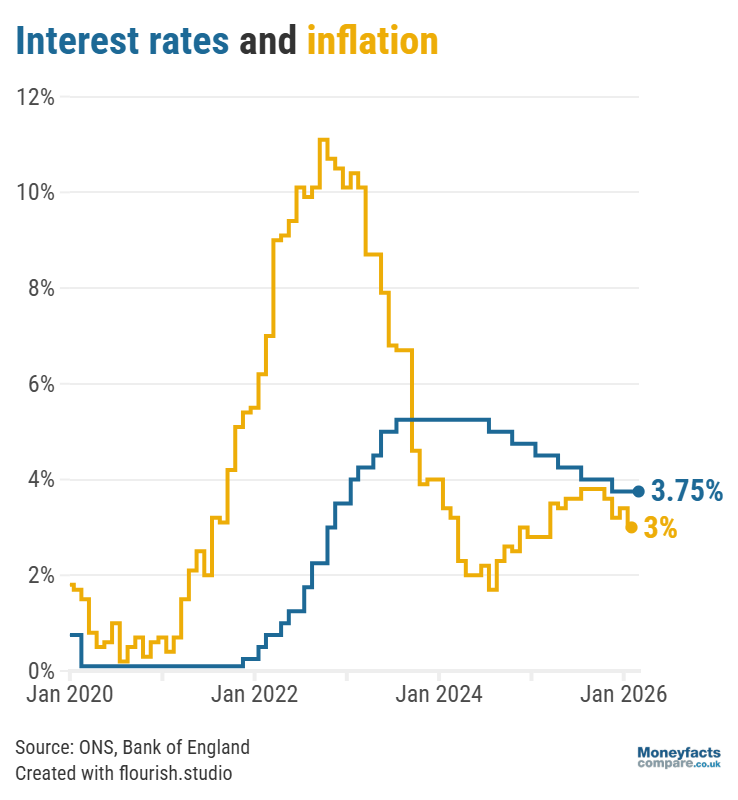

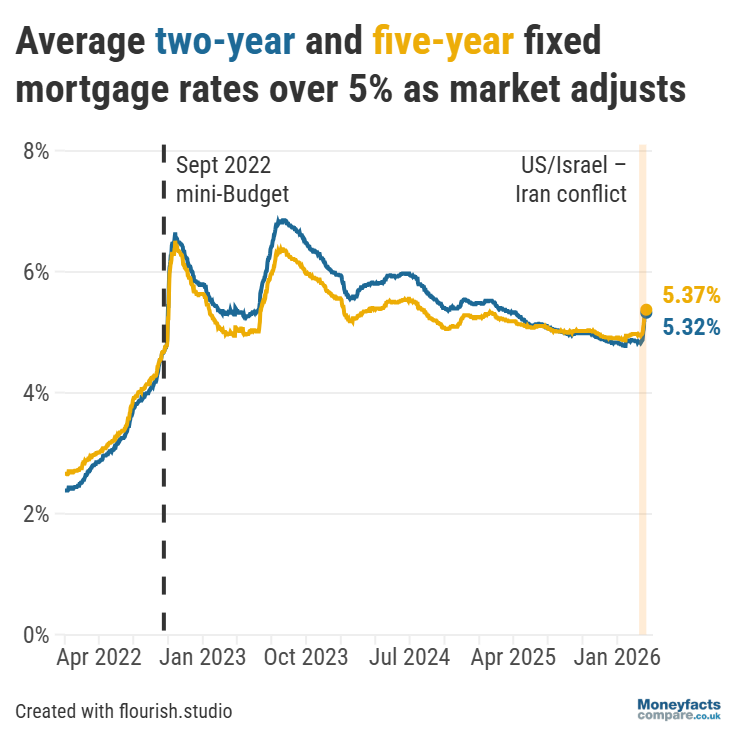

The UK mortgage market is already feeling the consequences.

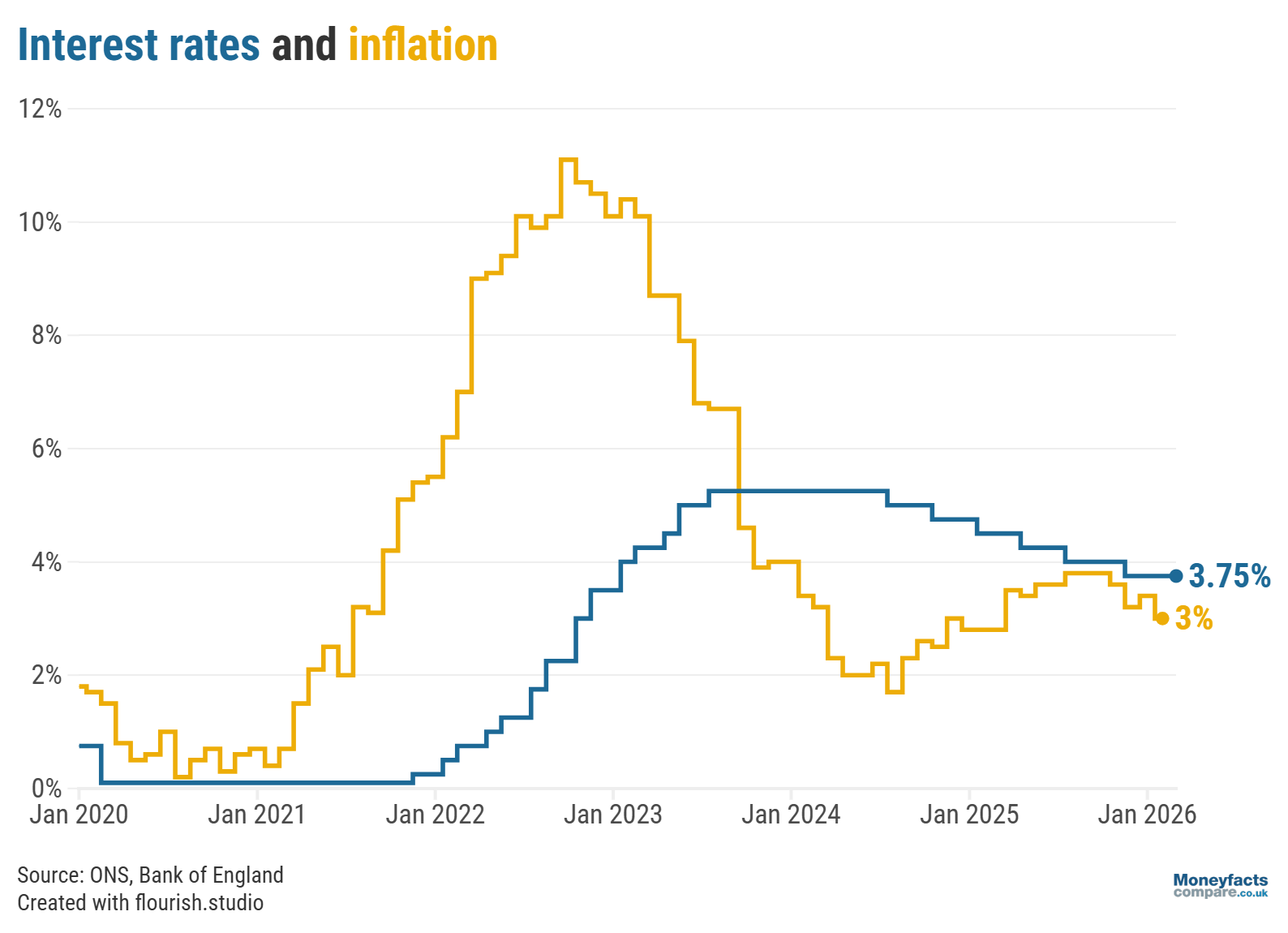

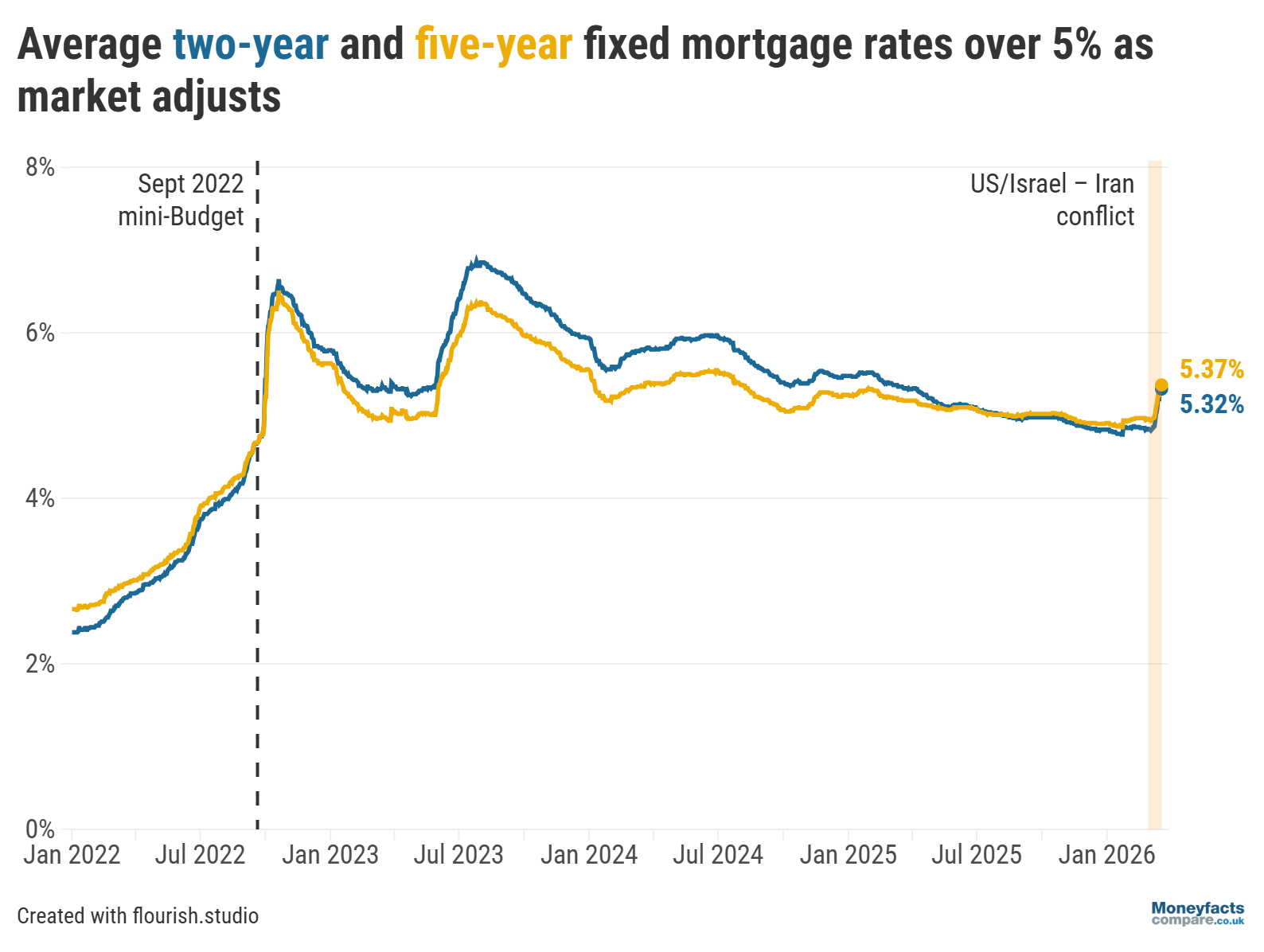

The Bank of England base rate will remain on hold at 3.75%, its Monetary Policy Committee (MPC) has decided – demonstrating just how quickly the outlook can change.

Only a matter of weeks ago, it was widely anticipated the UK’s central bank might look to cut interest rates. However, it now appears the MPC is waiting to better understand how ongoing conflict in the Middle East is impacting the economy before it decides what action – if any – to take.

While latest inflation figures are expected next week from the Office for National Statistics (ONS), they will reflect the period before the US and Israel joined forces against Iran. Instead, eyes will be on when inflation figures for March are published – with fear it could creep higher as the war disrupts global oil supplies and drives up prices.

UK Finance Trends: Graph showing the Bank of England base rate and the rate of inflation between 2020 and March 2026.

The base rate is the amount of interest the Bank of England charges commercial banks, building societies and other financial institutions to borrow money which, in turn, influences how these organisations price their mortgages and savings products.

It can therefore be used as a tool to keep inflation in check. For example, during periods of high inflation, the Bank of England might raise the base rate to lessen demand (by rewarding saving and making it more expensive to borrow money).

On the other hand, the Bank of England might lower the base rate to support economic growth (by making borrowing cheaper to encourage greater levels of spending). Learn more about inflation and the base rate.

Despite there being no change to the base rate, the recent turmoil has already had an adverse effect on the UK mortgage market.

“The unrest in the Middle East has led to rising swap rates, which has inflated mortgage rates and caused deals to be pulled from sale, some temporarily,” said Rachel Springall, Finance Expert at Moneyfactscompare.co.uk. As a result, the average two-year fixed mortgage rate has risen from 4.84% at the start of the month to 5.32% this morning, while the typical rate charged by a five-year fixed deal jumped from 4.96% to 5.37% over the same timeframe.

UK Mortgage Trends: Graph showing average two- and five-year fixed mortgage rates between 2022 and March 2026.

To make matters worse, borrowers will find fixed mortgages priced below 4% have almost entirely vanished from the market. “Lenders look at margins very carefully, so it would be unwise to price their deals too low,” Springall explained

“If such uncertainty is prolonged, and indeed if inflation spikes, we could even see an increase to the Bank of England base rate before the year is over,” she warned. “It really is too early to tell what might happen, but borrowers searching for a new deal should seek advice if they are concerned about rising costs,” Springall added.

Meanwhile, Oliver Dack, Spokesperson at Mortgage Advice Bureau, said “borrowers within six months of their product end date would be wise to explore a new deal as early as possible”. He added that “even those outside of this window may find it more cost-effective to shoulder any Early Repayment Charges (ERCs) and lock in a fixed rate now” if borrowing costs continue to rise.

“It’s uncertain when conflict in the Middle East will end but, even when it does, mortgage rates are unlikely to bounce back overnight. The silver lining is that rates are still cheaper than a couple of years ago despite the recent volatility,” said Dack. “We monitor the market regularly and, if conditions were to improve before completion, we can look to move our clients onto a better deal should one become available,” he added.

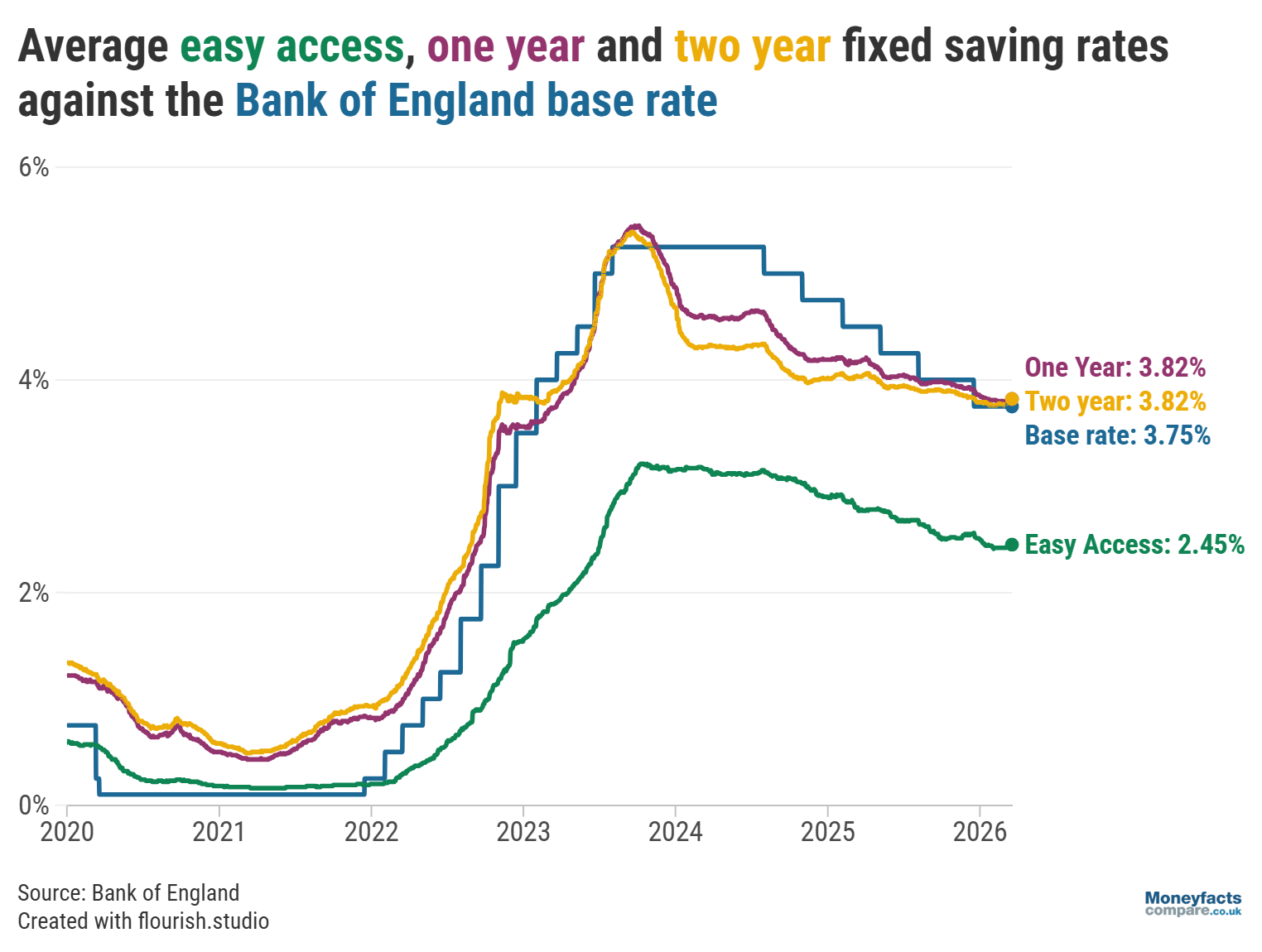

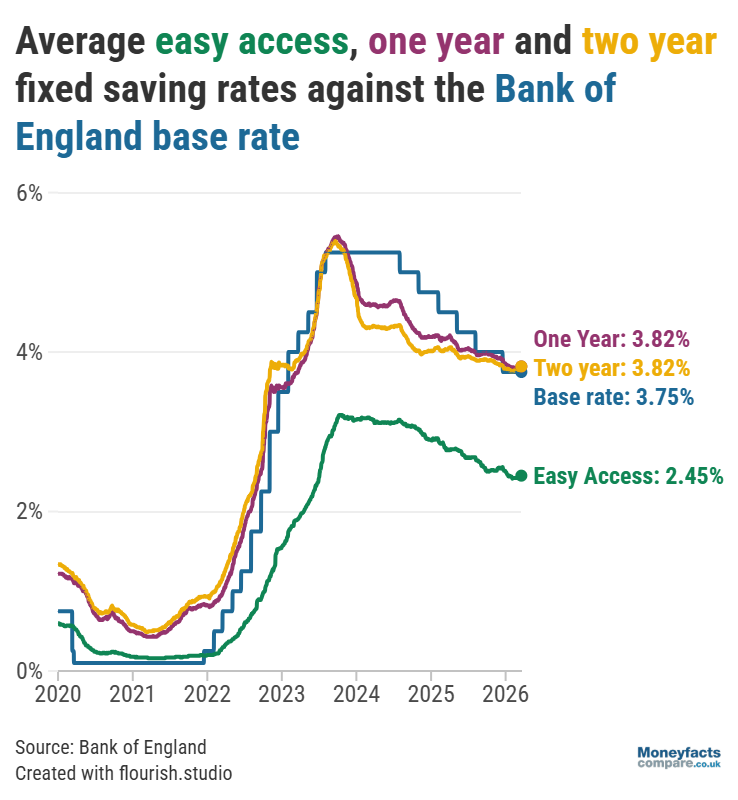

In contrast, Springall said maintaining the base rate at its current level could offer savers a “short respite”, as providers may hold off making changes to their product ranges until the situation becomes clearer.

“Savers have been hit hard by cuts to the Bank of England base rate, as less than half the market (40%) can now beat 3.75%,” she explained. The average rate paid by an easy access account, for instance, fell from 2.85% in March last year to 2.42% by the start of this month. Typical returns on a notice account, meanwhile, saw an even steeper decline from 3.86% to 3.31% over the same period.

UK Savings Trends: Graph showing average easy access, one- and two-year fixed savings rates between 2020 and March 2026.

With concern that inflation could accelerate over the coming months, it’s crucial savers who want to combat the rising cost of living review their accounts and consider switching if better returns are available. Those worried about earning enough interest to exceed their Personal Savings Allowance (and being faced with a tax bill) may also want to make the most of this year’s £20,000 ISA allowance before it automatically resets in a little over two weeks’ time (on 6 April).

Our savings charts are regularly updated throughout the day so you can discover the best and latest rates currently available.

You can also read our daily ISA roundup and weekly savings roundup for more information on the most competitive accounts, and subscribe to our Savers Friend newsletter for weekly updates on changes from across the savings market.

All of our newsletters are available free by email to all Moneyfactscompare.co.uk users.

Send me Weekend Moneyfactscompare, Savers Friend, and Companies Friend.

Information is correct as of the date of publication (shown at the top of this article). Any products featured may be withdrawn by their provider or changed at any time. Links to third parties on this page are paid for by the third party. You can find out more about the individual products by visiting their site. Moneyfactscompare.co.uk will receive a small payment if you use their services after you click through to their site. All information is subject to change without notice. Please check all terms before making any decisions. This information is intended solely to provide guidance and is not financial advice. Moneyfacts will not be liable for any loss arising from your use or reliance on this information. If you are in any doubt, Moneyfacts recommends you obtain independent financial advice.

Moneyfactscompare.co.uk will never contact you by phone to sell you any financial product. Any calls like this are not from Moneyfacts. Emails sent by Moneyfactscompare.co.uk will always be from news@moneyfacts-news.co.uk. Be ScamSmart.

Moneyfactscompare.co.uk will never contact you by phone to sell you any financial product. Any calls like this are not from Moneyfacts. Emails sent by Moneyfactscompare.co.uk will always be from news@moneyfacts-news.co.uk. Be ScamSmart.

Moneyfactscompare.co.uk will never contact you by phone to sell you any financial product. Any calls like this are not from Moneyfacts. Emails sent by Moneyfactscompare.co.uk will always be from news@moneyfacts-news.co.uk. Be ScamSmart.

Moneyfactscompare.co.uk will never contact you by phone to sell you any financial product. Any calls like this are not from Moneyfacts. Emails sent by Moneyfactscompare.co.uk will always be from news@moneyfacts-news.co.uk. Be ScamSmart.

Moneyfactscompare.co.uk will never contact you by phone to sell you any financial product. Any calls like this are not from Moneyfacts. Emails sent by Moneyfactscompare.co.uk will always be from news@moneyfacts-news.co.uk. Be ScamSmart.

Moneyfactscompare.co.uk will never contact you by phone to sell you any financial product. Any calls like this are not from Moneyfacts. Emails sent by Moneyfactscompare.co.uk will always be from news@moneyfacts-news.co.uk. Be ScamSmart.