The latest figures reflect the impact the conflict in the Middle East is having on the UK economy.

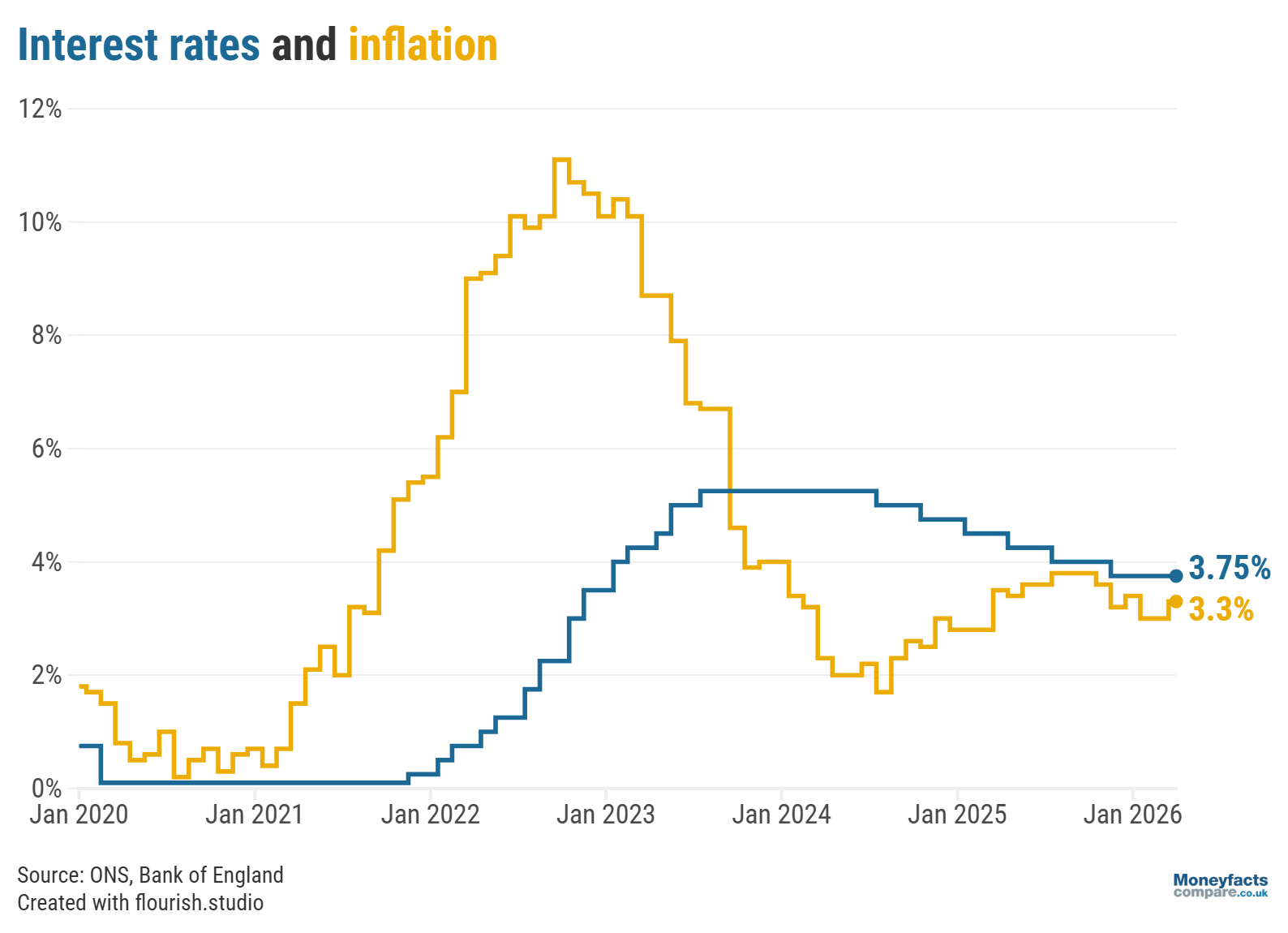

As expected, the annual rate of inflation in the UK rose from 3% in February to 3.3% in March 2026, the Office for National Statistics (ONS) revealed today (22 April).

This was the first set of inflation figures to take into account the conflict in the Middle East (which began at the end of February), so it was no surprise to see inflation increase as the cost of fuel has soared since war broke out.

Rising inflation means that, on average, the cost of goods and services increased more quickly year-on-year in March compared to the previous month. See our guide to find out more about inflation and how it is measured.

Indeed, prices in the transport division rose by 4.7% in the 12 months to March, the highest recorded annual rate since December 2022 and a significant increase from the previous month (2.4%). Motor fuel prices saw particularly notable hikes, as the average price of petrol rose by 8.6 pence per litre between February and March 2026, while the price of diesel rocketed by 17.6 pence per litre over the same period.

In a further blow for households, the cost of food and non-alcoholic drinks rose by 3.7% in the year to March 2026, up from 3.3% in February. A number of categories contributed to this increase, including chocolate and confectionery, meat, fish and soft drinks.

UK Finance Trends: Graph showing the Bank of England base rate and the rate of inflation between 2020 and March 2026.

The rate of inflation is forecast to accelerate even further in 2026, with the Bank of England estimating in March that it could hit 3.5% over the next few months. Some experts think it could rise even higher, but much of this will depend on how the situation in the Middle East evolves.

This higher level of inflation has already significantly altered forecasts for the Bank of England base rate which, at the start of the year, was expected to be cut at least once. But the impact of global events means the Bank’s Monetary Policy Committee (MPC) is much more likely to hold the base rate at its current level of 3.75%, or potentially even increase it if it feels it’s necessary to bring inflation under control.

The MPC is meeting next week to determine where to set the base rate and will announce its decision on Thursday 30 April.

“The fading rate environment attitude at the start of the year has U-turned as fresh inflation shocks continue to shift base rate expectations,” Caitlyn Eastell, Personal Finance Analyst at Moneyfactscompare.co.uk, explained.

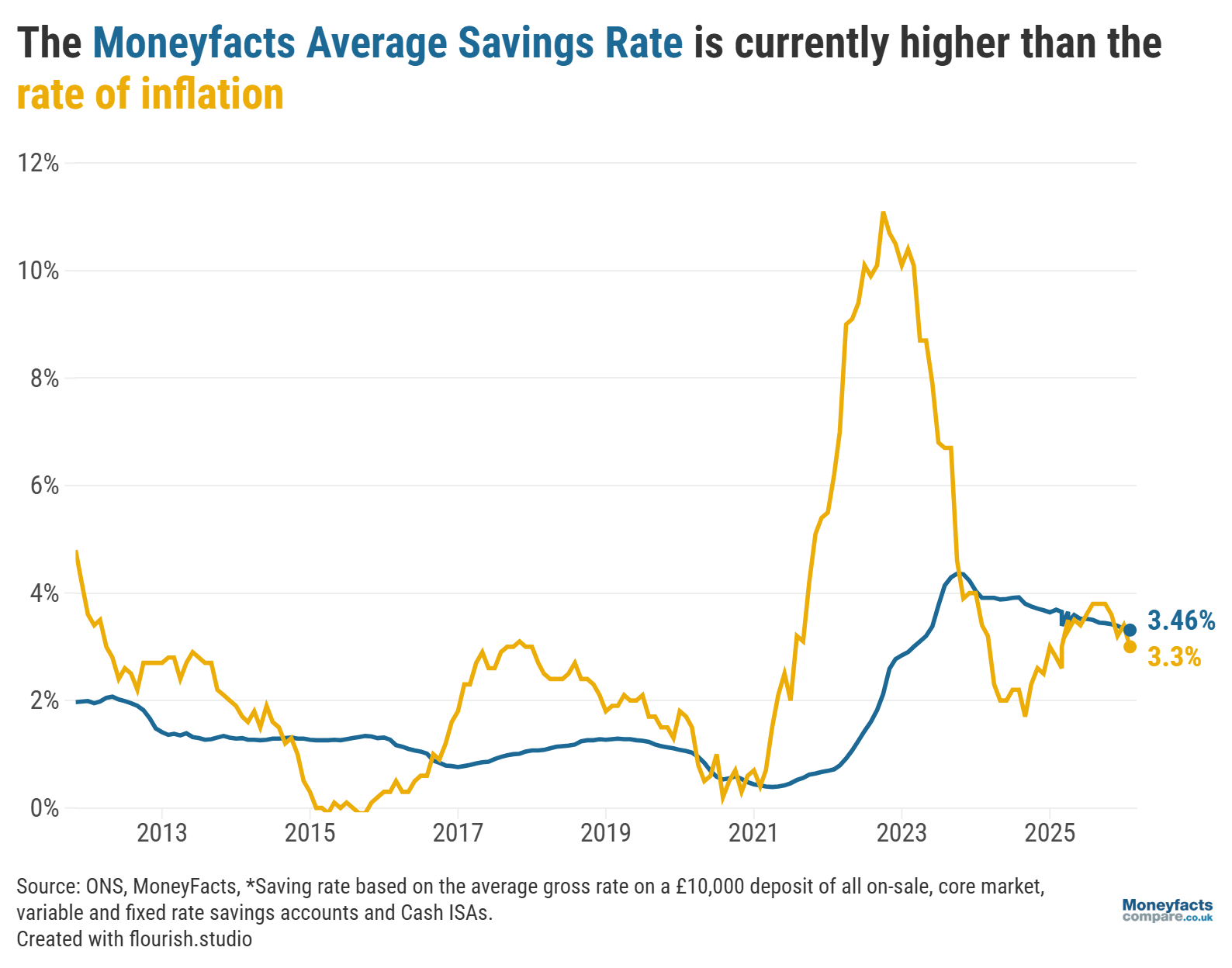

But, despite the higher level of inflation, there were 1,582 savings accounts and ISAs that could offer an inflation-beating rate at the time of the announcement.

UK Savings Trends: Graph showing the Moneyfacts Average Savings Rate and the rate of UK inflation between 2011 and March 2026.

Even if inflation rises to 3.5%, as the Bank of England forecasts, Eastell calculates that (based on today’s rates), there would be over 200 more accounts paying above this rate compared to the last time inflation was at 3.5%*.

“The ‘higher for longer’ stance could temporarily push this number even higher, giving savers unrivalled choice,” Eastell pointed out, but warned that “providers may not be able to maintain these competitive margins as markets remain volatile”.

“Savers face a tricky balancing act. While they may be able to enjoy more competitive returns in the short-term, inflation will quickly catch up, eroding their hard-earned cash. In any case it’s crucial savers shop around for deals that pay over 3.3% to ensure they aren’t left out of pocket,” Eastell urged.

In periods of uncertainty, savers may prefer the flexibility offered by easy access accounts as they can dip into their savings to help cover any unexpected costs, for example. Moreover, easy access options can offer even more competitive rates than fixed accounts, which could help savers boost the return on their money.

However, it’s important to consider that providers can adjust the rate on easy access accounts at any time, whereas fixed accounts pay a guaranteed rate for the specified term.

With inflation on the rise and eating into the purchasing power of our money, it’s particularly important to ensure you’re getting the most competitive return on your savings. When the latest inflation figures were announced, more than 130 easy access accounts and 700 fixed rate bonds paid interest above 3.3%.

Or, if savers want to maximise the tax-free returns on their savings, more than 130 variable ISAs and 300 fixed ISAs offered an inflation-beating rate.

Concerns that the conflict in the Middle East would push up inflation caused havoc in the mortgage market throughout March, as lenders withdrew products and hiked rates.

However, Eastell notes that “rising mortgage rates seem to have stabilised as average rates have held firm in recent weeks”.

“Swap rates have edged closer to 4%, and this has spurred a handful of the biggest lenders to start introducing cuts,” she explained.

But, while mortgage rates are no longer increasing, Eastell warns that the market is “still sensitive to sudden shifts”. Moreover, she calculates that borrowers could be facing a £1,700 increase to their mortgage payments per year on a two-year fix, or £1,300 on a five-year fix since the conflict in Iran began. Based on a typical £250,000 mortgage over 25 years.

“Homebuyers will need to evaluate their affordability because rates could stay higher for longer as the Bank of England tries to bring inflation back towards its target,” she continued.

* Data note: Please note that these savings product numbers include deals that are available to UK residents (easy access accounts, notice accounts, fixed rate bonds, variable Cash ISAs and fixed Cash ISAs) and exclude regular savers, children’s savers, variable rate fixed term bonds or ISAs, JISAs and LISAs, based on a £10,000 deposit, gross rates. Higher rates may be available for other levels of deposit.

All of our newsletters are available free by email to all Moneyfactscompare.co.uk users.

Send me Weekend Moneyfactscompare, Savers Friend, and Companies Friend.

Information is correct as of the date of publication (shown at the top of this article). Any products featured may be withdrawn by their provider or changed at any time. Links to third parties on this page are paid for by the third party. You can find out more about the individual products by visiting their site. Moneyfactscompare.co.uk will receive a small payment if you use their services after you click through to their site. All information is subject to change without notice. Please check all terms before making any decisions. This information is intended solely to provide guidance and is not financial advice. Moneyfacts will not be liable for any loss arising from your use or reliance on this information. If you are in any doubt, Moneyfacts recommends you obtain independent financial advice.

Moneyfactscompare.co.uk will never contact you by phone to sell you any financial product. Any calls like this are not from Moneyfacts. Emails sent by Moneyfactscompare.co.uk will always be from news@moneyfacts-news.co.uk. Be ScamSmart.

Moneyfactscompare.co.uk will never contact you by phone to sell you any financial product. Any calls like this are not from Moneyfacts. Emails sent by Moneyfactscompare.co.uk will always be from news@moneyfacts-news.co.uk. Be ScamSmart.

Moneyfactscompare.co.uk will never contact you by phone to sell you any financial product. Any calls like this are not from Moneyfacts. Emails sent by Moneyfactscompare.co.uk will always be from news@moneyfacts-news.co.uk. Be ScamSmart.

Moneyfactscompare.co.uk will never contact you by phone to sell you any financial product. Any calls like this are not from Moneyfacts. Emails sent by Moneyfactscompare.co.uk will always be from news@moneyfacts-news.co.uk. Be ScamSmart.

Moneyfactscompare.co.uk will never contact you by phone to sell you any financial product. Any calls like this are not from Moneyfacts. Emails sent by Moneyfactscompare.co.uk will always be from news@moneyfacts-news.co.uk. Be ScamSmart.

Moneyfactscompare.co.uk will never contact you by phone to sell you any financial product. Any calls like this are not from Moneyfacts. Emails sent by Moneyfactscompare.co.uk will always be from news@moneyfacts-news.co.uk. Be ScamSmart.