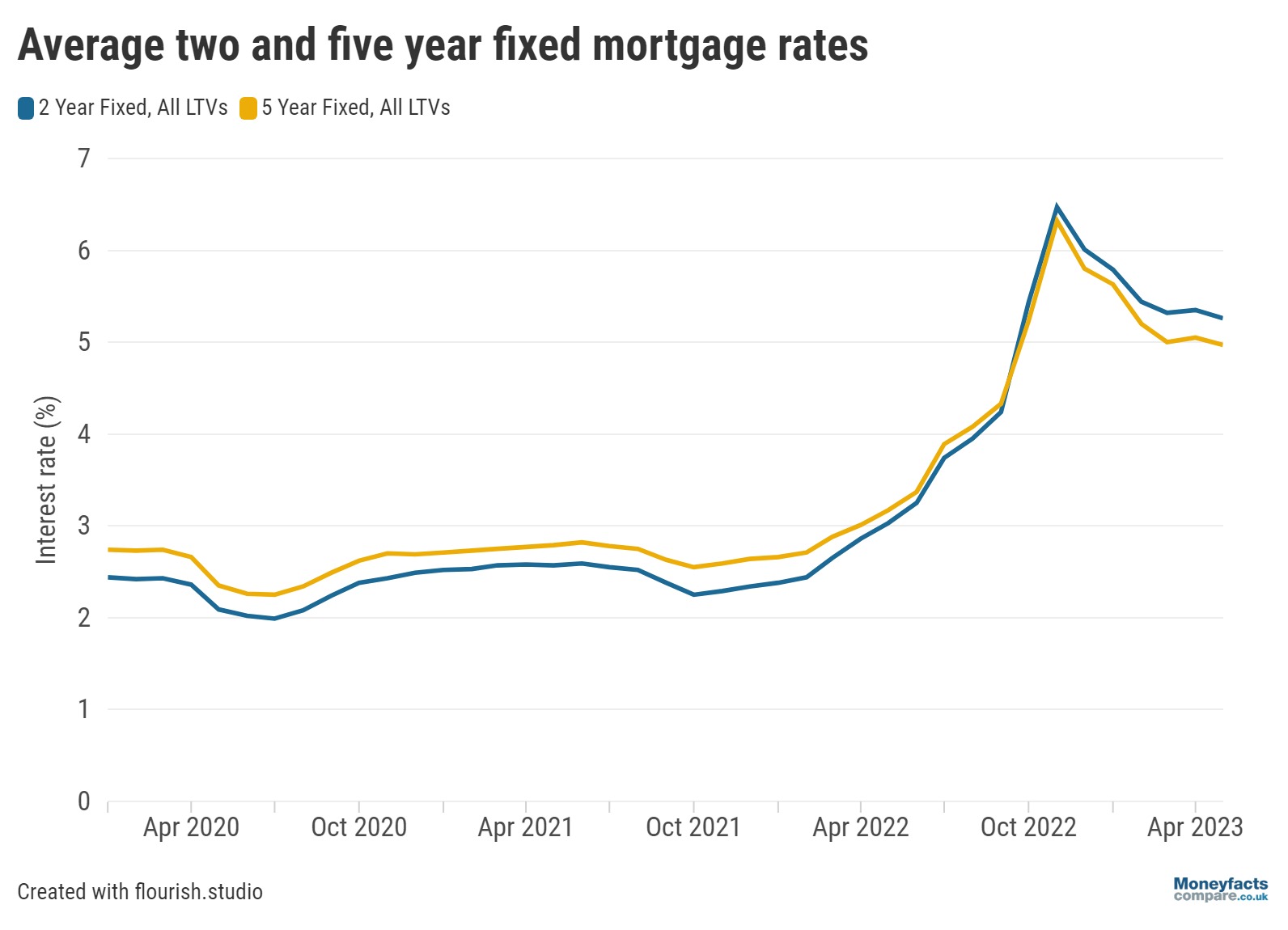

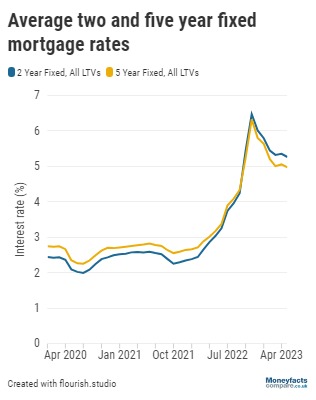

Traditionally, a two-year fixed rate mortgage would offer a lower rate than its five year fixed counterpart.

This made sense.

Fixing for a longer period carries more uncertainty for your lender. As opposed to a shorter term, amongst other things, there is more chance over a longer mortgage that you could lose access to your regular income and therefore default.

It also made sense for borrowers. Fixing your mortgage over a longer period provides more certainty over your monthly repayments, and this relief comes at a price.

But for the past eight consecutive months this historical relationship has reversed, according to Moneyfacts data.

The average five year fixed rate is now cheaper than its two year fixed counterpart (See below).

So why has this happened, and will it likely revert soon?

It is no coincidence that the average two year fixed deal became more expensive than the five year fixed deal in October 2022 – the month following the mini-Budget.

As documented on our website, the statement from the former Chancellor Kwasi Kwarteng created uncertainty in the market and this fed into the price of fixed rate mortgages.

More specifically, the mini-Budget created uncertainty for swap rates and the market’s outlook on interest rates.

Most retail banks make money through net interest. A detailed overview on how this works can be found in a previous article.

Swap rates play a key role in keeping retail banks profitable.

To illustrate, consider the scenario where you wish to lock into a fixed rate mortgage with your lender. For the purposes of this example, your bank may need to make use of the money deposited in its easy access accounts or current accounts to fund your mortgage.

Now, if the Bank of England (BoE) were to increase interest rates the bank might have to increase its variable savings rates to remain competitive. Since you are paying a fixed rate of income, this increase will eat into the bank’s profits.

In order to address this challenge, banks can trade – or swap – their variable rate cash flow for a fixed rate payment on a secondary market. Traders on this secondary market includes other banks, pension companies and financial institutions which have their own goals and objectives.

Fixed rate payments are determined on market sentiment, or where traders believe the BoE’s base rate may fluctuate in the future.

Banks can then use this sentiment to help determine the pricing of their fixed rate mortgages.

Despite the effects of the mini-Budget, the gap between the average two and five year fixed deal was already closing.

In January 2020, before the outbreak of the COVID-19 pandemic, the difference between the average two and five year fixed mortgage sat at 0.30 percentage points.

By last September this had shrunk to 0.09 percentage points.

As for this month, the average two year fixed deal stands at 5.26% while the average five year fixed deal is priced at 4.97%.

Both these figures have fallen from last month, with the average five year fixed deal now below 5% for the first time since September.

While there are other reasons for this trend, swap rates and the market’s outlook on the BoE’s base rate have played a role in engineering this inverse relationship.

Currently, two year fixed swap rates are higher than their five year fixed equivalents. This perhaps reflects the market’s view that interest rates will remain elevated for the next two years while in the following three years they are more likely to fall.

If two-year fixed rate mortgages are to become cheaper the market’s outlook on interest rates will need to change too.

Inflation, which still sits in double digits, will need to fall quickly and beat the BoE’s expectations to give these mortgages some reprieve.

But this won’t be the only variable at play, and a significant reduction in two year fixed rates will depend upon other factors, such as lender appetite in the market.

Make sure to visit Moneyfactscompare.co.uk for breaking stories on inflation and how it affects your personal finances.

All of our newsletters are available free by email to all Moneyfactscompare.co.uk users.

Send me Weekend Moneyfactscompare, Savers Friend, and Companies Friend.

Information is correct as of the date of publication (shown at the top of this article). Any products featured may be withdrawn by their provider or changed at any time. Links to third parties on this page are paid for by the third party. You can find out more about the individual products by visiting their site. Moneyfactscompare.co.uk will receive a small payment if you use their services after you click through to their site. All information is subject to change without notice. Please check all terms before making any decisions. This information is intended solely to provide guidance and is not financial advice. Moneyfacts will not be liable for any loss arising from your use or reliance on this information. If you are in any doubt, Moneyfacts recommends you obtain independent financial advice.

Moneyfactscompare.co.uk will never contact you by phone to sell you any financial product. Any calls like this are not from Moneyfacts. Emails sent by Moneyfactscompare.co.uk will always be from news@moneyfacts-news.co.uk. Be ScamSmart.

Moneyfactscompare.co.uk will never contact you by phone to sell you any financial product. Any calls like this are not from Moneyfacts. Emails sent by Moneyfactscompare.co.uk will always be from news@moneyfacts-news.co.uk. Be ScamSmart.

Moneyfactscompare.co.uk will never contact you by phone to sell you any financial product. Any calls like this are not from Moneyfacts. Emails sent by Moneyfactscompare.co.uk will always be from news@moneyfacts-news.co.uk. Be ScamSmart.

Moneyfactscompare.co.uk will never contact you by phone to sell you any financial product. Any calls like this are not from Moneyfacts. Emails sent by Moneyfactscompare.co.uk will always be from news@moneyfacts-news.co.uk. Be ScamSmart.

Moneyfactscompare.co.uk will never contact you by phone to sell you any financial product. Any calls like this are not from Moneyfacts. Emails sent by Moneyfactscompare.co.uk will always be from news@moneyfacts-news.co.uk. Be ScamSmart.

Moneyfactscompare.co.uk will never contact you by phone to sell you any financial product. Any calls like this are not from Moneyfacts. Emails sent by Moneyfactscompare.co.uk will always be from news@moneyfacts-news.co.uk. Be ScamSmart.