Borrowers are warned that political volatility could lead to higher interest rates.

Speaking outside Downing Street earlier today, Sir Keir Starmer announced he will be stepping down as Prime Minister after nearly two years in charge. But, with his successor set to be the country’s seventh leader in just 10 years, should UK households be worried about the effects of more upheaval on their finances?

“A departing Prime Minister rarely changes your finances overnight,” reassured Charlotte Kennedy, Chartered Financial Planner at wealth management company, Rathbones, but added that it can “create uncertainty that affects markets, confidence and expectations”.

According to Adam French, Head of Consumer Finance at Moneyfactscompare.co.uk, there has been a “fairly muted response so far” to news of the resignation. However, he explained that money markets had already priced in a fresh wave of political uncertainty following last week’s by-election results (which saw frontrunner to replace Starmer, Andy Burnham, elected as MP for Makerfield).

“While Andy Burnham appears to be in pole position to take the helm, whoever ultimately takes power will inherit the same difficult fiscal backdrop and quickly discover there are no easy wins,” said Kennedy.

“The UK faces a challenging set of public finance constraints, with limited room for additional spending and persistent questions about how future commitments will be funded. Fears remain that spending cuts, tax rises or a bitter cocktail of both could be required to pay for any flagship policies,” she continued.

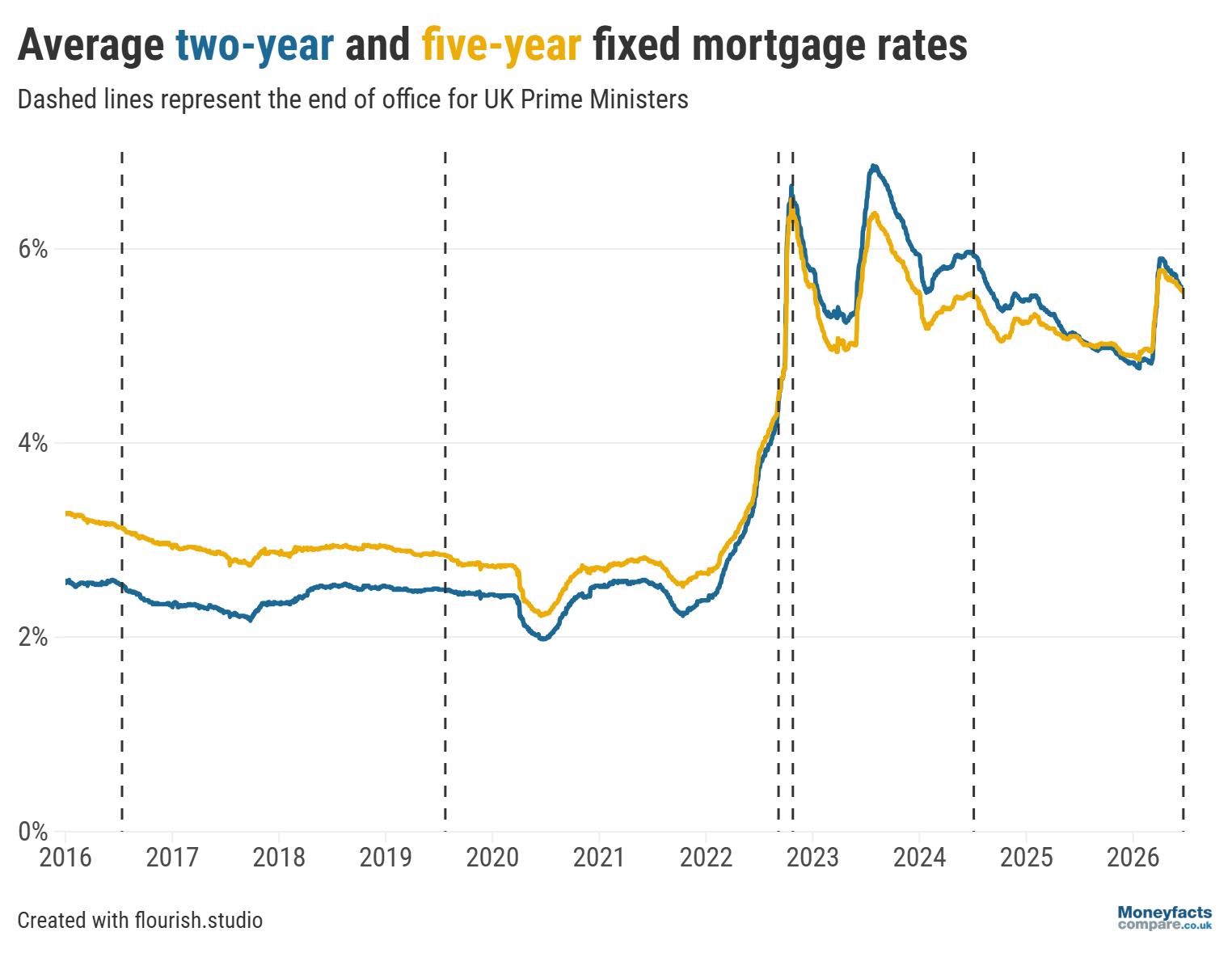

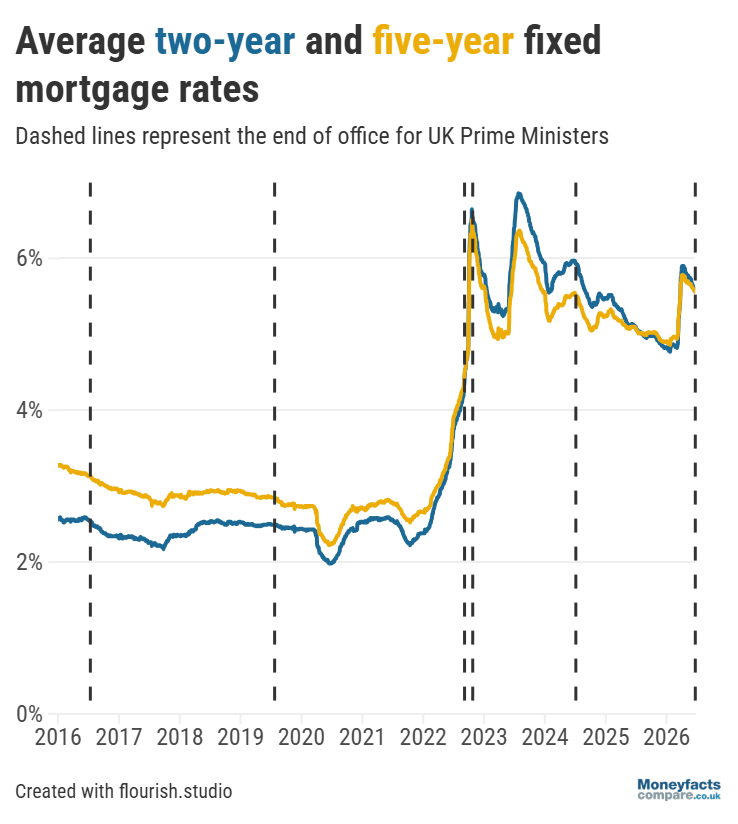

With the mortgage market only recently showing signs of recovering from the impact of conflict in the Middle East, borrowers may feel concerned that more turbulence could see interest rates trend upwards again.

“Episodes of political volatility tend to push up borrowing costs,” said French, explaining that this is due to the greater perceived risk to lenders. However, he added that whether (and how far) interest rates will climb in the coming months highly depends on the fiscal policies proposed by those vying for the leadership position.

UK Mortgage Trends: Graph showing average two- and five-year fixed mortgage rates over the past 10 years.

Our mortgage charts are regularly updated throughout the day so you can easily find the latest rates currently available.

However, it’s important to bear in mind that the deal charging the cheapest rate may not be the most suitable for your needs and circumstances. That’s why our weekly roundup includes alternative options that earn spots on our Moneyfacts Best Buy charts based on their overall true cost, as well as providing a summary of some of the lowest fixed mortgage rates.

“The lessons of the 2022 mini-Budget remain fresh. Fiscal headroom is tight and money markets will be watching the UK closely. If plans don’t add up, the subsequent loss of confidence can quickly drive up borrowing costs,” French continued.

Fortunately, he explained there are steps borrowers can take to reduce the risk of being caught out if interest rates were to rise. “Many lenders allow borrowers to secure a new deal up to six months before their current mortgage ends, providing valuable protection should uncertainty push rates higher in the meantime,” said French. “If rates do fall, borrowers can usually switch to a cheaper deal before completion without penalty,” he added.

Those unsure about the best course of action might find it useful to speak to a mortgage broker.

Speak to an award-winning mortgage broker today

MAB is the preferred mortgage broker of Moneyfactscompare.co.uk

![]()

Get friendly, expert advice free of charge as a visitor of Moneyfactscompare.co.uk

Mortgage Advice Bureau have 1,600 UK advisers with 200 awards between them.

Speak to an award-winning mortgage broker today.

Call 0800 031 8553 or request a callback

Mortgage Advice Bureau offers fee free mortgage advice for Moneyfactscompare.co.uk visitors that call on 0800 031 8553. If you contact Mortgage Advice Bureau outside of these channels you may incur a fee of up to 1%. Lines are open Monday to Friday 8am to 8pm and Saturday 9am to 1pm excluding bank holidays. Calls may be recorded.

Your home may be repossessed if you do not keep up repayments on your mortgage.

All of our newsletters are available free by email to all Moneyfactscompare.co.uk users.

Send me Weekend Moneyfactscompare, Savers Friend, and Companies Friend.

Information is correct as of the date of publication (shown at the top of this article). Any products featured may be withdrawn by their provider or changed at any time. Links to third parties on this page are paid for by the third party. You can find out more about the individual products by visiting their site. Moneyfactscompare.co.uk will receive a small payment if you use their services after you click through to their site. All information is subject to change without notice. Please check all terms before making any decisions. This information is intended solely to provide guidance and is not financial advice. Moneyfacts will not be liable for any loss arising from your use or reliance on this information. If you are in any doubt, Moneyfacts recommends you obtain independent financial advice.

Moneyfactscompare.co.uk will never contact you by phone to sell you any financial product. Any calls like this are not from Moneyfacts. Emails sent by Moneyfactscompare.co.uk will always be from news@moneyfacts-news.co.uk. Be ScamSmart.

Moneyfactscompare.co.uk will never contact you by phone to sell you any financial product. Any calls like this are not from Moneyfacts. Emails sent by Moneyfactscompare.co.uk will always be from news@moneyfacts-news.co.uk. Be ScamSmart.

Moneyfactscompare.co.uk will never contact you by phone to sell you any financial product. Any calls like this are not from Moneyfacts. Emails sent by Moneyfactscompare.co.uk will always be from news@moneyfacts-news.co.uk. Be ScamSmart.

Moneyfactscompare.co.uk will never contact you by phone to sell you any financial product. Any calls like this are not from Moneyfacts. Emails sent by Moneyfactscompare.co.uk will always be from news@moneyfacts-news.co.uk. Be ScamSmart.

Moneyfactscompare.co.uk will never contact you by phone to sell you any financial product. Any calls like this are not from Moneyfacts. Emails sent by Moneyfactscompare.co.uk will always be from news@moneyfacts-news.co.uk. Be ScamSmart.

Moneyfactscompare.co.uk will never contact you by phone to sell you any financial product. Any calls like this are not from Moneyfacts. Emails sent by Moneyfactscompare.co.uk will always be from news@moneyfacts-news.co.uk. Be ScamSmart.