Does this mean inflation won’t rise as much as previously feared?

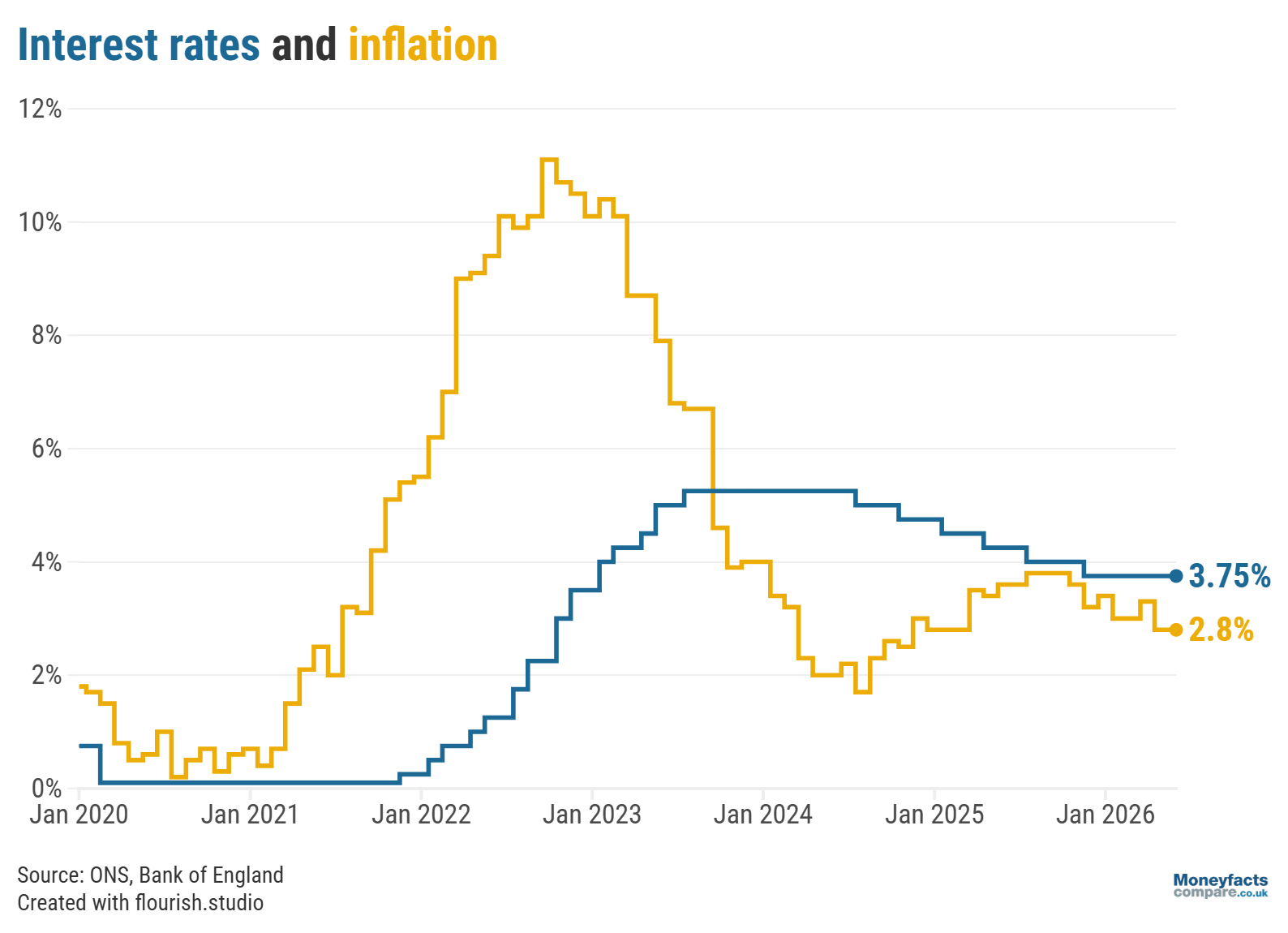

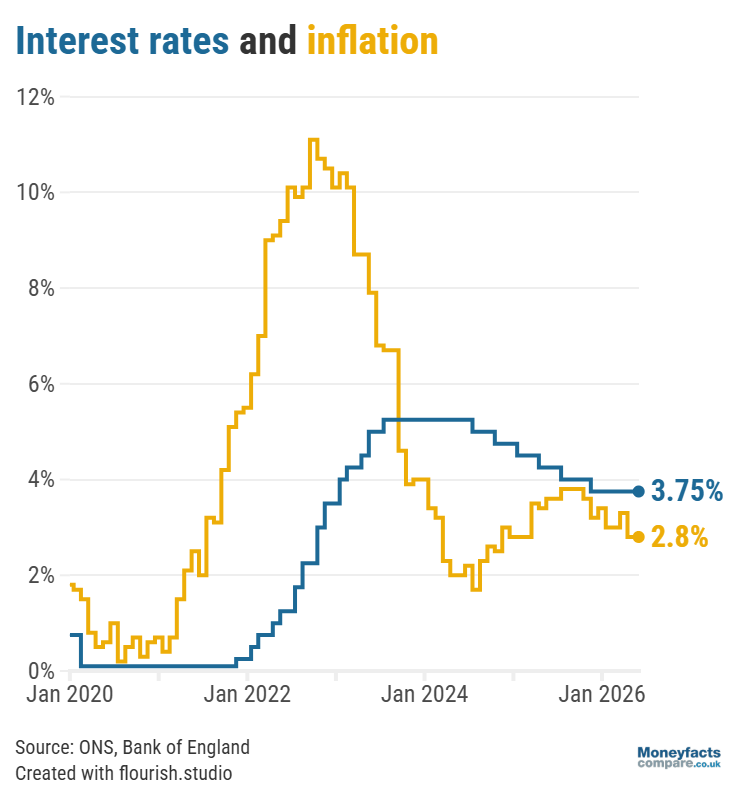

Although many experts had expected the annual rate of UK inflation to increase after it eased in April, it remained at 2.8% in May, the Office for National Statistics (ONS) announced today (17 June).

The conflict in the Middle East was predicted to push up prices in the UK but, so far, the official figures indicate that its effect on the overall cost of living has been relatively limited. While it wouldn’t be a surprise to see inflation accelerate in 2026, the pace of price rises may not be as significant as the Bank of England forecast in its April Monetary Policy Report.

As a worst-case scenario, the Bank said inflation could peak at 6.2% in the first quarter of 2027, but the latest figures and the peace deal that has recently been agreed between the US and Iran makes this outcome appear less likely.

The main measure of inflation is the Consumer Price Index (CPI). This tracks the prices of a range of goods and services over time, with all of these numbers consolidated into one “headline” rate of inflation. Within this main figure, some sectors may have seen prices soar even higher, while other areas may have seen prices fall. Find out more about inflation and how it’s measured.

However, it’s probable that the UK will continue to feel the effect of global events over the coming months and, as the first half of 2026 has shown, the situation can quickly change and completely overturn any predictions.

The Bank of England’s Monetary Policy Committee (MPC) will be taking note of the latest inflation figures, as well as the peace talks between the US and Iran, when it decides where to set the base rate. Many experts are predicting that the base rate will stay at 3.75%, especially in light of recent developments, with the decision to be announced tomorrow (18 June) at midday.

UK Finance Trends: The Bank of England base rate and the rate of inflation between January 2020 and May 2026.

One of the main reasons why inflation didn’t increase as expected was because prices in the food and non-alcoholic beverages sector rose by just 2.2% in the year to May, compared to 3% in the previous month. This was the lowest annual increase in prices in this category since December 2024. Meat (especially beef and cooked ham), cheese, vegetables and fish were some areas that saw prices ease.

On the other hand, transport costs rose by 6.8% in the 12 months to May, significantly higher than the 4.5% recorded in April. Within this overall figure, motor fuel prices increased by 24.6% in the year to May with the average price of petrol (157.4 pence per litre) reaching its highest point since November 2022.

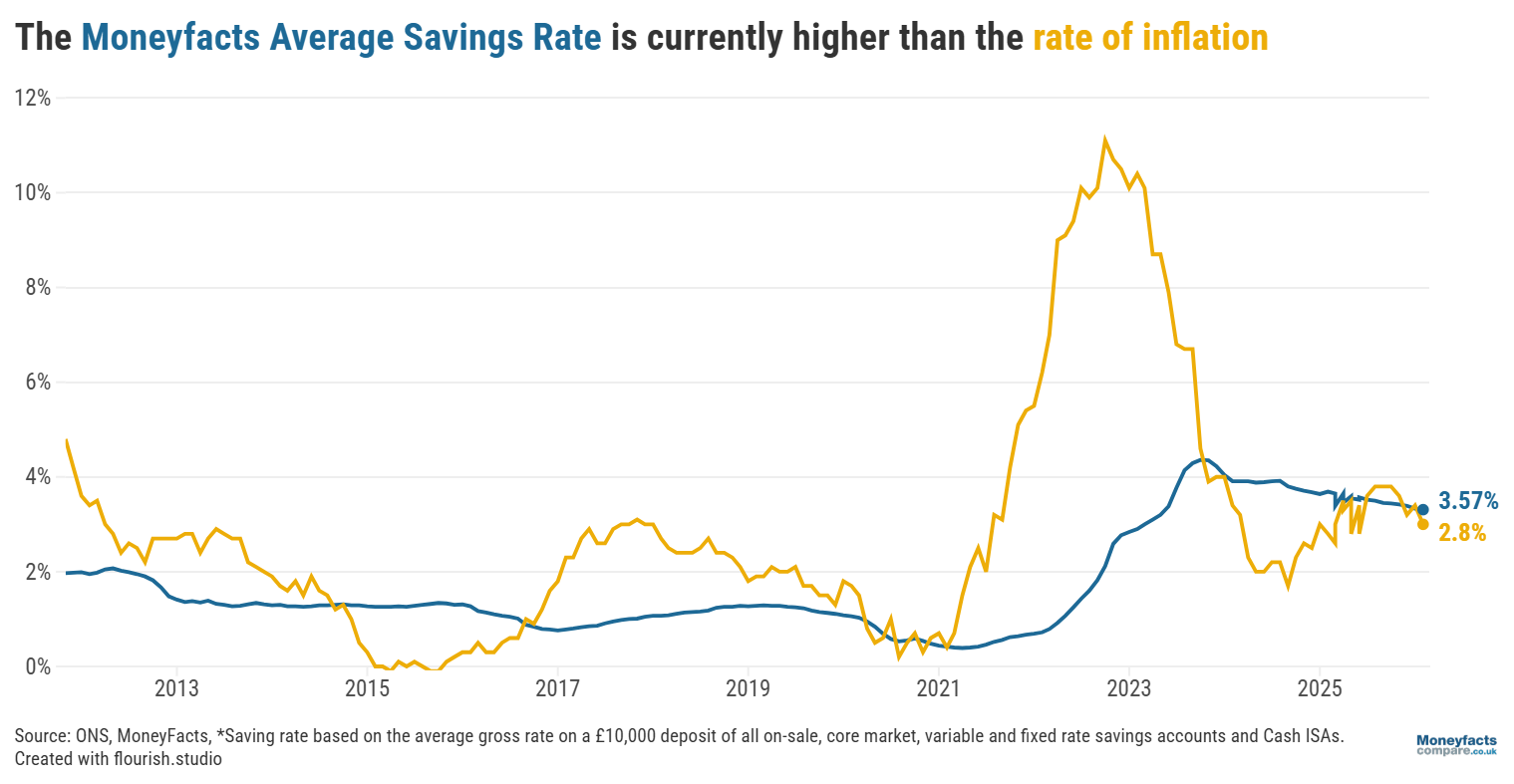

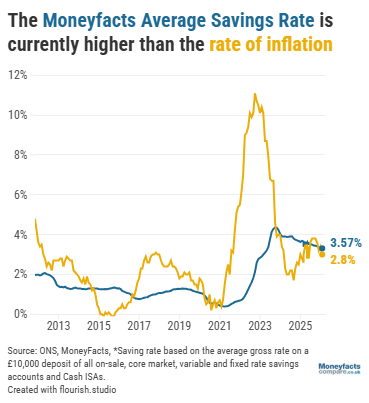

Savings rates have risen in recent months but Caitlyn Eastell, Personal Finance Analyst at Moneyfactscompare.co.uk, points out that they “may not have peaked yet”.

Although inflation held at 2.8% in May, it is still expected to increase in 2026, which could result in a base rate hike this year.

If the Bank of England does raise the base rate, Eastell explains that “banks and building societies are likely to pass this on as they’ll need to compete for deposits”, which means that “headline rates may become more attractive”.

Nevertheless, she warns that this is a “double-edged sword” as “stubborn inflation means savers’ cash can still be losing power even when their balance ticks up on paper”.

UK Savings Trends: The Moneyfacts Average Savings Rate vs the rate of UK inflation since 2011.

While there are currently more than 1,800 savings accounts and ISAs that offer inflation-beating returns, it’s crucial for savers to review their accounts and switch if they’re not earning a competitive rate.

“Loyalty rarely pays and the best rates are typically reserved for new money, not existing customers,” Eastell warns.

Furthermore, she adds that although major high street banks may seem an appealing option for some savers, they rarely pay the best rates.

Eastell calculates that the most flexible accounts from the major high street banks pay just 1.16% on average*, whereas the market-leading easy access savings accounts offer 4.89% (gross). For a saver with a £10,000 deposit, this could be a difference of £373 interest over one year.

“Savers who move away from low-paying high street banks can grow the real value of their cash and stop emergency funds being eaten away by inflation,” Eastell highlighted.

If you haven’t reviewed your savings and switched accounts in a while, your money could be losing value in real terms due to inflation.

When the latest figures were released, there were 1,825 savings accounts and ISAs that paid interest above inflation, which can help savers maximise the return on their money whether they’re searching for an easy access account, a fixed bond or a cash ISA, for example.

Inflation is one of the many factors that influences mortgage rates and expectations that it would accelerate due to the conflict in the Middle East was one of the reasons why we saw lenders hike rates in March and the start of April.

However, average mortgage rates have since dropped, with the Moneyfacts Average Mortgage rate falling from 5.64% to 5.54% since the last inflation announcement.

“In recent weeks average mortgage rates have been dropping and may now be past their peak, offering a welcome opportunity for borrowers. For homeowners approaching the end of their deal, this could be an ideal time to review their options,” Eastell noted.

“Many lenders allow remortgage customers to secure a new rate up to six months before their current deal expires,” she added. This can give customers peace of mind that the monthly payments agreed on this new deal won’t change, even if mortgage rates start rising again. On the other hand, they may have the flexibility to remortgage to a new deal if rates drop significantly, allowing them to lock into a cheaper option.

Either way, Eastell underlines the importance of not letting your mortgage revert to your lender’s Standard Variable Rate (SVR) when a fixed term ends. She calculates that someone with a typical £250,000 mortgage with a 25-year term could find themselves paying almost £3,000 more per year, based on the average SVR (7.13%) and the Moneyfacts Average Mortgage Rate (5.54%).

* Big Bank easy access selection, £10k gross rates: Barclays Bank, Everyday Saver, 1.00%. HSBC, Flexible Saver, 1.04%. Lloyds Bank, Easy Saver, 0.75%. NatWest, Flexible Saver, 1.00%. Santander, Easy Access Saver (Issue 30), 2.00%.

All of our newsletters are available free by email to all Moneyfactscompare.co.uk users.

Send me Weekend Moneyfactscompare, Savers Friend, and Companies Friend.

Information is correct as of the date of publication (shown at the top of this article). Any products featured may be withdrawn by their provider or changed at any time. Links to third parties on this page are paid for by the third party. You can find out more about the individual products by visiting their site. Moneyfactscompare.co.uk will receive a small payment if you use their services after you click through to their site. All information is subject to change without notice. Please check all terms before making any decisions. This information is intended solely to provide guidance and is not financial advice. Moneyfacts will not be liable for any loss arising from your use or reliance on this information. If you are in any doubt, Moneyfacts recommends you obtain independent financial advice.

Moneyfactscompare.co.uk will never contact you by phone to sell you any financial product. Any calls like this are not from Moneyfacts. Emails sent by Moneyfactscompare.co.uk will always be from news@moneyfacts-news.co.uk. Be ScamSmart.

Moneyfactscompare.co.uk will never contact you by phone to sell you any financial product. Any calls like this are not from Moneyfacts. Emails sent by Moneyfactscompare.co.uk will always be from news@moneyfacts-news.co.uk. Be ScamSmart.

Moneyfactscompare.co.uk will never contact you by phone to sell you any financial product. Any calls like this are not from Moneyfacts. Emails sent by Moneyfactscompare.co.uk will always be from news@moneyfacts-news.co.uk. Be ScamSmart.

Moneyfactscompare.co.uk will never contact you by phone to sell you any financial product. Any calls like this are not from Moneyfacts. Emails sent by Moneyfactscompare.co.uk will always be from news@moneyfacts-news.co.uk. Be ScamSmart.

Moneyfactscompare.co.uk will never contact you by phone to sell you any financial product. Any calls like this are not from Moneyfacts. Emails sent by Moneyfactscompare.co.uk will always be from news@moneyfacts-news.co.uk. Be ScamSmart.

Moneyfactscompare.co.uk will never contact you by phone to sell you any financial product. Any calls like this are not from Moneyfacts. Emails sent by Moneyfactscompare.co.uk will always be from news@moneyfacts-news.co.uk. Be ScamSmart.