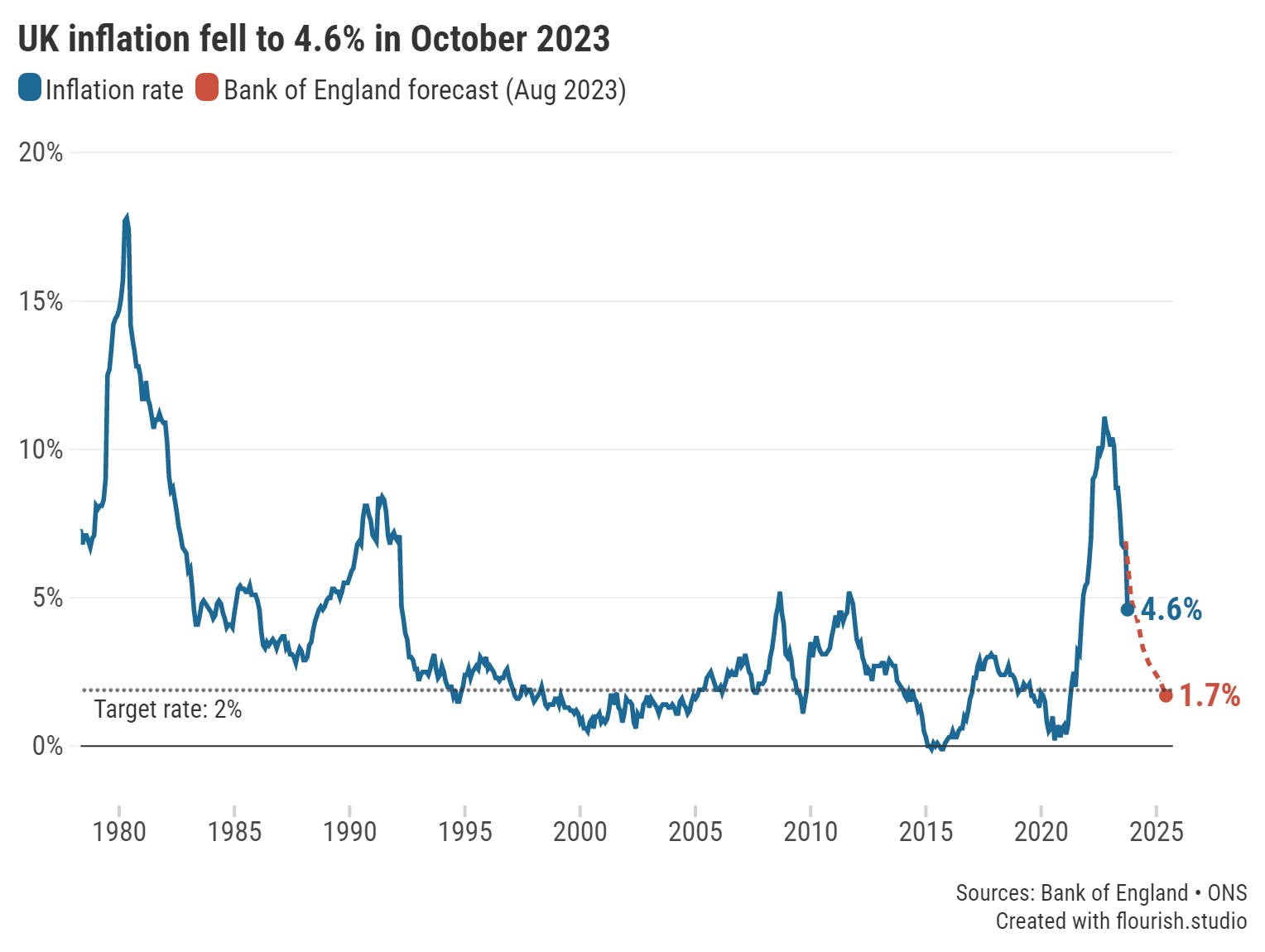

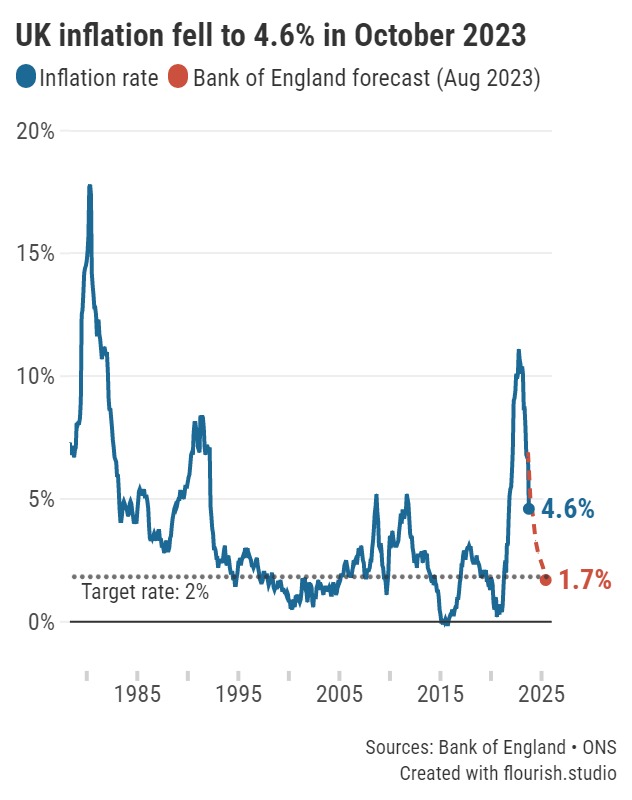

This is the lowest annual rate in two years, finds the Office for National Statistics (ONS).

UK inflation, the measure of how fast prices of goods and services are rising, slowed to 4.6% in the year to October, according to today’s release from the Office for National Statistics (ONS). This is down dramatically from 6.7% the previous month and sees the Government meet its pledge to halve inflation by the end of the year.

This is a positive sign that measures taken by the Bank of England are effective in helping towards its 2% target for inflation. Members of its Monetary Policy Committee (MPC) maintained the base rate at a 15-year high of 5.25% on the past two occasions they voted on the matter.

Caption: UK inflation slows dramatically to 4.6% in October 2023 - the lowest annual rate in two years according to the Office for National Statistics (ONS).

Housing and household services was one division to make significant downward contributions to inflation. This reflects electricity and gas prices falling both on the month and on the year.

Meanwhile, an easing in the annual rate for food and non-alcoholic beverages helped slow inflation. Of the categories in this division, the largest downward contribution came from milk, cheese, eggs and, most notably, yoghurt.

Otherwise, the costs associated with restaurants and hotels also made a contribution. However, as the effect from catering was small, the downward effect came almost entirely from overnight hotel accommodation.

It has taken over two years, but inflation has finally fallen to a level where there are now some standard savings accounts that can outpace its eroding prowess.

The savings market has felt a few rate cuts since last month’s inflation announcement, with fixed rate bonds under the spotlight.

Savers will no longer find a bond that pays more than 6%, but it is worth noting that challenger banks are still holding the top spots despite shuffling positions. These institutions can launch enticing offers to attract deposits for their future lending, but they also act quickly to pull offers when they become fully subscribed. However, consumers will need to act quickly to grab the top deals on offer and consider the more unfamiliar brands when comparing deals.

Our savings charts are regularly updated throughout the day to show you the best rates currently available. Alternatively, you can read our weekly savings and ISA roundups for further details on accounts offering some of the top rates.

The incentive to switch remains for those savers with flexible pots, as many of the top rate deals that pay 5% or more for new customers do not come from the biggest high street bank brands. It’s simple and easy to switch, but savers must check the terms of any new account carefully, such as those with withdrawal restrictions or introductory bonus rates.

To take full advantage of the best deals, it’s worth spreading any investment across easy access accounts and fixed bonds, but there are also notice accounts to consider which currently pay competitive rates.

Cash ISAs are still offering attractive rates, but there remains a rate gap between the top fixed rate bond and fixed rate ISAs. There are not as many brands operating accounts under an ISA wrapper, so savers must be sure to consider these deals carefully while also being conscious of any Personal Savings Allowance (PSA) they have.

As we edge closer to the end of the year, consumers may well be thinking about spending rather than saving, but it’s still a good time to set up a nest egg to fall back on, just in case.

All of our newsletters are available free by email to all Moneyfactscompare.co.uk users.

Send me Weekend Moneyfactscompare, Savers Friend, and Companies Friend.

Information is correct as of the date of publication (shown at the top of this article). Any products featured may be withdrawn by their provider or changed at any time. Links to third parties on this page are paid for by the third party. You can find out more about the individual products by visiting their site. Moneyfactscompare.co.uk will receive a small payment if you use their services after you click through to their site. All information is subject to change without notice. Please check all terms before making any decisions. This information is intended solely to provide guidance and is not financial advice. Moneyfacts will not be liable for any loss arising from your use or reliance on this information. If you are in any doubt, Moneyfacts recommends you obtain independent financial advice.

Moneyfactscompare.co.uk will never contact you by phone to sell you any financial product. Any calls like this are not from Moneyfacts. Emails sent by Moneyfactscompare.co.uk will always be from news@moneyfacts-news.co.uk. Be ScamSmart.

Moneyfactscompare.co.uk will never contact you by phone to sell you any financial product. Any calls like this are not from Moneyfacts. Emails sent by Moneyfactscompare.co.uk will always be from news@moneyfacts-news.co.uk. Be ScamSmart.

Moneyfactscompare.co.uk will never contact you by phone to sell you any financial product. Any calls like this are not from Moneyfacts. Emails sent by Moneyfactscompare.co.uk will always be from news@moneyfacts-news.co.uk. Be ScamSmart.

Moneyfactscompare.co.uk will never contact you by phone to sell you any financial product. Any calls like this are not from Moneyfacts. Emails sent by Moneyfactscompare.co.uk will always be from news@moneyfacts-news.co.uk. Be ScamSmart.

Moneyfactscompare.co.uk will never contact you by phone to sell you any financial product. Any calls like this are not from Moneyfacts. Emails sent by Moneyfactscompare.co.uk will always be from news@moneyfacts-news.co.uk. Be ScamSmart.

Moneyfactscompare.co.uk will never contact you by phone to sell you any financial product. Any calls like this are not from Moneyfacts. Emails sent by Moneyfactscompare.co.uk will always be from news@moneyfacts-news.co.uk. Be ScamSmart.