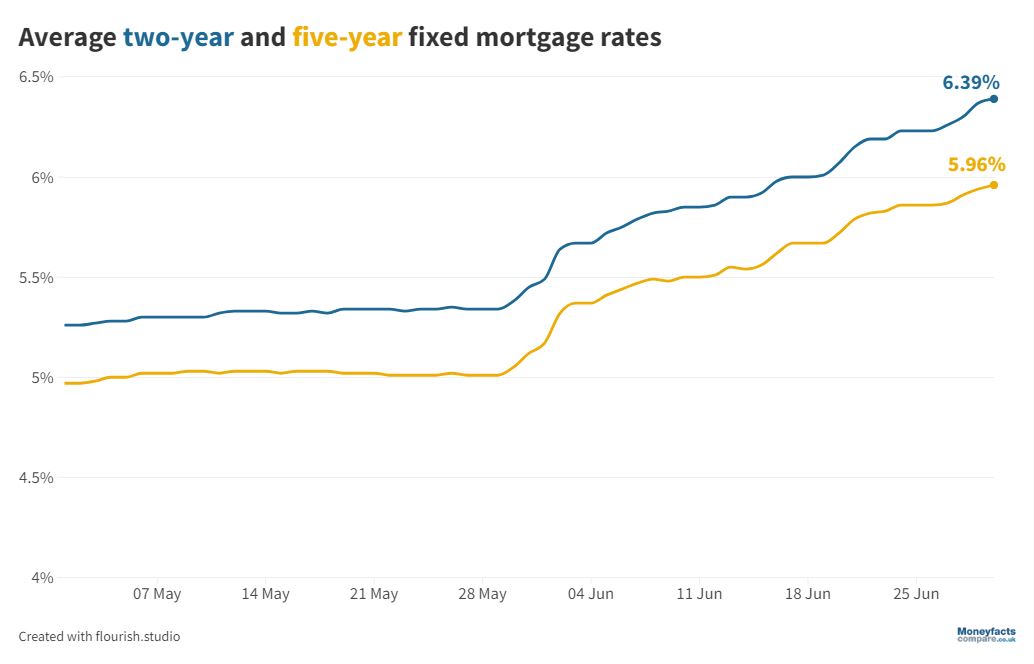

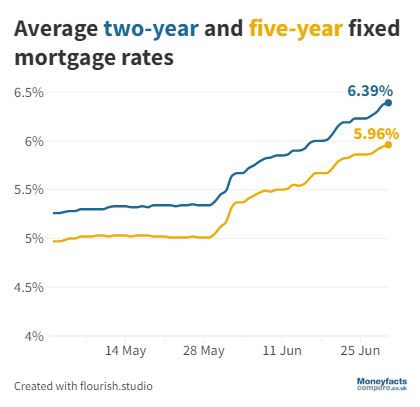

The average five year fixed rate is almost at 6%.

House prices remain broadly stable, according to Nationwide BS, one of the UK’s largest mortgage lenders. In the month to June prices nudged up 0.1%, but are down 3.5% on an annual basis.

However, the building society also made note that rising borrowing costs will likely force a cooldown across the market in the near term.

“Despite the higher interest rates available to savers, the sharp rise in rents, together with continued high rates of inflation more generally is continuing to make it difficult for many prospective buyers to save for a deposit,” said Robert Gardener, Chief Economist at Nationwide BS.

He also noted that rising borrowing costs will affect those already on the property ladder.

With two year fixed rates above 6%, Gardner said those looking to refinance could expect to add 4.25 percentage points onto their mortgage rate. This equates to an increase of £385 per month for the typical borrower.

“Clearly this represents a significant increase, but those borrowers were stress tested at interest rates above those now prevailing in the market to ensure they could cope with such an increase,” said Gardener.

Today the average five year fixed rate stands at 5.96%, according to Moneyfacts data.

Like the average two year rate, this figure has risen sharply after back-to-back worse-than-expected inflation figures.

If the average five year rate were to breach 6%, it would be the first time this figure has surpassed this point since last November. At this point average fixed rates were on their way down from the aftermath of the mini-Budget.

All of our newsletters are available free by email to all Moneyfactscompare.co.uk users.

Send me Weekend Moneyfactscompare, Savers Friend, and Companies Friend.

Information is correct as of the date of publication (shown at the top of this article). Any products featured may be withdrawn by their provider or changed at any time. Links to third parties on this page are paid for by the third party. You can find out more about the individual products by visiting their site. Moneyfactscompare.co.uk will receive a small payment if you use their services after you click through to their site. All information is subject to change without notice. Please check all terms before making any decisions. This information is intended solely to provide guidance and is not financial advice. Moneyfacts will not be liable for any loss arising from your use or reliance on this information. If you are in any doubt, Moneyfacts recommends you obtain independent financial advice.

Moneyfactscompare.co.uk will never contact you by phone to sell you any financial product. Any calls like this are not from Moneyfacts. Emails sent by Moneyfactscompare.co.uk will always be from news@moneyfacts-news.co.uk. Be ScamSmart.

Moneyfactscompare.co.uk will never contact you by phone to sell you any financial product. Any calls like this are not from Moneyfacts. Emails sent by Moneyfactscompare.co.uk will always be from news@moneyfacts-news.co.uk. Be ScamSmart.

Moneyfactscompare.co.uk will never contact you by phone to sell you any financial product. Any calls like this are not from Moneyfacts. Emails sent by Moneyfactscompare.co.uk will always be from news@moneyfacts-news.co.uk. Be ScamSmart.

Moneyfactscompare.co.uk will never contact you by phone to sell you any financial product. Any calls like this are not from Moneyfacts. Emails sent by Moneyfactscompare.co.uk will always be from news@moneyfacts-news.co.uk. Be ScamSmart.

Moneyfactscompare.co.uk will never contact you by phone to sell you any financial product. Any calls like this are not from Moneyfacts. Emails sent by Moneyfactscompare.co.uk will always be from news@moneyfacts-news.co.uk. Be ScamSmart.

Moneyfactscompare.co.uk will never contact you by phone to sell you any financial product. Any calls like this are not from Moneyfacts. Emails sent by Moneyfactscompare.co.uk will always be from news@moneyfacts-news.co.uk. Be ScamSmart.