The inversion of fixed mortgage rates reflects the ongoing volatility and uncertainty in the market caused by the conflict in the Middle East.

The mortgage market continues to feel the effects of the Iran war, as lenders adjust to the changing conditions by raising rates and withdrawing deals.

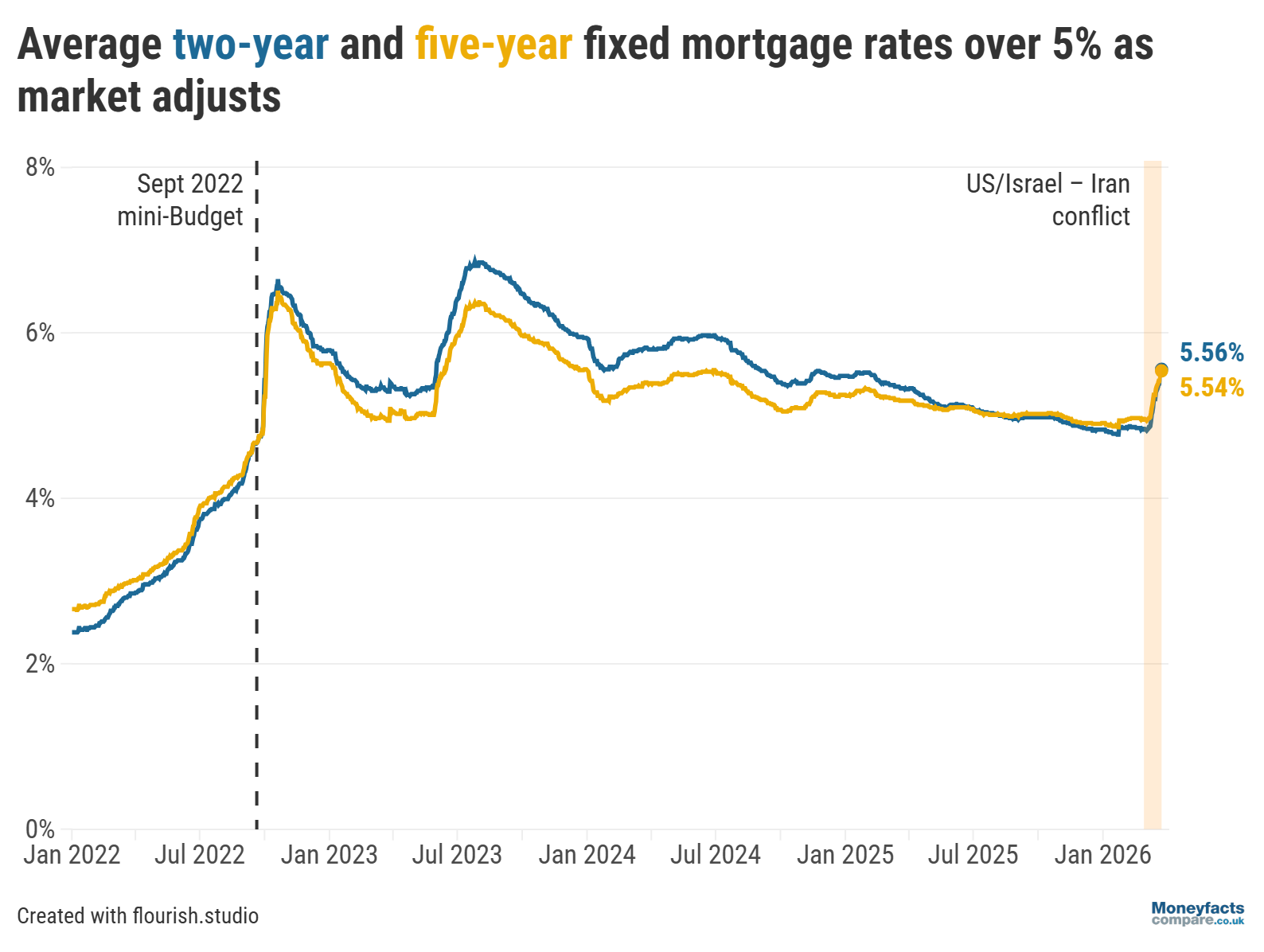

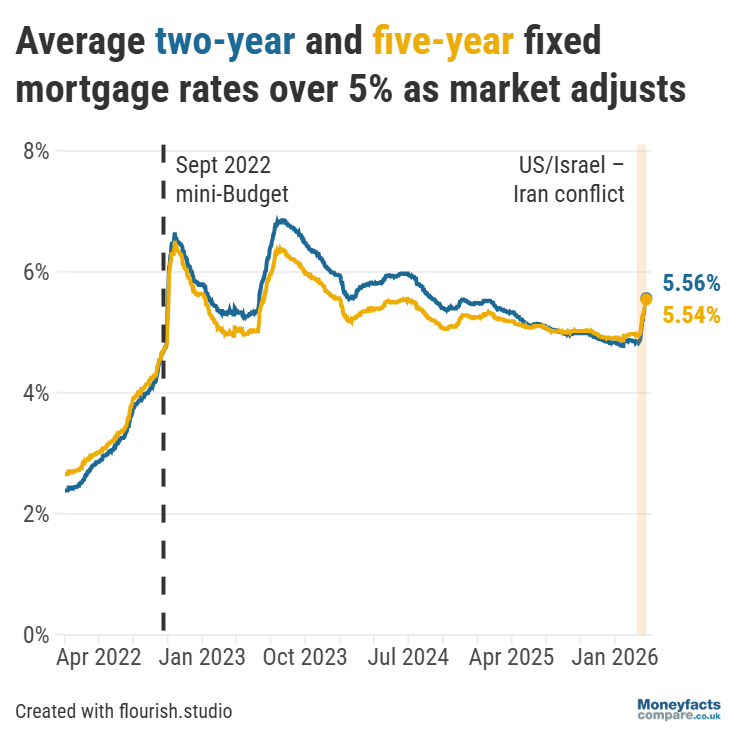

Fixed mortgage rates have rocketed since the start of the conflict and, underlining the volatility in the market, today (25 March 2026) saw the average two-year fixed mortgage rate jump above the average five-year fixed mortgage rate, according to latest Moneyfacts’ data.

The average two-year fixed mortgage now stands at 5.56% (up from 4.83% at the start of this month), while the typical rate charged by a five-year fixed deal is now at 5.54% (compared to 4.95% at the start of March).

“In a traditional market, the average two-year fixed deal would be lower than the five-year, but the unrest in the Middle East is causing concerns over the path of interest rate setting, with inflation expected to spike in the months ahead,” Rachel Springall, Finance Expert at Moneyfactscompare.co.uk, explained.

“Swap rates have been inverted for a few days now,” she added, which meant that it was only a matter of time before this was reflected in mortgage pricing.

Latest UK mortgage trends: Graph showing the average two-year and five-year fixed mortgage rates between January 2022 and March 2026.

While some may hope this will be a “temporary blip”, Springall points out that it will depend on how long the current volatility continues and how the markets expect the Bank of England base rate to change.

The average two-year fixed mortgage rate soared above the average five-year fixed rate after the fall-out from the September 2022 mini-Budget. This inversion remained for around three years, as it wasn’t until August 2025 that the average two-year fixed rate finally dropped below the average five-year rate, signalling a return to a more “traditional” market.

In addition to rising rates, lenders have withdrawn more than 1,500 mortgage products since 9 March 2026, which is roughly equivalent to a fifth of the overall market, Moneyfacts’ data revealed. This means borrowers now have fewer than 6,000 mortgages to choose from.

On 21 March alone, product choice fell by 448 deals – the highest amount in a single day since the aftermath of the September 2022 mini-Budget.

Even though product numbers showed a slight recovery between 24 and 25 March, Springall notes that, when products return to the market, “they will likely be at inflated rates to catch up with the current state of play”.

First-time buyers have been hit particularly hard by the recent volatility, as the average two-year fixed rate on deals at 95% loan-to-value (LTV) has soared above 6%.

Springall calculates that, for those taking out a two-year fix now compared to the start of March, this hike in rates could add around £1,200 per year to their mortgage repayments. This is based on a mortgage of £250,000 with a 25-year term, with a two-year fixed interest rate of 6.10% vs. 5.45%.

In a further blow to those looking to get on the property ladder, more than 200 deals at the 95% LTV tier have been withdrawn since 6 March 2026. On Saturday 21 March alone, 52 deals were pulled, marking the biggest daily fall in product numbers at this tier since the mini-Budget.

There are many factors that influence mortgage pricing, but the Bank of England base rate and swap market perhaps have the most sway.

The base rate is the amount of interest the Bank of England charges commercial banks, building societies and other financial institutions to borrow money which, in turn, affects how these organisations price their mortgages and savings products.

As such, raising the base rate can help to lessen demand during times of high inflation (by rewarding saving and making it more expensive to borrow money). By contrast, lowering the base rate could stimulate economic growth (by making borrowing cheaper to encourage spending). Learn more about the base rate.

As recently as last month, there were expectations that the Bank of England would cut the base rate this year which might have helped to push down borrowing costs. However, these have since given way to the possibility of interest rate hikes – particularly if disruption to global oil supplies causes UK inflation to rise.

“Mortgage rates have historically averaged around 1.5 percentage points above base rate. If markets continue to price in one or two rate rises, this could see average new mortgage rates stabilise at around 5.50% to 5.75%,” explained French, referring to recent analysis of Moneyfacts data. Based on these figures, borrowers could end up paying between £1,000 and £1,500 more per year on a typical £250,000 mortgage.

“While a quicker resolution to the conflict could ease some of [the] pressure on rates, the reality is that a more volatile world is a more expensive world,” said French. “Even though the most competitive deals will remain below average, anyone looking to buy or remortgage this year needs to prepare for higher costs than previously expected,” he added.

Mortgage brokers remove a lot of the paperwork and hassle of getting a mortgage, as well as helping you access exclusive products and rates that aren’t available to the public. Mortgage brokers are regulated by the Financial Conduct Authority (FCA) and are required to pass specific qualifications before they can give you advice.

MAB is the preferred mortgage broker of Moneyfactscompare.co.uk

![]()

Get friendly, expert advice free of charge as a visitor of Moneyfactscompare.co.uk

Mortgage Advice Bureau have 1,600 UK advisers with 200 awards between them.

Speak to an award-winning mortgage broker today.

Call 0800 031 8553 or request a callback

Mortgage Advice Bureau offers fee free mortgage advice for Moneyfactscompare.co.uk visitors that call on 0800 031 8553. If you contact Mortgage Advice Bureau outside of these channels you may incur a fee of up to 1%. Lines are open Monday to Friday 8am to 8pm and Saturday 9am to 1pm excluding bank holidays. Calls may be recorded.

Your home may be repossessed if you do not keep up repayments on your mortgage.

Although mortgage rates (on-the-whole) are rising, there are still plenty of deals charging below-average prices. Visit our regularly-updated mortgage charts to discover some of the lowest rates currently available.

But, bear in mind that the cheapest-priced deal may not be the most cost-effective for your needs and circumstances. That’s why our weekly mortgage roundup features some Moneyfacts Best Buy alternatives based on their overall true cost - as well as some of the week’s lowest fixed rates.

All of our newsletters are available free by email to all Moneyfactscompare.co.uk users.

Send me Weekend Moneyfactscompare, Savers Friend, and Companies Friend.

Information is correct as of the date of publication (shown at the top of this article). Any products featured may be withdrawn by their provider or changed at any time. Links to third parties on this page are paid for by the third party. You can find out more about the individual products by visiting their site. Moneyfactscompare.co.uk will receive a small payment if you use their services after you click through to their site. All information is subject to change without notice. Please check all terms before making any decisions. This information is intended solely to provide guidance and is not financial advice. Moneyfacts will not be liable for any loss arising from your use or reliance on this information. If you are in any doubt, Moneyfacts recommends you obtain independent financial advice.

Moneyfactscompare.co.uk will never contact you by phone to sell you any financial product. Any calls like this are not from Moneyfacts. Emails sent by Moneyfactscompare.co.uk will always be from news@moneyfacts-news.co.uk. Be ScamSmart.

Moneyfactscompare.co.uk will never contact you by phone to sell you any financial product. Any calls like this are not from Moneyfacts. Emails sent by Moneyfactscompare.co.uk will always be from news@moneyfacts-news.co.uk. Be ScamSmart.

Moneyfactscompare.co.uk will never contact you by phone to sell you any financial product. Any calls like this are not from Moneyfacts. Emails sent by Moneyfactscompare.co.uk will always be from news@moneyfacts-news.co.uk. Be ScamSmart.

Moneyfactscompare.co.uk will never contact you by phone to sell you any financial product. Any calls like this are not from Moneyfacts. Emails sent by Moneyfactscompare.co.uk will always be from news@moneyfacts-news.co.uk. Be ScamSmart.

Moneyfactscompare.co.uk will never contact you by phone to sell you any financial product. Any calls like this are not from Moneyfacts. Emails sent by Moneyfactscompare.co.uk will always be from news@moneyfacts-news.co.uk. Be ScamSmart.

Moneyfactscompare.co.uk will never contact you by phone to sell you any financial product. Any calls like this are not from Moneyfacts. Emails sent by Moneyfactscompare.co.uk will always be from news@moneyfacts-news.co.uk. Be ScamSmart.