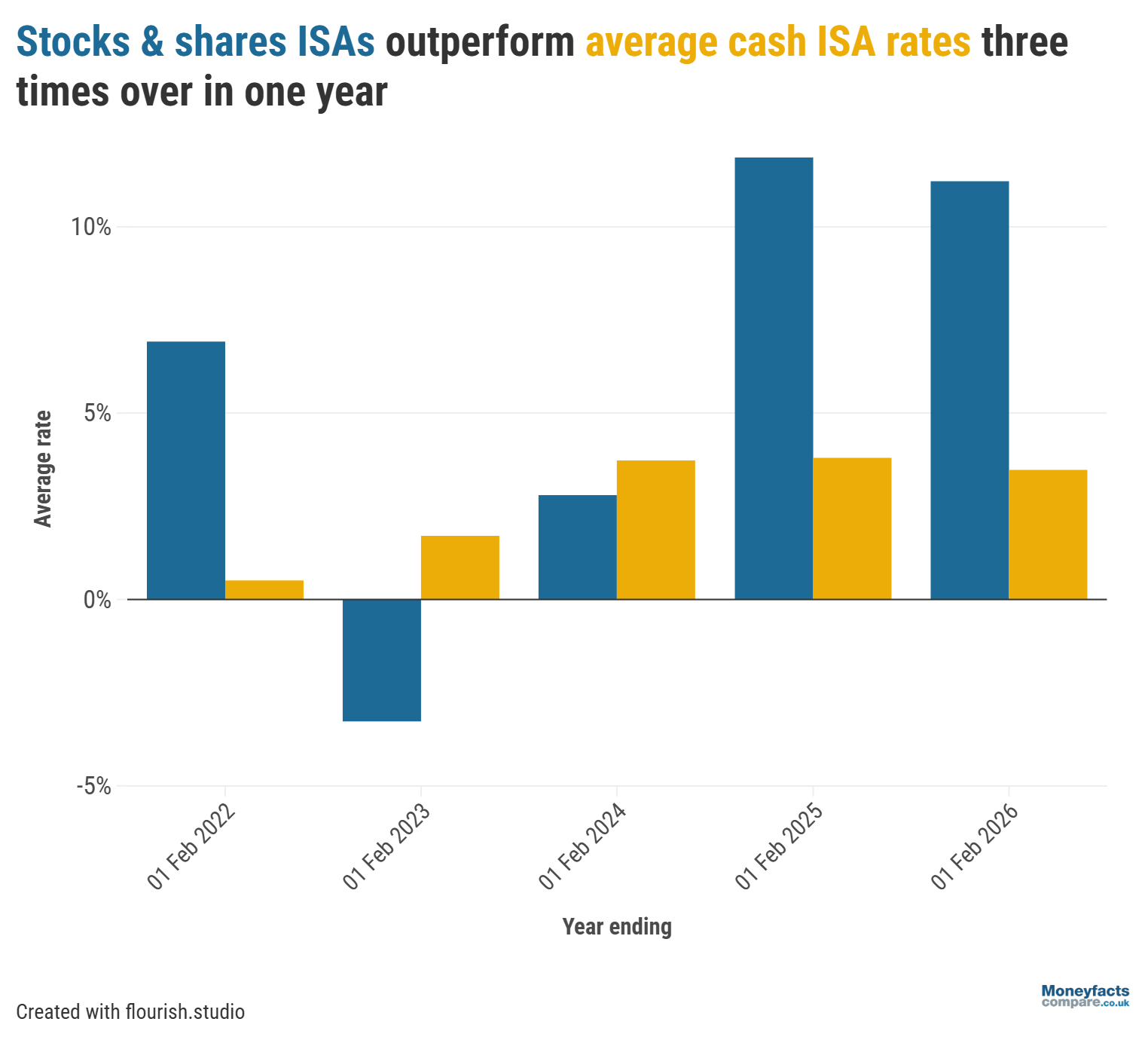

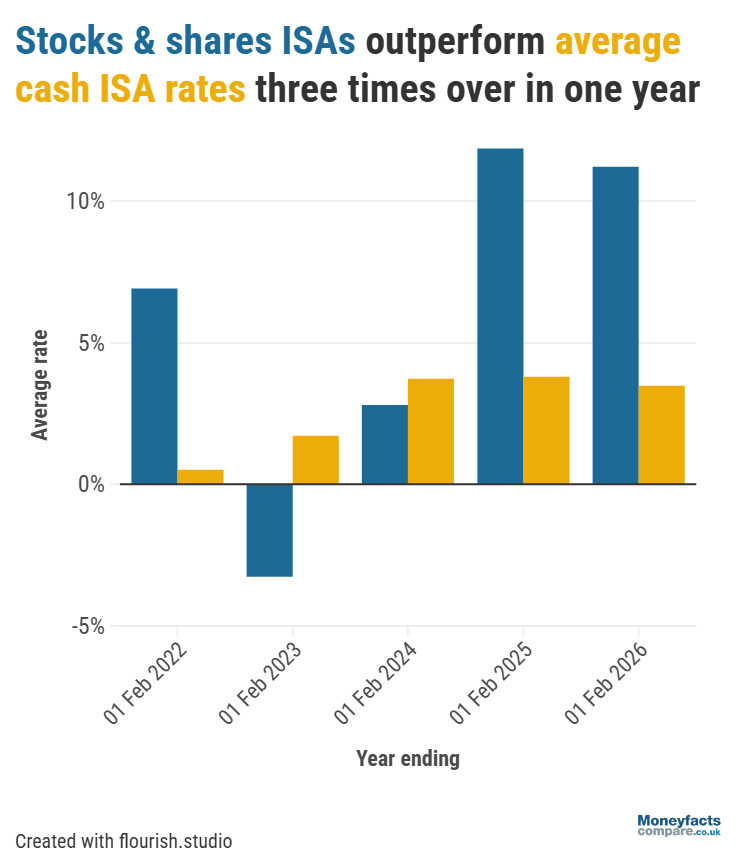

Stocks and shares ISAs returned three times more than cash ISAs, on average, over the past year.

Fear of investing could be costing savers a significant amount of money, according to latest analysis by Moneyfactscompare.co.uk. It found the average stocks and shares ISA fund grew by 11.22% in the year to February 2026 – returning three times more than a typical cash ISA over the same period (3.48%). This is the second consecutive year stocks and shares ISAs have outperformed their cash counterparts.

UK ISA Trends: Average stocks and shares ISA growth vs cash ISA growth between February 2022 and 2026.

“Cash is considered a safe choice, but investing shows the gains that could be made over the longer-term,” commented Rachel Springall, Finance Expert at Moneyfactscompare.co.uk. Although returns are never guaranteed, she said these latest figures should come as “a wake-up call” for anyone still hesitant about investing.

Of the more than half of Brits (55%) who don’t have any investments, a third (33%) said this is due to not knowing enough about investing, according to new research from Aviva. It also found almost two fifths (39%) think investing is too risky and are worried about losing money.

But, while Springall acknowledged that “not every saver will feel confident enough to invest” she said starting small and getting good guidance could help to build knowledge. There are plenty of stocks and shares ISAs that don’t require substantial monthly deposits. What’s more, some platforms offer ready-made portfolios to suit different attitudes towards risk.

That being said, those who opt for an investment platform should make sure they regularly review any management fees, “as the most cost-effective choice can vary depending on the size of someone’s portfolio,” warned Springall. She also encouraged savers to “monitor their pots and consider seeking other funds if they are seeing consecutive periods of poor performance”. Some might even want to contemplate moving their pots if their risk appetite changes over time.

Rising gold prices and general demand over raw materials (such as metal and oil) influenced fund performance over the past year, said Springall. As a result, the top-performing sectors, such as Commodities and Natural Resources, returned over 28%.

However, it’s important to remember that past performance is never an indication of future returns. While Latin America was the best-performing stocks and shares ISA fund sector and returned 38.24% over the past year, it was the worst-performing sector between February 2024 and 2025 (returning -11.15%).

“Those intrigued to know how well UK fund sectors have fared over the past 12 months may be pleased to see the UK All Companies fund returned 13.72%, slightly higher than a year prior of 13.26%,” Springall added.

Although stocks and shares ISAs offer the potential for higher returns, they won’t be a feasible option for everyone. These accounts are generally best suited to those who don’t mind putting their capital risk and are willing to stay invested over a long period of time (usually five years or more).

Instead, Springall explained that cash ISAs will remain “an attractive choice” for many savers – particularly those who’ll see their Personal Savings Allowance slashed (i.e. the amount of tax-free interest they can earn from their savings each year) after being dragged up the tax ladder.

However, time is running out to make the most of the cash ISA allowance at its current level; from April 2027, those under 65 will only be able to deposit up to £12,000 in cash ISAs each tax-year. This is part of the Government’s initiative to get more people investing.

All of our newsletters are available free by email to all Moneyfactscompare.co.uk users.

Send me Weekend Moneyfactscompare, Savers Friend, and Companies Friend.

Information is correct as of the date of publication (shown at the top of this article). Any products featured may be withdrawn by their provider or changed at any time. Links to third parties on this page are paid for by the third party. You can find out more about the individual products by visiting their site. Moneyfactscompare.co.uk will receive a small payment if you use their services after you click through to their site. All information is subject to change without notice. Please check all terms before making any decisions. This information is intended solely to provide guidance and is not financial advice. Moneyfacts will not be liable for any loss arising from your use or reliance on this information. If you are in any doubt, Moneyfacts recommends you obtain independent financial advice.

Moneyfactscompare.co.uk will never contact you by phone to sell you any financial product. Any calls like this are not from Moneyfacts. Emails sent by Moneyfactscompare.co.uk will always be from news@moneyfacts-news.co.uk. Be ScamSmart.

Moneyfactscompare.co.uk will never contact you by phone to sell you any financial product. Any calls like this are not from Moneyfacts. Emails sent by Moneyfactscompare.co.uk will always be from news@moneyfacts-news.co.uk. Be ScamSmart.

Moneyfactscompare.co.uk will never contact you by phone to sell you any financial product. Any calls like this are not from Moneyfacts. Emails sent by Moneyfactscompare.co.uk will always be from news@moneyfacts-news.co.uk. Be ScamSmart.

Moneyfactscompare.co.uk will never contact you by phone to sell you any financial product. Any calls like this are not from Moneyfacts. Emails sent by Moneyfactscompare.co.uk will always be from news@moneyfacts-news.co.uk. Be ScamSmart.

Moneyfactscompare.co.uk will never contact you by phone to sell you any financial product. Any calls like this are not from Moneyfacts. Emails sent by Moneyfactscompare.co.uk will always be from news@moneyfacts-news.co.uk. Be ScamSmart.

Moneyfactscompare.co.uk will never contact you by phone to sell you any financial product. Any calls like this are not from Moneyfacts. Emails sent by Moneyfactscompare.co.uk will always be from news@moneyfacts-news.co.uk. Be ScamSmart.