While the outlook for savers is optimistic, do inflation risks threaten to derail real returns?

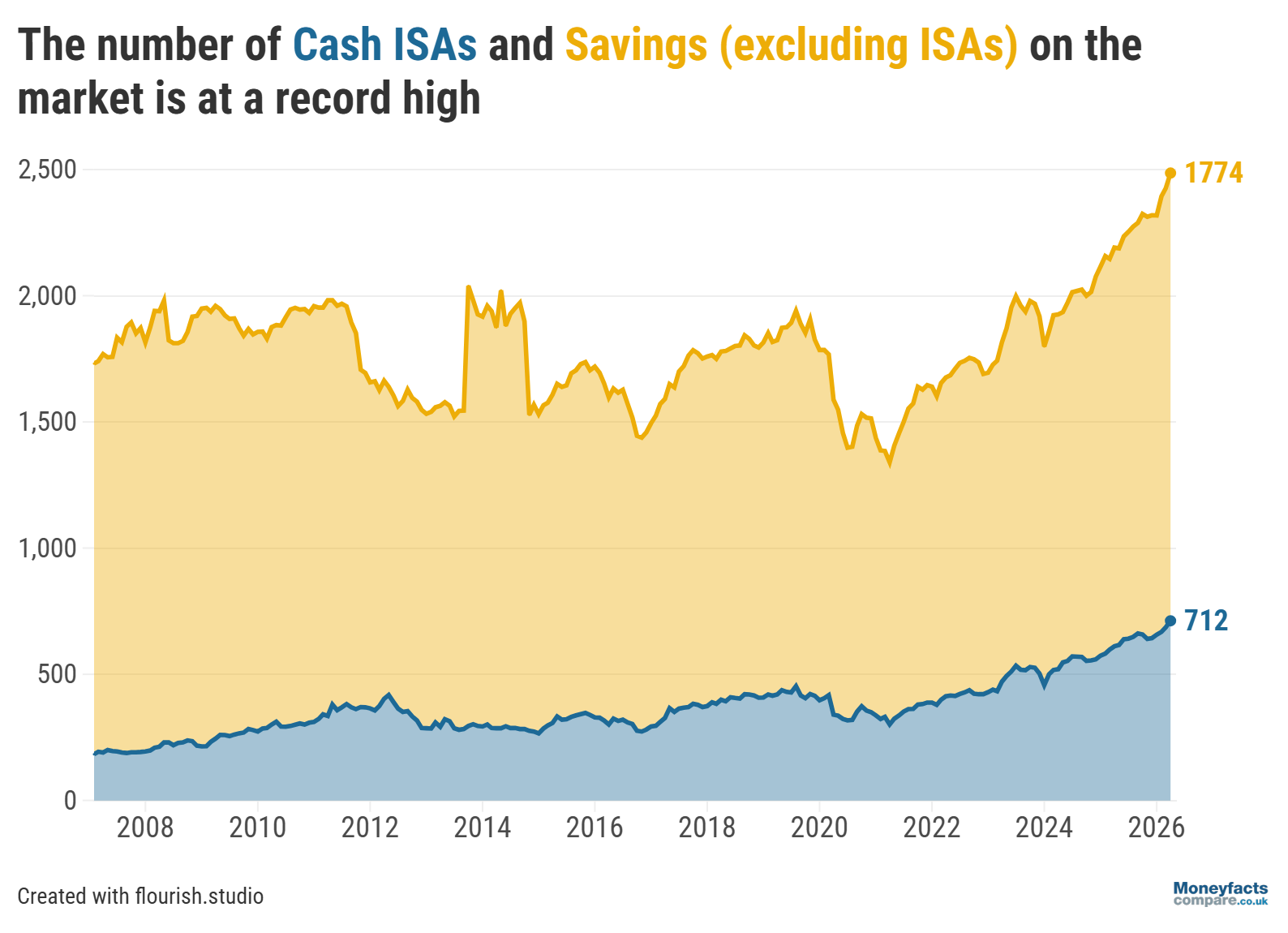

Off the back of providers hiking rates to attract deposits, likely due to the impending changes to the ISA allowance limit from April 2027, the number of cash ISA deals on the market rose to a record-breaking 712 at the start of April, the latest Moneyfacts UK Savings Treasury Report revealed. This is its largest monthly rise since May 2024.

And with ISA deals at a record high, savers looking to maximise their returns have an array of competitive options for the new tax-year.

From April 2027, the amount savers can put into cash ISAs will be cut from £20,000 to £12,000 for those under 65. Savers aged 65 and over will still be able to deposit £20,000 into cash ISAs per tax-year.

“Savers should be taking advantage of this all-time high, and it may be especially timely as the new tax-year is the perfect window to review their current deal and switch to ensure they can maximise their returns before thresholds tighten,” Caitlyn Eastell, Personal Finance Analyst at Moneyfacts, commented.

Graph: The number of Cash ISAs on the market compared to the number of savings accounts from 2008 to 2026.

With an unprecedented number of cash ISAs available, and providers having battled it out to top the charts, the average ISA rates have also climbed.

The average easy access ISA rate increased month-on-month by its biggest margin since October 2023 to 2.73%. Elsewhere, savers who want to lock in a guaranteed rate will find the average one-year fixed ISA rose to 4.01% - the highest it’s been since May 2025 – and the average longer-term fixed ISA hit 3.98% (its highest in a year).

What’s more, the number of savings accounts (excluding ISAs) available also saw a significant rise to 1,774 deals – the highest number on record. And the number of accounts paying above the Bank of England base rate (3.75%) has leaped to its highest level since December 2021.

“Markets have pivoted from the rate cut mindset seen earlier this year to a ‘higher for longer’ stance, or even potential rises, as the ongoing tensions in the Middle East threaten a fresh inflationary shock,” Eastell remarked.

This is reflected in fixed rate bonds, with the average one-year bond seeing its biggest monthly increase since September 2023.

While savers may feel reassured that they could secure more competitive rates, Eastell warned that “it can be a tricky balancing act because sharp spikes to household bills and inflation could quickly catch up, meaning savers may be left out of pocket”.

So, while rates could be on the rise, daily costs could be too, seeing our savings erode in real terms (meaning our money is able to buy less).

This makes it more important than ever to review – and switch – your accounts. Searching the market for attractive deals can help to protect your money from any potential rises to inflation.

Head to our dedicated savings and ISA charts to compare the highest rates on the market. Alternatively, see our weekly savings and ISA roundups for a more detailed overview. Or subscribe to our Savers Friend newsletter to get updates on the latest savings changes delivered straight into your inbox.

All of our newsletters are available free by email to all Moneyfactscompare.co.uk users.

Send me Weekend Moneyfactscompare, Savers Friend, and Companies Friend.

Information is correct as of the date of publication (shown at the top of this article). Any products featured may be withdrawn by their provider or changed at any time. Links to third parties on this page are paid for by the third party. You can find out more about the individual products by visiting their site. Moneyfactscompare.co.uk will receive a small payment if you use their services after you click through to their site. All information is subject to change without notice. Please check all terms before making any decisions. This information is intended solely to provide guidance and is not financial advice. Moneyfacts will not be liable for any loss arising from your use or reliance on this information. If you are in any doubt, Moneyfacts recommends you obtain independent financial advice.

Moneyfactscompare.co.uk will never contact you by phone to sell you any financial product. Any calls like this are not from Moneyfacts. Emails sent by Moneyfactscompare.co.uk will always be from news@moneyfacts-news.co.uk. Be ScamSmart.

Moneyfactscompare.co.uk will never contact you by phone to sell you any financial product. Any calls like this are not from Moneyfacts. Emails sent by Moneyfactscompare.co.uk will always be from news@moneyfacts-news.co.uk. Be ScamSmart.

Moneyfactscompare.co.uk will never contact you by phone to sell you any financial product. Any calls like this are not from Moneyfacts. Emails sent by Moneyfactscompare.co.uk will always be from news@moneyfacts-news.co.uk. Be ScamSmart.

Moneyfactscompare.co.uk will never contact you by phone to sell you any financial product. Any calls like this are not from Moneyfacts. Emails sent by Moneyfactscompare.co.uk will always be from news@moneyfacts-news.co.uk. Be ScamSmart.

Moneyfactscompare.co.uk will never contact you by phone to sell you any financial product. Any calls like this are not from Moneyfacts. Emails sent by Moneyfactscompare.co.uk will always be from news@moneyfacts-news.co.uk. Be ScamSmart.

Moneyfactscompare.co.uk will never contact you by phone to sell you any financial product. Any calls like this are not from Moneyfacts. Emails sent by Moneyfactscompare.co.uk will always be from news@moneyfacts-news.co.uk. Be ScamSmart.