Air fares made the largest upwards contribution as average motor fuel prices fell.

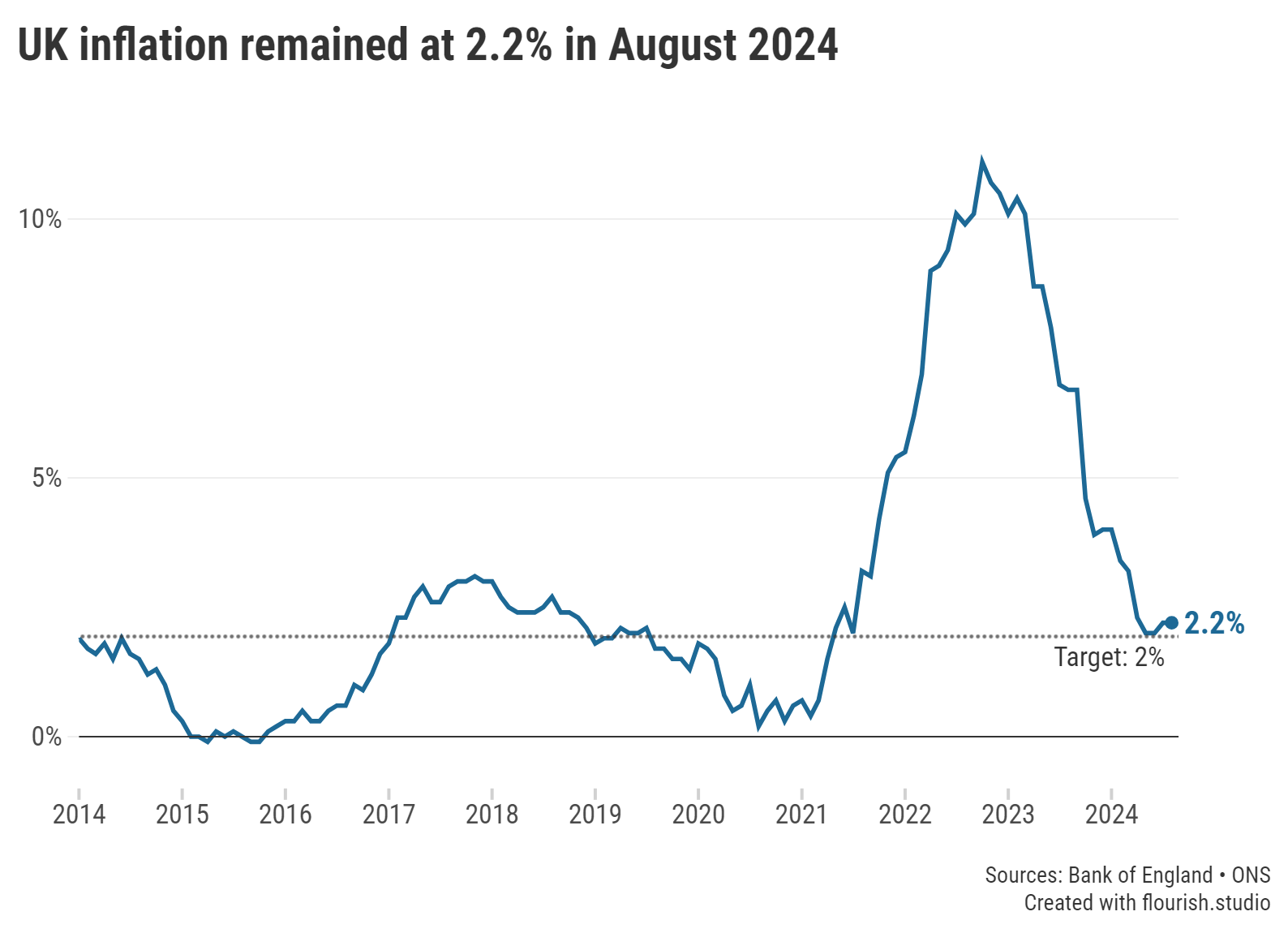

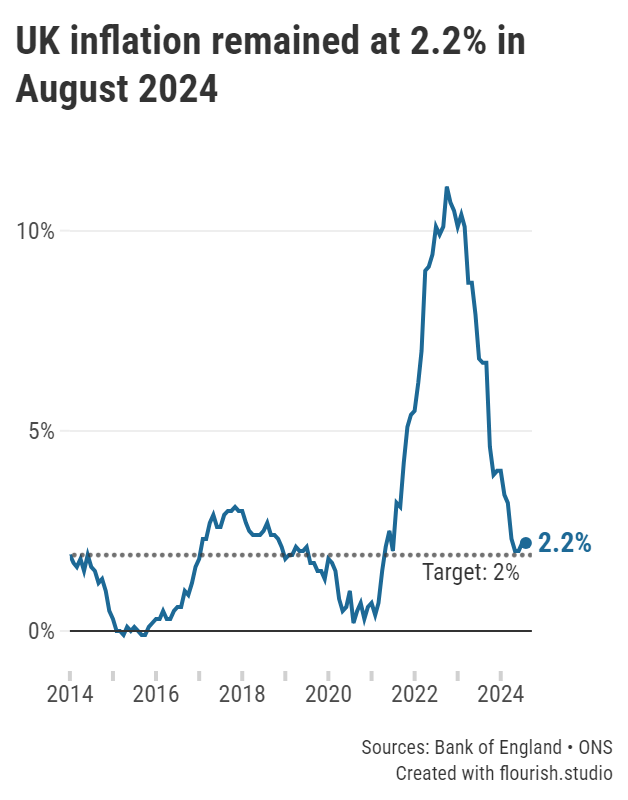

UK inflation remained at 2.2% in the year to August 2024, according to figures released today by the Office for National Statistics (ONS). This means, on the whole, prices of goods and services increased at the same rate as in the year to July.

Inflation is a significant factor for the Bank of England’s Monetary Policy Committee (MPC) when deciding whether to raise or lower the base rate.

With the rate of inflation now holding steady, this could delay any potential changes to the base rate until later in the year.

Inflation shows how quickly, or slowly, the prices of goods and services have risen over the past year. The Consumer Price Index (CPI) is the key metric used to calculate the rate of inflation.

Keep in mind that, while the rate of inflation has gone unchanged in August, prices are still higher compared to the previous year.

Graph: Inflation held at 2.2% in August.

Transport made a significant upwards contribution to inflation, with air fares in particular rising by 22.2% between July and August.

While the price of air travel is naturally expected to increase over the summer months, this marks the second largest rise since the ONS began its monthly collection of prices in 2001.

This is in contrast to a year ago, when air fares fell by 2.1% between July and August 2023. The only other time prices in this sector fell during these months was during 2020 amid the COVID- 19 pandemic.

Falling motor fuel costs helped to quell a consecutive rise in inflation, with average petrol prices dropping to 142.3 pence per litre between July and August. The price of diesel also fell in the same period to stand at 147.8 pence per litre.

Overall, this saw motor fuel prices drop by 3.4% in the year to August, compared with a rise of 1.8% in the year to July.

Otherwise, the service sector also helped keep inflation down; the annual rate for restaurants and hotels rose by 4.4% in the year to August, slowing from the 4.9% rise in the year to July. This was largely driven by the price of alcohol products in pubs and restaurants rising less than a year ago.

The majority of top rates have seen significant falls since the previous inflation announcement, with fixed ISA and non-ISA accounts taking the biggest hits. Providers have been busy passing on the reduction in interest rates to their savings deals, so it would be wise to grab a market-leading rate while there are still some sitting around the 5% mark.

Fixed bonds are continuing to follow a downward trend, particularly one-year fixed bonds and their ISA counterparts. Savers can now expect over 1% less interest than the leading rate in September 2023. Longer-term bonds have seen less drastic cuts; however, they are still worse month-on-month.

The gap between shorter- and longer-term savings is slowly beginning to close. Savers can receive a better return for a one- or two-year term but if they wish to beat inflation for longer it may be worth considering fixed bonds with a term of three or more years.

Following the reduction in the Bank of England base rate last month variable accounts have been under the spotlight but there are still some competitive accounts out there.

ISAs have also seen reductions across the board but continue to pay lower rates than their non-ISA alternatives.

Despite this, savers should not be deterred by the lower rates as they benefit from having a tax-free allowance, unlike a non-ISA where savers get a personal savings allowance (PSA) which they could breach. The top easy access ISA has dropped below the 5% mark, which may be disappointing news for investors looking for flexibility.

There are currently 1,606 savings accounts that now beat the rate of inflation. You can visit our charts to compare the top easy access savings accounts, fixed rate bonds and notice accounts.

All of our newsletters are available free by email to all Moneyfactscompare.co.uk users.

Send me Weekend Moneyfactscompare, Savers Friend, and Companies Friend.

Information is correct as of the date of publication (shown at the top of this article). Any products featured may be withdrawn by their provider or changed at any time. Links to third parties on this page are paid for by the third party. You can find out more about the individual products by visiting their site. Moneyfactscompare.co.uk will receive a small payment if you use their services after you click through to their site. All information is subject to change without notice. Please check all terms before making any decisions. This information is intended solely to provide guidance and is not financial advice. Moneyfacts will not be liable for any loss arising from your use or reliance on this information. If you are in any doubt, Moneyfacts recommends you obtain independent financial advice.

Moneyfactscompare.co.uk will never contact you by phone to sell you any financial product. Any calls like this are not from Moneyfacts. Emails sent by Moneyfactscompare.co.uk will always be from news@moneyfacts-news.co.uk. Be ScamSmart.

Moneyfactscompare.co.uk will never contact you by phone to sell you any financial product. Any calls like this are not from Moneyfacts. Emails sent by Moneyfactscompare.co.uk will always be from news@moneyfacts-news.co.uk. Be ScamSmart.

Moneyfactscompare.co.uk will never contact you by phone to sell you any financial product. Any calls like this are not from Moneyfacts. Emails sent by Moneyfactscompare.co.uk will always be from news@moneyfacts-news.co.uk. Be ScamSmart.

Moneyfactscompare.co.uk will never contact you by phone to sell you any financial product. Any calls like this are not from Moneyfacts. Emails sent by Moneyfactscompare.co.uk will always be from news@moneyfacts-news.co.uk. Be ScamSmart.

Moneyfactscompare.co.uk will never contact you by phone to sell you any financial product. Any calls like this are not from Moneyfacts. Emails sent by Moneyfactscompare.co.uk will always be from news@moneyfacts-news.co.uk. Be ScamSmart.

Moneyfactscompare.co.uk will never contact you by phone to sell you any financial product. Any calls like this are not from Moneyfacts. Emails sent by Moneyfactscompare.co.uk will always be from news@moneyfacts-news.co.uk. Be ScamSmart.