If costs rise too rapidly, this could push the Bank of England to increase interest rates.

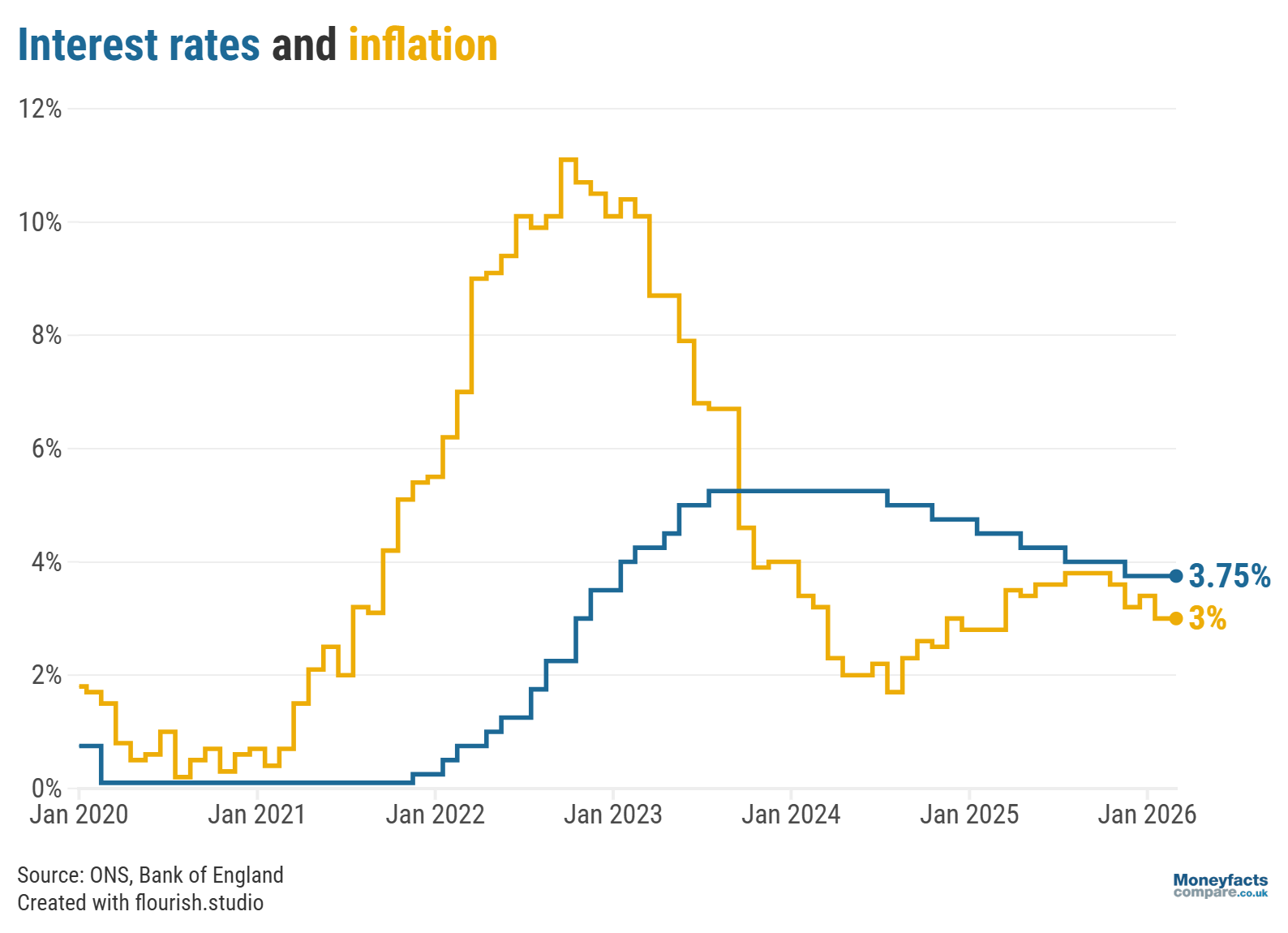

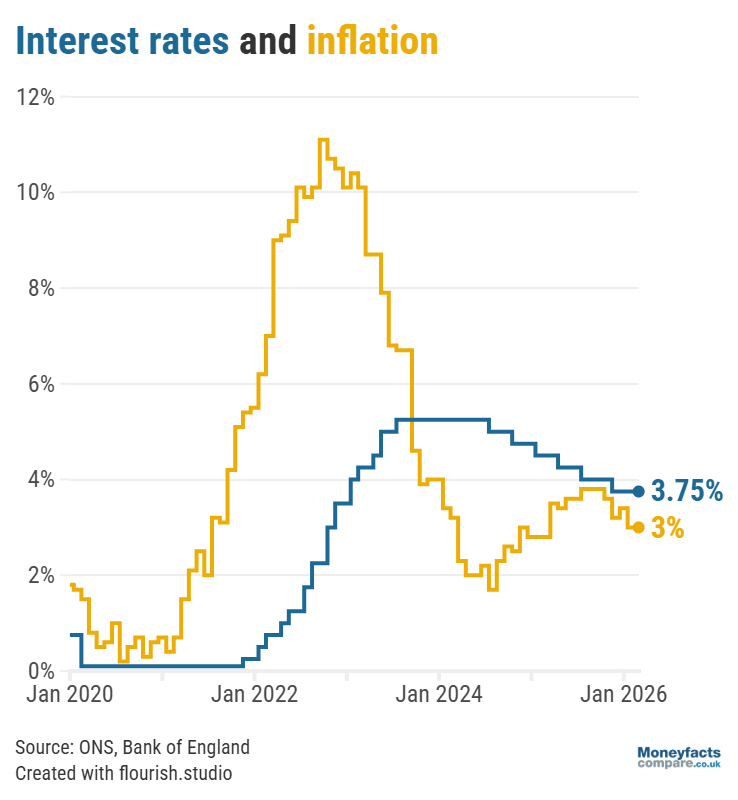

While UK inflation held steady at 3% in the year to February 2026 (the Office for National Statistics today revealed), consumers must brace themselves for costs to rise more rapidly in the coming months as conflict in the Middle East continues.

Importantly, it should be noted that these latest figures were recorded before joint US and Israeli airstrikes on Iran began on 28 February 2026 and were kept low by a 4.6% decline in overall motor fuel prices year-on-year.

UK Finance Trends: Graph showing the Bank of England base rate and the rate of inflation between 2020 and February 2026.

However, it’s likely costs will climb at a faster rate going forwards as the war in Iran disrupts global oil and gas supplies – not only impacting household fuel and energy bills but also driving up business expenses. Indeed, according to the RAC, the average price of petrol has risen by 15.7 pence per litre since the start of the conflict, while the average price of diesel leaped by a more substantial 31.5 pence per litre.

As such, the Bank of England has suggested inflation will be delayed in returning to its 2% target and could reach 3.5% later this year.

Although there’s been no change in the annual rate of inflation between January and February, this doesn’t mean the price of goods and services have stayed the same. Instead, they are continuing to rise at the same pace (year-on-year) as in the previous month. Learn more about inflation and how it affects your finances.

If inflation was to accelerate in the months ahead, this could cause the Bank of England to raise the UK’s central interest rate (also known as the ‘base rate’) to get it back under control. But, “even just one 0.25% hike could push mortgage rates higher,” warned Caitlyn Eastell, Personal Finance Analyst at Moneyfactscompare.co.uk.

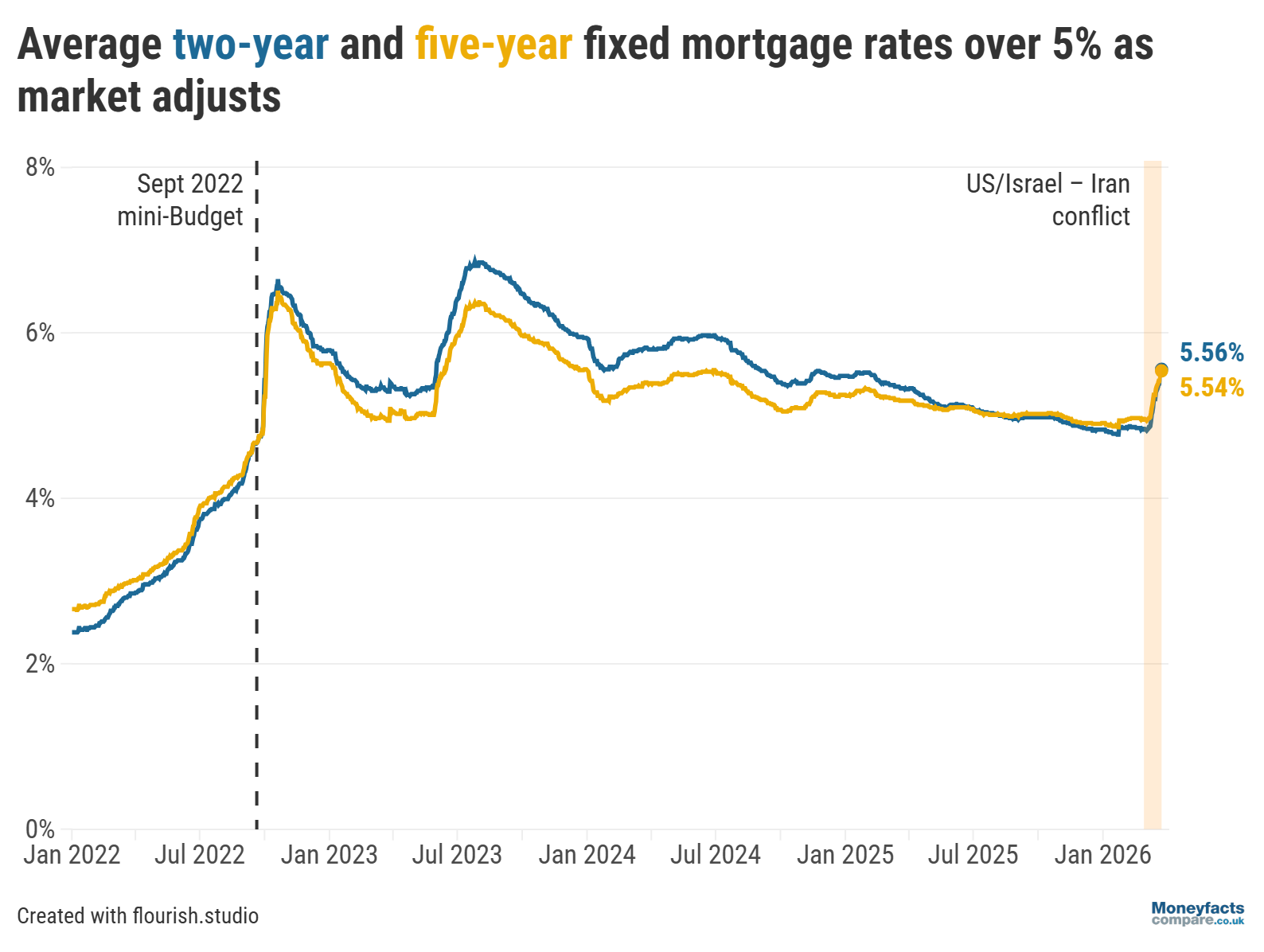

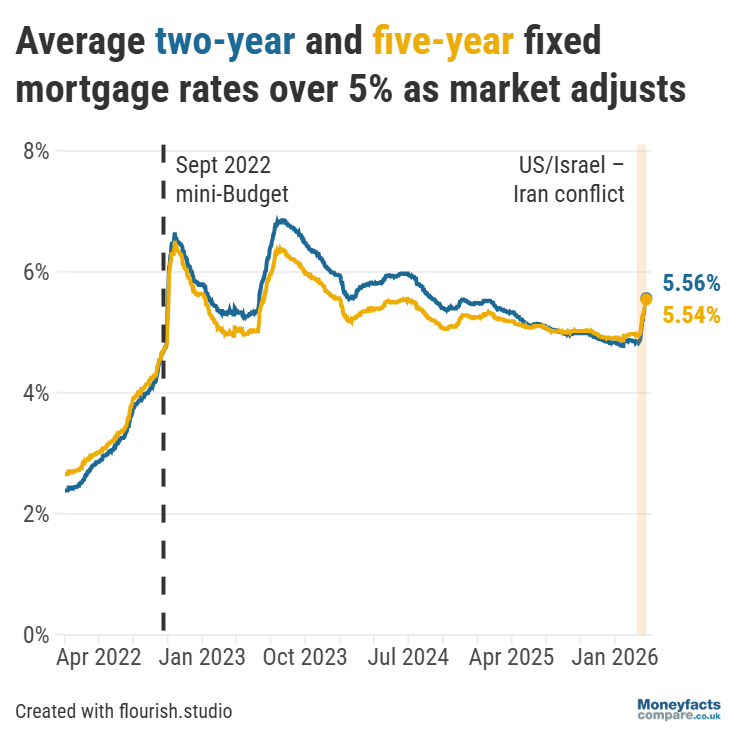

The uncertainty has already seen more than 1,700 products pulled from the mortgage market since 9 March 2026. While some have returned, Eastell explained that they now charge higher rates as lenders are expecting the base rate to rise this year. This has led the average two-year fixed mortgage rate to jump from 4.84% at the start of the month to 5.56% this morning and the average five-year fixed rate rise from 4.96% to 5.54% over the same period.

UK Mortgage Trends: Graph showing average two- and five-year fixed mortgage rates between 2022 and March 2026.

This will no doubt disappoint the roughly 1.8 million borrowers due to refinance this year – particularly those coming to the end of a cheap five-year fixed deal. “Homeowners should prepare themselves for higher-than-expected costs,” said Eastell, adding that “if they lock into another five-year term, they could see their monthly repayments spike by over £380”.

“Borrowers have the option of securing a new deal typically up to six months before their current rate expires, [which] may be crucial for those who are concerned about rising costs. This also avoids borrowers slipping onto their revert rate, which would add over £630 per month on average, an amount that many may not be able to afford,” she continued.

Meanwhile, Eastell said the ongoing volatility is a “double-edged sword” for savers.

“Stubborn inflation could slam the brakes on rate cuts, or even prompt hikes which could deliver short-term boosts to savings returns. This relief is short-lived [as], if inflation stays elevated, it will quickly erode ‘real’ returns and chip away at the true value of savers’ cash,” she explained.

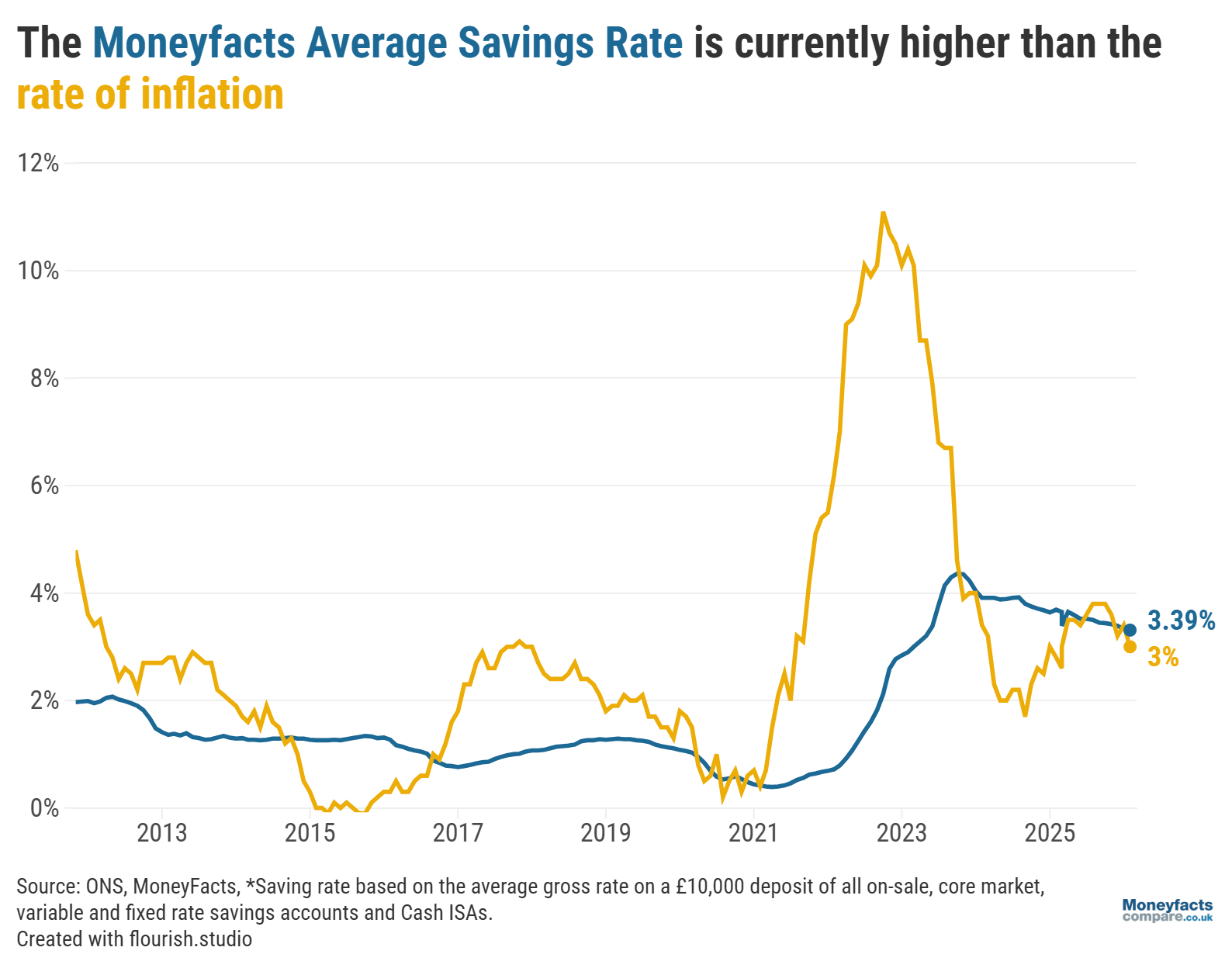

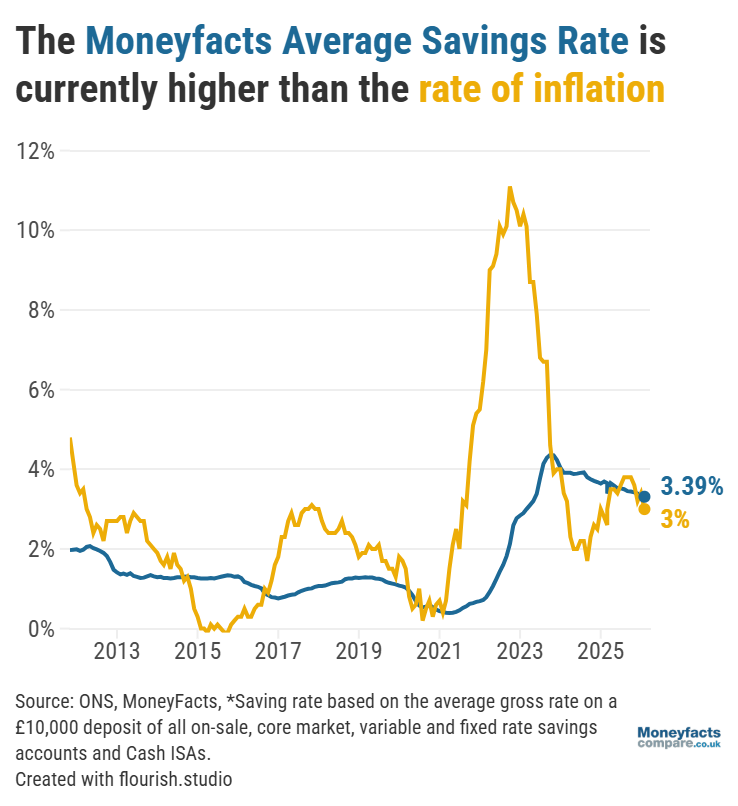

Despite the Moneyfacts Average Savings Rate currently sitting above inflation (at 3.39%) and there being more than 1,600 savings accounts that can outpace the rate at which costs are rising, Eastell urged savers to hunt for the most competitive returns as “settling for average won’t cut it”. At the time of writing, the top easy access savings account (Tembo Money’s HomeSaver) pays 4.75% AER (inclusive of a 1.75% bonus for 12 months).

UK Savings Trends: Graph showing the Moneyfacts Average Savings Rate and the rate of inflation between 2011 and March 2026.

With the end of the tax-year fast approaching, savers may also find that ISAs offer a competitive return as providers try to encourage people to use their £20,000 allowance before it automatically resets once the new tax-year begins (on 6 April). And, with the cash ISA limit set to be cut to £12,000 for under-65s from April 2027, it could prove crucial for savers to maximise their contributions now, as well as in the months ahead.

“Providers will be continuing to compete for investors’ new cash for weeks after the deadline, meaning it’s worth tracking the top returns beyond April,” Eastell reminded.

Our savings and ISA charts are updated hourly every day between 9am and 5pm so you can discover the best and latest rates available.

You can also read our weekly savings roundup and daily ISA roundup for more information on the most competitive accounts, and subscribe to our Savers Friend newsletter for regular updates on changes from across the savings market.

All of our newsletters are available free by email to all Moneyfactscompare.co.uk users.

Send me Weekend Moneyfactscompare, Savers Friend, and Companies Friend.

Information is correct as of the date of publication (shown at the top of this article). Any products featured may be withdrawn by their provider or changed at any time. Links to third parties on this page are paid for by the third party. You can find out more about the individual products by visiting their site. Moneyfactscompare.co.uk will receive a small payment if you use their services after you click through to their site. All information is subject to change without notice. Please check all terms before making any decisions. This information is intended solely to provide guidance and is not financial advice. Moneyfacts will not be liable for any loss arising from your use or reliance on this information. If you are in any doubt, Moneyfacts recommends you obtain independent financial advice.

Moneyfactscompare.co.uk will never contact you by phone to sell you any financial product. Any calls like this are not from Moneyfacts. Emails sent by Moneyfactscompare.co.uk will always be from news@moneyfacts-news.co.uk. Be ScamSmart.

Moneyfactscompare.co.uk will never contact you by phone to sell you any financial product. Any calls like this are not from Moneyfacts. Emails sent by Moneyfactscompare.co.uk will always be from news@moneyfacts-news.co.uk. Be ScamSmart.

Moneyfactscompare.co.uk will never contact you by phone to sell you any financial product. Any calls like this are not from Moneyfacts. Emails sent by Moneyfactscompare.co.uk will always be from news@moneyfacts-news.co.uk. Be ScamSmart.

Moneyfactscompare.co.uk will never contact you by phone to sell you any financial product. Any calls like this are not from Moneyfacts. Emails sent by Moneyfactscompare.co.uk will always be from news@moneyfacts-news.co.uk. Be ScamSmart.

Moneyfactscompare.co.uk will never contact you by phone to sell you any financial product. Any calls like this are not from Moneyfacts. Emails sent by Moneyfactscompare.co.uk will always be from news@moneyfacts-news.co.uk. Be ScamSmart.

Moneyfactscompare.co.uk will never contact you by phone to sell you any financial product. Any calls like this are not from Moneyfacts. Emails sent by Moneyfactscompare.co.uk will always be from news@moneyfacts-news.co.uk. Be ScamSmart.