Overall product choice has reached a new record high – with more than half of accounts paying above the base rate.

Savers who let their money languish in low-paying accounts are being warned that they risk missing out on hundreds of pounds in potential interest as competition remains fierce among providers.

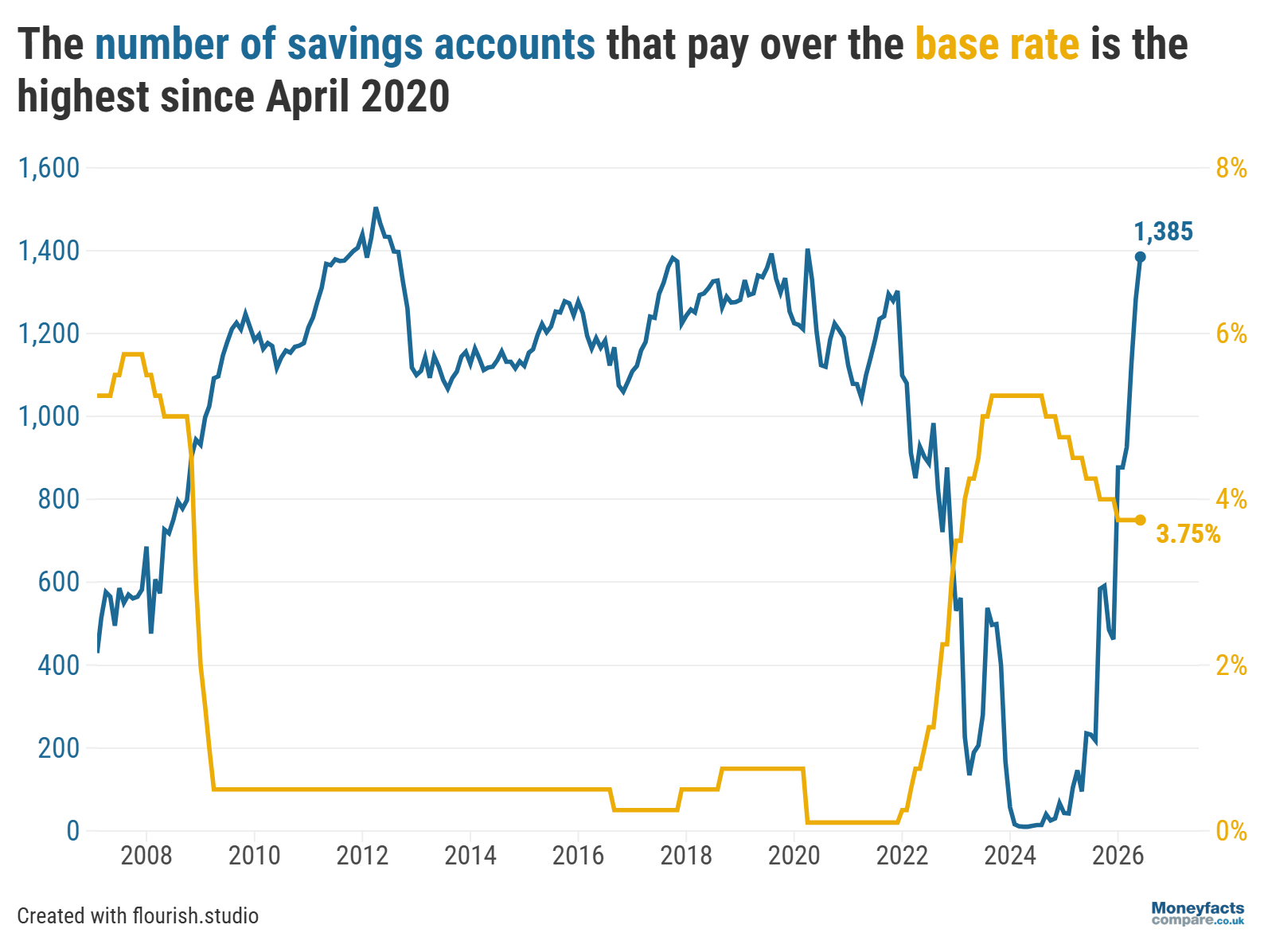

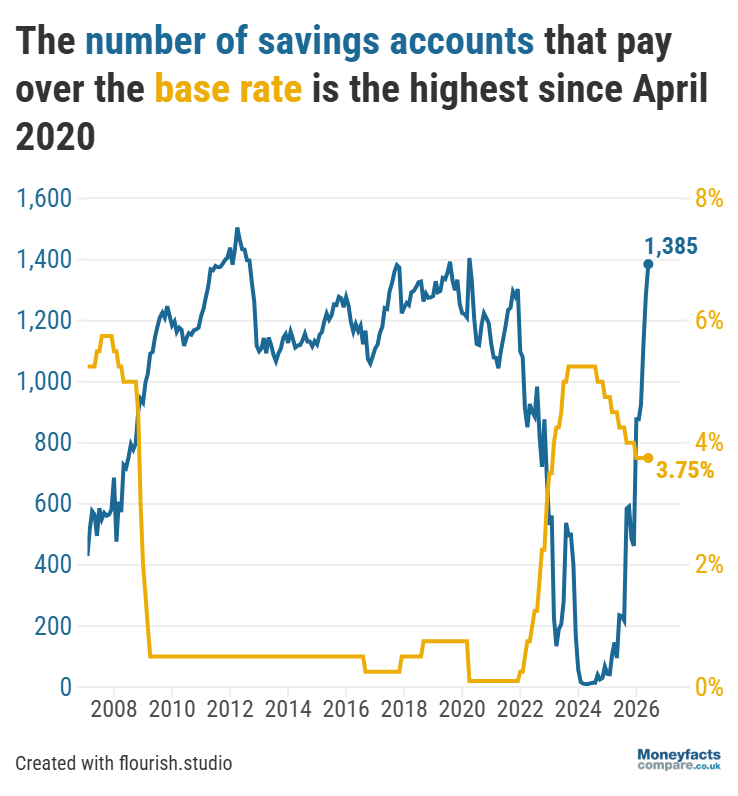

With many banks and building societies launching new savings accounts in recent weeks, overall product choice reached another record high for a sixth consecutive month – rising to 2,583 by the start of July, according to data from the latest Moneyfacts UK Savings Trends Treasury Report. What’s more, over half of accounts pay above the current Bank of England base rate (3.75%)* – with this figure increasing to 1,385 month-on-month (its highest in over six years).

UK Savings Trends: Number of savings accounts paying above the Bank of England base rate between 2008 and 2026.

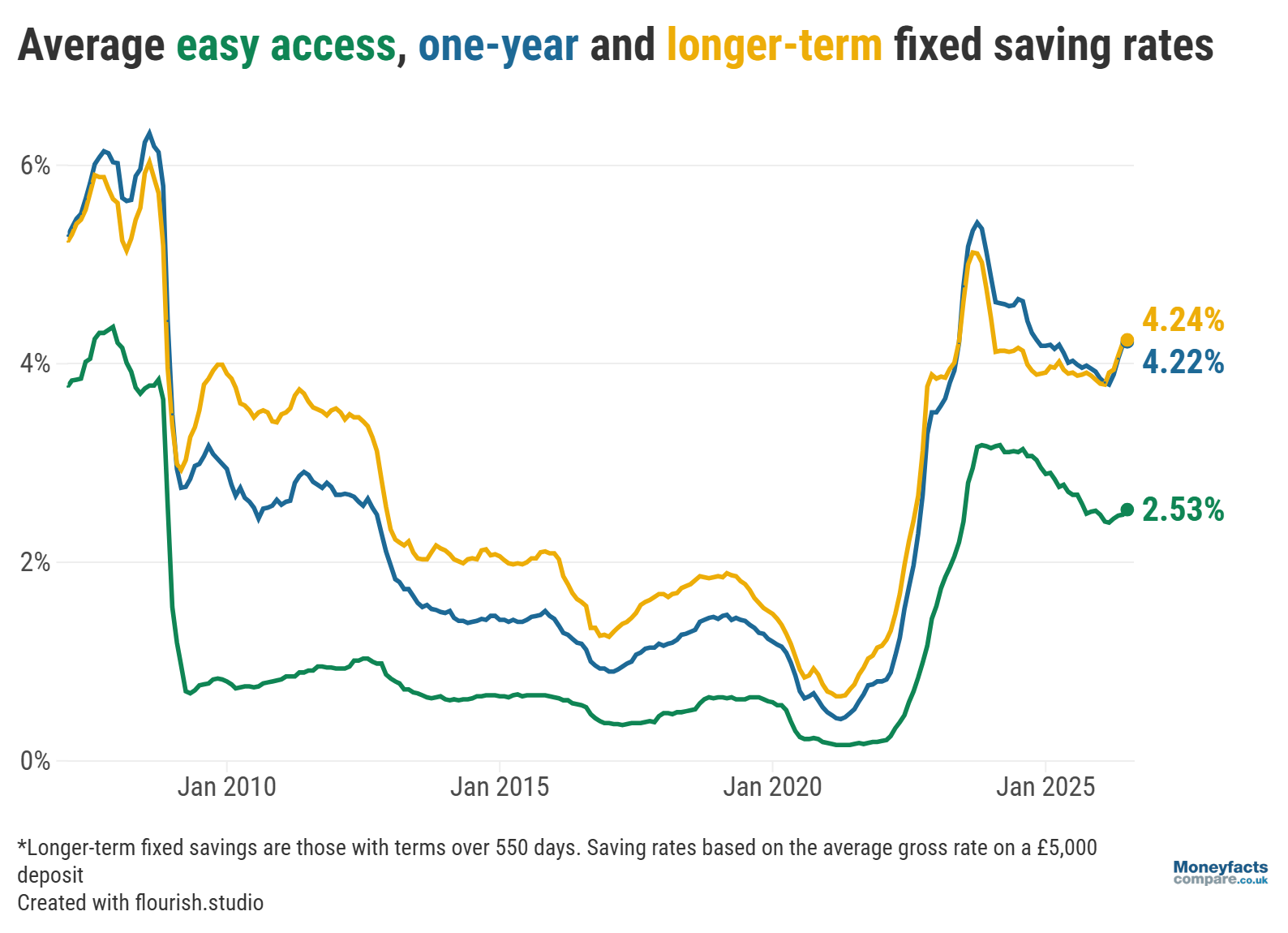

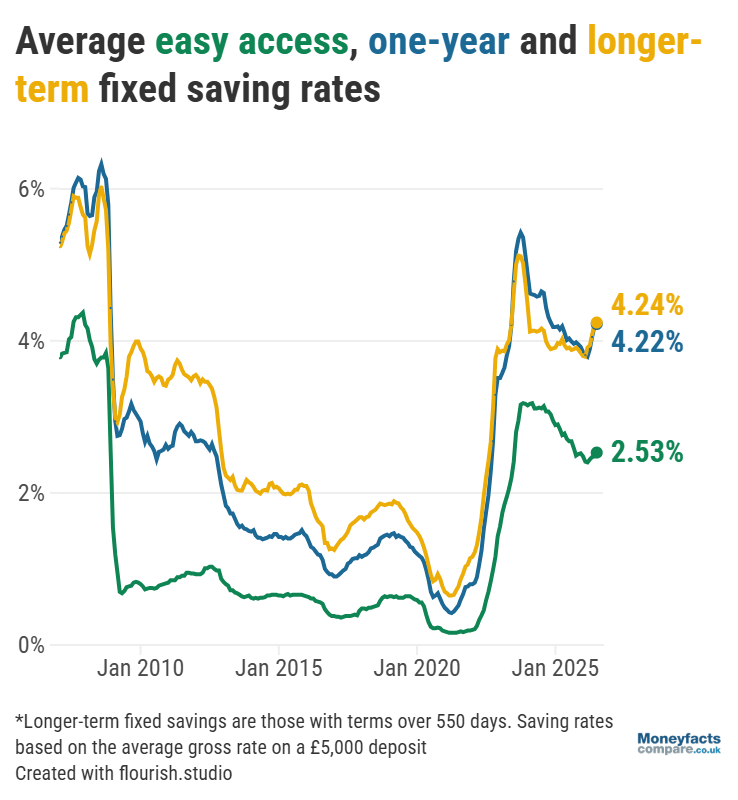

The combination of new products being launched and providers actively improving rates has also seen average returns on savings accounts (excluding ISAs) continue to climb between June and July. The typical easy access savings rate, for instance, rose from 2.48% to 2.53% month-on-month (its highest in almost a year), while the average notice savings rate increased from 3.36% to 3.40% over the same timeframe.

But, despite the positive momentum, new research from LHV Bank worryingly uncovered that over half (53%) of UK savers aren’t confident they’re earning a competitive return – meaning many might be being short-changed by a paltry savings rate.

Fortunately, there are steps savers can take which could help them get more for their money.

“The current condition of the savings market strongly favours active savers. Regularly reviewing and switching accounts can make a meaningful difference to how quickly savings grow, helping savers benefit from the most competitive rates available,” said Caitlyn Eastell, Personal Finance Analyst at Moneyfactscompare.co.uk.

She encouraged savers to look beyond average rates, explaining that someone with £10,000 stashed in a typical easy access account might earn just £253 in interest over the course of a year (in contrast to around £500 in a top-paying account). “On larger balances, the benefit of switching becomes even more significant,” she added.

Alternatively, those who don’t need immediate access to their cash could consider locking it away in a fixed account to safeguard against the possibility of interest rates falling in the future. Average returns on a one-year bond rose from 4.19% to 4.22% in the month to July, while the typical rate paid by a longer-term bond (of over 550 days) went up from 4.21% to 4.24% during this time. In both cases, this marks five months of consecutive increases and the highest rates since 2024.

UK Savings Trends: Average rates paid by easy access accounts, one-year fixed bonds and longer-term bonds between 2008 and 2026.

Our savings and ISA charts are updated every day between 9am and 5pm so you can easily find the best rates currently available.

Also check out our weekly savings and ISA roundups for more information on some of the most competitive accounts, or subscribe for free to our Savers Friend newsletter for regular updates from across the savings market.

*Based on a £5,000 deposit.

All of our newsletters are available free by email to all Moneyfactscompare.co.uk users.

Send me Weekend Moneyfactscompare, Savers Friend, and Companies Friend.

Information is correct as of the date of publication (shown at the top of this article). Any products featured may be withdrawn by their provider or changed at any time. Links to third parties on this page are paid for by the third party. You can find out more about the individual products by visiting their site. Moneyfactscompare.co.uk will receive a small payment if you use their services after you click through to their site. All information is subject to change without notice. Please check all terms before making any decisions. This information is intended solely to provide guidance and is not financial advice. Moneyfacts will not be liable for any loss arising from your use or reliance on this information. If you are in any doubt, Moneyfacts recommends you obtain independent financial advice.

Moneyfactscompare.co.uk will never contact you by phone to sell you any financial product. Any calls like this are not from Moneyfacts. Emails sent by Moneyfactscompare.co.uk will always be from news@moneyfacts-news.co.uk. Be ScamSmart.

Moneyfactscompare.co.uk will never contact you by phone to sell you any financial product. Any calls like this are not from Moneyfacts. Emails sent by Moneyfactscompare.co.uk will always be from news@moneyfacts-news.co.uk. Be ScamSmart.

Moneyfactscompare.co.uk will never contact you by phone to sell you any financial product. Any calls like this are not from Moneyfacts. Emails sent by Moneyfactscompare.co.uk will always be from news@moneyfacts-news.co.uk. Be ScamSmart.

Moneyfactscompare.co.uk will never contact you by phone to sell you any financial product. Any calls like this are not from Moneyfacts. Emails sent by Moneyfactscompare.co.uk will always be from news@moneyfacts-news.co.uk. Be ScamSmart.

Moneyfactscompare.co.uk will never contact you by phone to sell you any financial product. Any calls like this are not from Moneyfacts. Emails sent by Moneyfactscompare.co.uk will always be from news@moneyfacts-news.co.uk. Be ScamSmart.

Moneyfactscompare.co.uk will never contact you by phone to sell you any financial product. Any calls like this are not from Moneyfacts. Emails sent by Moneyfactscompare.co.uk will always be from news@moneyfacts-news.co.uk. Be ScamSmart.