Best 5 Year Fixed Rate Bond Rates

We found 94 PRODUCTS in total, of which 27 are EASY TO OPEN

Afin Bank 5-Year Fixed Term Account (Issue 10)

In the UK, the first £120,000 of savings per person is protected by the Financial Services Compensation Scheme. Some banking brands share the same banking licence which means your deposit protection is across all brands sharing the licence. If you have also borrowed from the failed bank/building society, the compensation will not be reduced to repay your debt, separate arrangements will be made for this. The deposits of most businesses are covered up to the £120,000 limit, but businesses should check with their bank before they apply as there are exclusions.

Atom Bank 5 Year Fixed Saver

In the UK, the first £120,000 of savings per person is protected by the Financial Services Compensation Scheme. Some banking brands share the same banking licence which means your deposit protection is across all brands sharing the licence. If you have also borrowed from the failed bank/building society, the compensation will not be reduced to repay your debt, separate arrangements will be made for this. The deposits of most businesses are covered up to the £120,000 limit, but businesses should check with their bank before they apply as there are exclusions.

thisbank Fixed-Term Savings Account

In the UK, the first £120,000 of savings per person is protected by the Financial Services Compensation Scheme. Some banking brands share the same banking licence which means your deposit protection is across all brands sharing the licence. If you have also borrowed from the failed bank/building society, the compensation will not be reduced to repay your debt, separate arrangements will be made for this. The deposits of most businesses are covered up to the £120,000 limit, but businesses should check with their bank before they apply as there are exclusions.

4.65%

Fixed

5 Year Bond

Anniversary, Monthly

Online, Branch, Mail

Online, Branch, Mail

Secure steady, long‑term growth with our 5 Year Fixed Rate Bond.

For longer‑term goals - A steady home for savings you won’t need to access for a while.

Confidence in your plan - A fixed term gives you clarity and stability from day one.

Focused saving - Start with a lump sum of at least £1,000, with room to save up to £250,000.

Simple to get started - Open online, in branch, or by post, whatever suits you best.

Close Brothers Savings Fixed Rate Bond

In the UK, the first £120,000 of savings per person is protected by the Financial Services Compensation Scheme. Some banking brands share the same banking licence which means your deposit protection is across all brands sharing the licence. If you have also borrowed from the failed bank/building society, the compensation will not be reduced to repay your debt, separate arrangements will be made for this. The deposits of most businesses are covered up to the £120,000 limit, but businesses should check with their bank before they apply as there are exclusions.

Aldermore 5 Year Fixed Rate Savings Account

In the UK, the first £120,000 of savings per person is protected by the Financial Services Compensation Scheme. Some banking brands share the same banking licence which means your deposit protection is across all brands sharing the licence. If you have also borrowed from the failed bank/building society, the compensation will not be reduced to repay your debt, separate arrangements will be made for this. The deposits of most businesses are covered up to the £120,000 limit, but businesses should check with their bank before they apply as there are exclusions.

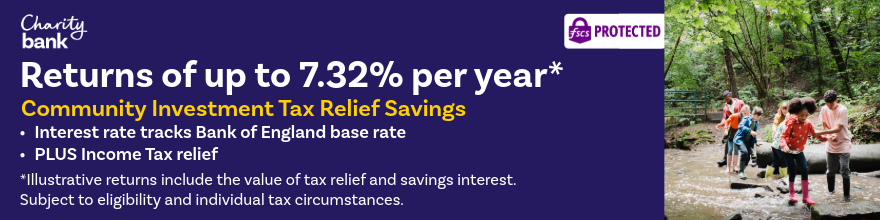

Unique to Charity Bank.

HMRC and Department of Business & Trade CITR scheme.

Leek Building Society 5 Year Fixed Rate Bond

In the UK, the first £120,000 of savings per person is protected by the Financial Services Compensation Scheme. Some banking brands share the same banking licence which means your deposit protection is across all brands sharing the licence. If you have also borrowed from the failed bank/building society, the compensation will not be reduced to repay your debt, separate arrangements will be made for this. The deposits of most businesses are covered up to the £120,000 limit, but businesses should check with their bank before they apply as there are exclusions.

Chetwood Bank HL Active Savings - 5 Year Fixed Term Deposit

In the UK, the first £120,000 of savings per person is protected by the Financial Services Compensation Scheme. Some banking brands share the same banking licence which means your deposit protection is across all brands sharing the licence. If you have also borrowed from the failed bank/building society, the compensation will not be reduced to repay your debt, separate arrangements will be made for this. The deposits of most businesses are covered up to the £120,000 limit, but businesses should check with their bank before they apply as there are exclusions.

Harpenden BS 5 Year Fixed Rate Bond (Issue 1)

In the UK, the first £120,000 of savings per person is protected by the Financial Services Compensation Scheme. Some banking brands share the same banking licence which means your deposit protection is across all brands sharing the licence. If you have also borrowed from the failed bank/building society, the compensation will not be reduced to repay your debt, separate arrangements will be made for this. The deposits of most businesses are covered up to the £120,000 limit, but businesses should check with their bank before they apply as there are exclusions.

RCI Bank UK 5 Year Fixed Term Savings Account

In the UK, the first £120,000 of savings per person is protected by the Financial Services Compensation Scheme. Some banking brands share the same banking licence which means your deposit protection is across all brands sharing the licence. If you have also borrowed from the failed bank/building society, the compensation will not be reduced to repay your debt, separate arrangements will be made for this. The deposits of most businesses are covered up to the £120,000 limit, but businesses should check with their bank before they apply as there are exclusions.

Yorkshire Building Society Fixed Rate eBond until 31 July 2031

In the UK, the first £120,000 of savings per person is protected by the Financial Services Compensation Scheme. Some banking brands share the same banking licence which means your deposit protection is across all brands sharing the licence. If you have also borrowed from the failed bank/building society, the compensation will not be reduced to repay your debt, separate arrangements will be made for this. The deposits of most businesses are covered up to the £120,000 limit, but businesses should check with their bank before they apply as there are exclusions.

Isbank Meteor Savings - 5 Year Fixed Term Deposit

In the UK, the first £120,000 of savings per person is protected by the Financial Services Compensation Scheme. Some banking brands share the same banking licence which means your deposit protection is across all brands sharing the licence. If you have also borrowed from the failed bank/building society, the compensation will not be reduced to repay your debt, separate arrangements will be made for this. The deposits of most businesses are covered up to the £120,000 limit, but businesses should check with their bank before they apply as there are exclusions.

Isbank Raisin UK - 5 Year Fixed Term Deposit

In the UK, the first £120,000 of savings per person is protected by the Financial Services Compensation Scheme. Some banking brands share the same banking licence which means your deposit protection is across all brands sharing the licence. If you have also borrowed from the failed bank/building society, the compensation will not be reduced to repay your debt, separate arrangements will be made for this. The deposits of most businesses are covered up to the £120,000 limit, but businesses should check with their bank before they apply as there are exclusions.

Skipton BS 5 Year Fixed Rate Bond (Issue 306.5)

In the UK, the first £120,000 of savings per person is protected by the Financial Services Compensation Scheme. Some banking brands share the same banking licence which means your deposit protection is across all brands sharing the licence. If you have also borrowed from the failed bank/building society, the compensation will not be reduced to repay your debt, separate arrangements will be made for this. The deposits of most businesses are covered up to the £120,000 limit, but businesses should check with their bank before they apply as there are exclusions.

Paragon Bank 5 Year Fixed Rate Savings Account

In the UK, the first £120,000 of savings per person is protected by the Financial Services Compensation Scheme. Some banking brands share the same banking licence which means your deposit protection is across all brands sharing the licence. If you have also borrowed from the failed bank/building society, the compensation will not be reduced to repay your debt, separate arrangements will be made for this. The deposits of most businesses are covered up to the £120,000 limit, but businesses should check with their bank before they apply as there are exclusions.

Hampshire Trust Bank 5 Year Online Fixed Saver (Issue 53)

In the UK, the first £120,000 of savings per person is protected by the Financial Services Compensation Scheme. Some banking brands share the same banking licence which means your deposit protection is across all brands sharing the licence. If you have also borrowed from the failed bank/building society, the compensation will not be reduced to repay your debt, separate arrangements will be made for this. The deposits of most businesses are covered up to the £120,000 limit, but businesses should check with their bank before they apply as there are exclusions.

Close Brothers Savings HL Active Savings - 5 Year Fixed Term Deposit

In the UK, the first £120,000 of savings per person is protected by the Financial Services Compensation Scheme. Some banking brands share the same banking licence which means your deposit protection is across all brands sharing the licence. If you have also borrowed from the failed bank/building society, the compensation will not be reduced to repay your debt, separate arrangements will be made for this. The deposits of most businesses are covered up to the £120,000 limit, but businesses should check with their bank before they apply as there are exclusions.

Perenna Raisin UK - 5 Year Fixed Term Deposit

In the UK, the first £120,000 of savings per person is protected by the Financial Services Compensation Scheme. Some banking brands share the same banking licence which means your deposit protection is across all brands sharing the licence. If you have also borrowed from the failed bank/building society, the compensation will not be reduced to repay your debt, separate arrangements will be made for this. The deposits of most businesses are covered up to the £120,000 limit, but businesses should check with their bank before they apply as there are exclusions.

Bank of Ceylon (UK) Raisin UK - 5 Year Fixed Term Deposit

In the UK, the first £120,000 of savings per person is protected by the Financial Services Compensation Scheme. Some banking brands share the same banking licence which means your deposit protection is across all brands sharing the licence. If you have also borrowed from the failed bank/building society, the compensation will not be reduced to repay your debt, separate arrangements will be made for this. The deposits of most businesses are covered up to the £120,000 limit, but businesses should check with their bank before they apply as there are exclusions.

Buckinghamshire BS Bucks Fixed Rate Bond Issue 237 to 31/05/2031

In the UK, the first £120,000 of savings per person is protected by the Financial Services Compensation Scheme. Some banking brands share the same banking licence which means your deposit protection is across all brands sharing the licence. If you have also borrowed from the failed bank/building society, the compensation will not be reduced to repay your debt, separate arrangements will be made for this. The deposits of most businesses are covered up to the £120,000 limit, but businesses should check with their bank before they apply as there are exclusions.

iFAST Global Bank Fixed Term Deposit

In the UK, the first £120,000 of savings per person is protected by the Financial Services Compensation Scheme. Some banking brands share the same banking licence which means your deposit protection is across all brands sharing the licence. If you have also borrowed from the failed bank/building society, the compensation will not be reduced to repay your debt, separate arrangements will be made for this. The deposits of most businesses are covered up to the £120,000 limit, but businesses should check with their bank before they apply as there are exclusions.

Eligible deposits with UK institutions are protected by the FSCS up to £120,000 per person per institution.

Who owns whom?

Find out which banks and savings account providers operate under which banking license with our who owns whom guide, helping savers work out to what degree their savings are protected by the FSCS.

Disclaimer*Data updated hourly, every day between 9am and 5pm.

Applicants must be a UK resident. All rates subject to change without notice. Please check all rates and terms before investing or borrowing.

Provider LinksLinks like ‘Go To Provider's Site’ or ‘Speak to a Broker’ connect you to providers or brokers we work with, for which we may receive a commission if you click or apply.

Favourites

Clicking the heart icon marks a product as a favourite for 14 days (if cookies are enabled), allowing you to filter and sort favourites at the top of the list.

Five-year fixed bonds are a type of savings account that offer an interest rate guaranteed to remain the same over a certain length of time in exchange for locking your money away (in this case, for five years).

Some five year bonds can be opened with as little as just £1, while others require a more substantial minimum deposit of £10,000 or more. Regardless of how much you’re looking to save, it’s important to consider your initial investment carefully as withdrawals typically aren’t allowed.

Depending on the specific account and provider, you’ll receive any returns on a regular basis (e.g. either monthly, yearly or on anniversary) or when the account matures - at which point you’ll regain access to your cash.

Many five-year fixed savings accounts accept deposits for a limited time after opening, but it’s not uncommon for some banks and building societies to impose greater restrictions (or prohibit further additions entirely).

Find out if you can add money to an account on our chart, select ‘view further details’ next to a listing.

Most fixed bonds don’t allow you to access your cash before the account matures, so you’ll need to think carefully before making any deposits – particularly when it comes to longer-term bonds of five or more years.

That being said, some bonds may grant early access before the term ends subject to a loss of interest penalty and/or account closure. You can also discover whether an account permits early access by selecting ‘view further details’ next to a listing on the chart above.

It used to be the case five-year bonds offered higher interest rates than their shorter-term counterparts to compensate savers who risked missing out on better returns or losing value to inflation when locking their money away for the long term.

However, this pattern reversed in 2023 when the best rate paid by a one-year bond overtook that offered by a five-year fixed savings account. This was partly due to the economic uncertainty generated by the September 2022 mini-Budget, as well as global conflicts and the COVID-19 pandemic placing strain upon supply chains, leading to rampant inflation.

Inflation has since cooled and the gap between the top longer and shorter-term bonds has closed significantly. Savers should continue to monitor the best 5 year fixed bond rates over the coming months to see if normal order resumes.

All of the five-year fixed bonds shown on our charts are covered by the Financial Services Compensation Scheme (FSCS), so you can be sure your money is safe if a provider were to go bust.

However, even though the FSCS protects deposits of up to £120,000, it’s important to remember this upper limit includes funds held with any provider operating under the same banking licence (and is not per account).

Check which banks and building societies share a licence with our who owns whom guide or visit the FSCS website for more information on what is covered.

You normally won’t find five-year bonds that are specifically designed for those over 60. Instead, the best 5 year savings account for someone aged 60 or above will likely be that which offers the highest interest rate while still meeting their needs and requirements.

Earning monthly interest from a five-year fixed could be a good way to supplement your income in retirement (when paid away into an accessible account). But, bear in mind that you usually won’t be able to draw upon your savings until the five-year term ends.

While five-year bonds offer some of the longest fixed terms on the market, other terms are available that can suit a wide variety of needs and circumstances.

For instance, if you’re uncomfortable locking away your funds for five years, why not consider a two-year bond, one-year bond or even a bond of less than a year? Alternatively, a three-year bond could offer a middle ground.

All of our newsletters are available free by email to all Moneyfactscompare.co.uk users.

Send me Weekend Moneyfactscompare, Savers Friend, and Companies Friend.

Moneyfactscompare.co.uk will never contact you by phone to sell you any financial product. Any calls like this are not from Moneyfacts. Emails sent by Moneyfactscompare.co.uk will always be from news@moneyfacts-news.co.uk. Be ScamSmart.

Moneyfactscompare.co.uk will never contact you by phone to sell you any financial product. Any calls like this are not from Moneyfacts. Emails sent by Moneyfactscompare.co.uk will always be from news@moneyfacts-news.co.uk. Be ScamSmart.

Moneyfactscompare.co.uk will never contact you by phone to sell you any financial product. Any calls like this are not from Moneyfacts. Emails sent by Moneyfactscompare.co.uk will always be from news@moneyfacts-news.co.uk. Be ScamSmart.

Moneyfactscompare.co.uk will never contact you by phone to sell you any financial product. Any calls like this are not from Moneyfacts. Emails sent by Moneyfactscompare.co.uk will always be from news@moneyfacts-news.co.uk. Be ScamSmart.

Moneyfactscompare.co.uk will never contact you by phone to sell you any financial product. Any calls like this are not from Moneyfacts. Emails sent by Moneyfactscompare.co.uk will always be from news@moneyfacts-news.co.uk. Be ScamSmart.

Moneyfactscompare.co.uk will never contact you by phone to sell you any financial product. Any calls like this are not from Moneyfacts. Emails sent by Moneyfactscompare.co.uk will always be from news@moneyfacts-news.co.uk. Be ScamSmart.

_All_125x80.png)

_All_125x80.png)

_All_125x80.png)

_All_125x80.png)

_All_125x80.png)

_All_125x80.jpg)

_Savings_HLActiveSavings-5YearFixedTermDeposit(110436)_125x80.png)

_All_125x80.png)

_All_125x80.png)

_All_125x80.png)

_Savings_MeteorSavings-5YearFixedTermDeposit(110768)_125x80.png)

_Savings_RaisinUK-5YearFixedTermDeposit(110736)_125x80.png)

_Savings_125x80.png)

_All_125x80.png)

_All_125x80.png)

_Savings_HLActiveSavings-5YearFixedTermDeposit(110443)_125x80.png)

_Savings_RaisinUK-5YearFixedTermDeposit(110695)_125x80.png)

(5356)_Savings_RaisinUK-5YearFixedTermDeposit(110664)_125x80.png)

_All_125x80.png)

_All_125x80.png)