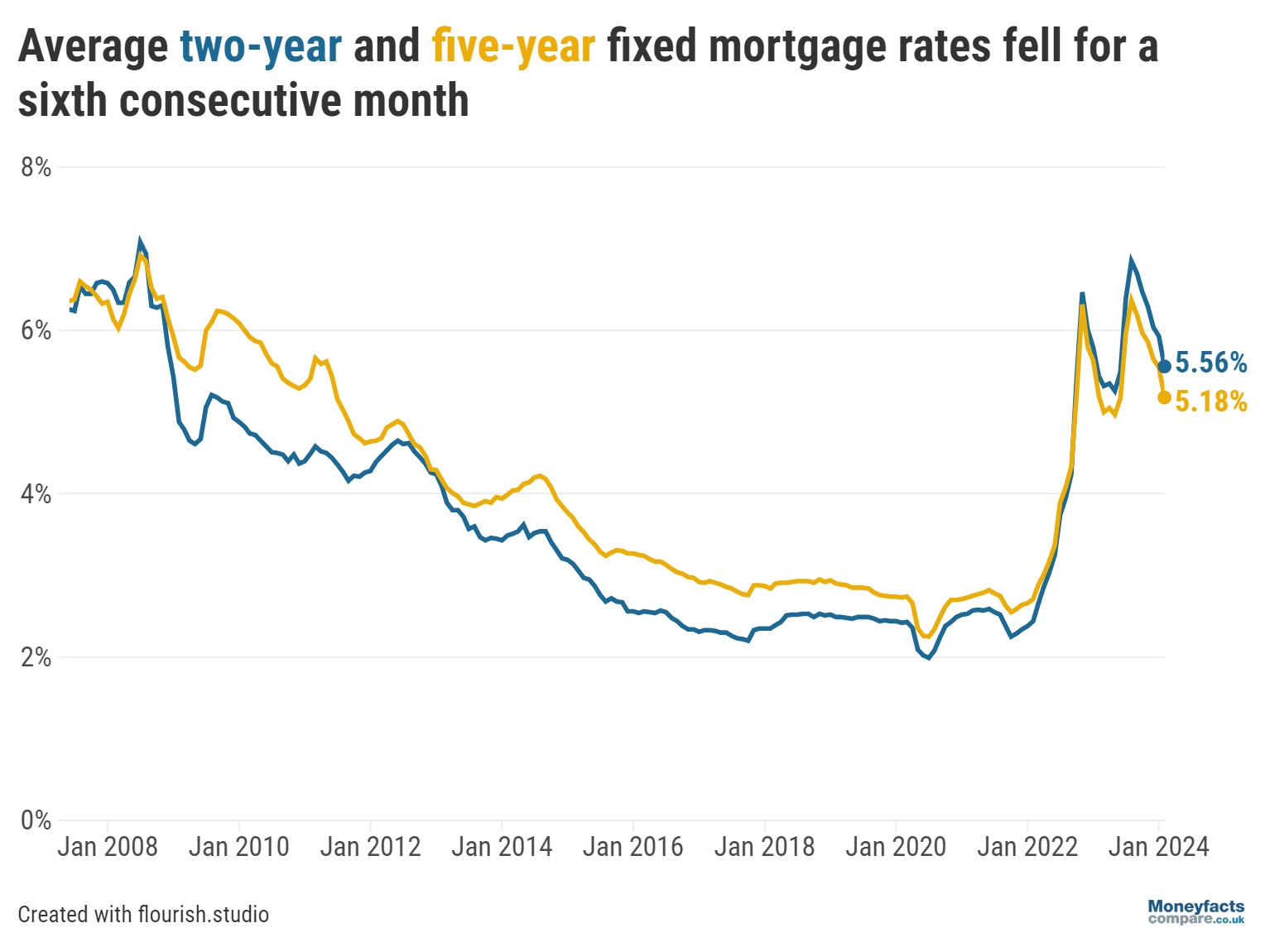

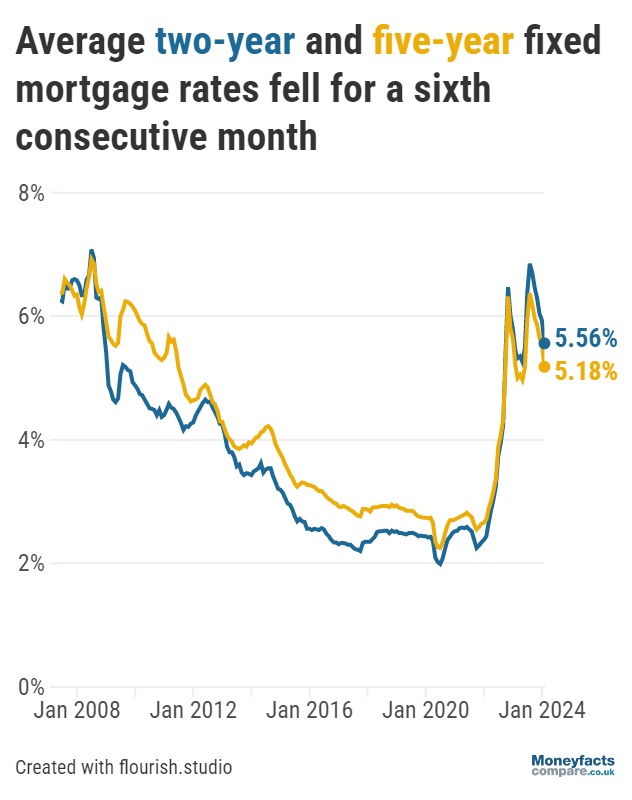

The average fixed mortgage rate fell by 0.37 percentage points between January and February.

Average rates on both two- and five-year fixed mortgages saw their sixth consecutive month-on-month fall to stand at 5.56% and 5.18% respectively at the start of February, Moneyfacts’ data finds.

This is a drop of 0.37 percentage points for both products compared to the start of January and is the largest monthly fall in average two-year fixed rates since December 2022.

Because of the consecutive monthly falls, average rates on both two- and five-year fixed mortgages are now significantly lower than at the start of August 2023, when these rates were 6.85% and 6.37% respectively.

At 5.18%, the average five-year fixed rate is now even lower than one year ago, when it stood at 5.20%.

Caption: Average two-year and five-year fixed mortgage rates fell for a sixth consecutive month.

The average Standard Variable Rate (SVR) also saw a slight month-on-month drop from 8.18% to 8.17% but, unlike fixed rates, it continues to be higher than the 7.85% average at the start of August 2023.

“Borrowers who are sitting on their Standard Variable Rate (SVR) should be incentivised to switch their mortgage if they can, as it’s unlikely they will see their repayments drop for the foreseeable. Indeed, the average two- and five-year fixed rates are much lower than the average SVR,” commented Rachel Springall, Finance Expert at Moneyfacts.

“Seeking advice from an independent broker is wise to work out if an individual could save a decent sum on their monthly repayments by changing their mortgage deal,” she added.

The mortgage market is showing some signs of improvement for prospective buyers looking to get on the property ladder. Average two- and five-year fixed mortgage rates for 90% and 95% LTV also continued to fall and are significantly lower than they were six months ago.

“Indeed, the average two-year fixed rate mortgage at 95% loan-to-value has dropped below 6% for the first time since May 2023 (5.94%), much lower than six months ago, when it was just over 7%,” commented Springall.

“Product choice has also increased at this LTV bracket and, while it’s a slight improvement month-on-month, it is encouraging and demonstrates lenders are still keen to support borrowers with small deposits,” she continued.

At the start of February there were 274 deals with a maximum LTV of 95%, an increase from 270 in January and 149 one year ago.

However, the number of deals catering for up to 90% LTV fell from 733 to 681 between January and February.

As lenders are constantly reviewing their rates and product ranges, the choice of deals across all LTVs may remain volatile this year. Although the average shelf-life of a mortgage currently sits at 28 days – its longest since February 2023 – borrowers may need to act quickly to take advantage of an attractive deal.

Whether you’re a first-time buyer, moving home or looking to remortgage, you can use our dedicated charts to compare mortgage deals from across the market.

All of our newsletters are available free by email to all Moneyfactscompare.co.uk users.

Send me Weekend Moneyfactscompare, Savers Friend, and Companies Friend.

Information is correct as of the date of publication (shown at the top of this article). Any products featured may be withdrawn by their provider or changed at any time. Links to third parties on this page are paid for by the third party. You can find out more about the individual products by visiting their site. Moneyfactscompare.co.uk will receive a small payment if you use their services after you click through to their site. All information is subject to change without notice. Please check all terms before making any decisions. This information is intended solely to provide guidance and is not financial advice. Moneyfacts will not be liable for any loss arising from your use or reliance on this information. If you are in any doubt, Moneyfacts recommends you obtain independent financial advice.

Moneyfactscompare.co.uk will never contact you by phone to sell you any financial product. Any calls like this are not from Moneyfacts. Emails sent by Moneyfactscompare.co.uk will always be from news@moneyfacts-news.co.uk. Be ScamSmart.

Moneyfactscompare.co.uk will never contact you by phone to sell you any financial product. Any calls like this are not from Moneyfacts. Emails sent by Moneyfactscompare.co.uk will always be from news@moneyfacts-news.co.uk. Be ScamSmart.

Moneyfactscompare.co.uk will never contact you by phone to sell you any financial product. Any calls like this are not from Moneyfacts. Emails sent by Moneyfactscompare.co.uk will always be from news@moneyfacts-news.co.uk. Be ScamSmart.

Moneyfactscompare.co.uk will never contact you by phone to sell you any financial product. Any calls like this are not from Moneyfacts. Emails sent by Moneyfactscompare.co.uk will always be from news@moneyfacts-news.co.uk. Be ScamSmart.

Moneyfactscompare.co.uk will never contact you by phone to sell you any financial product. Any calls like this are not from Moneyfacts. Emails sent by Moneyfactscompare.co.uk will always be from news@moneyfacts-news.co.uk. Be ScamSmart.

Moneyfactscompare.co.uk will never contact you by phone to sell you any financial product. Any calls like this are not from Moneyfacts. Emails sent by Moneyfactscompare.co.uk will always be from news@moneyfacts-news.co.uk. Be ScamSmart.