Despite this dip, consumers should prepare for higher levels of inflation over the coming months.

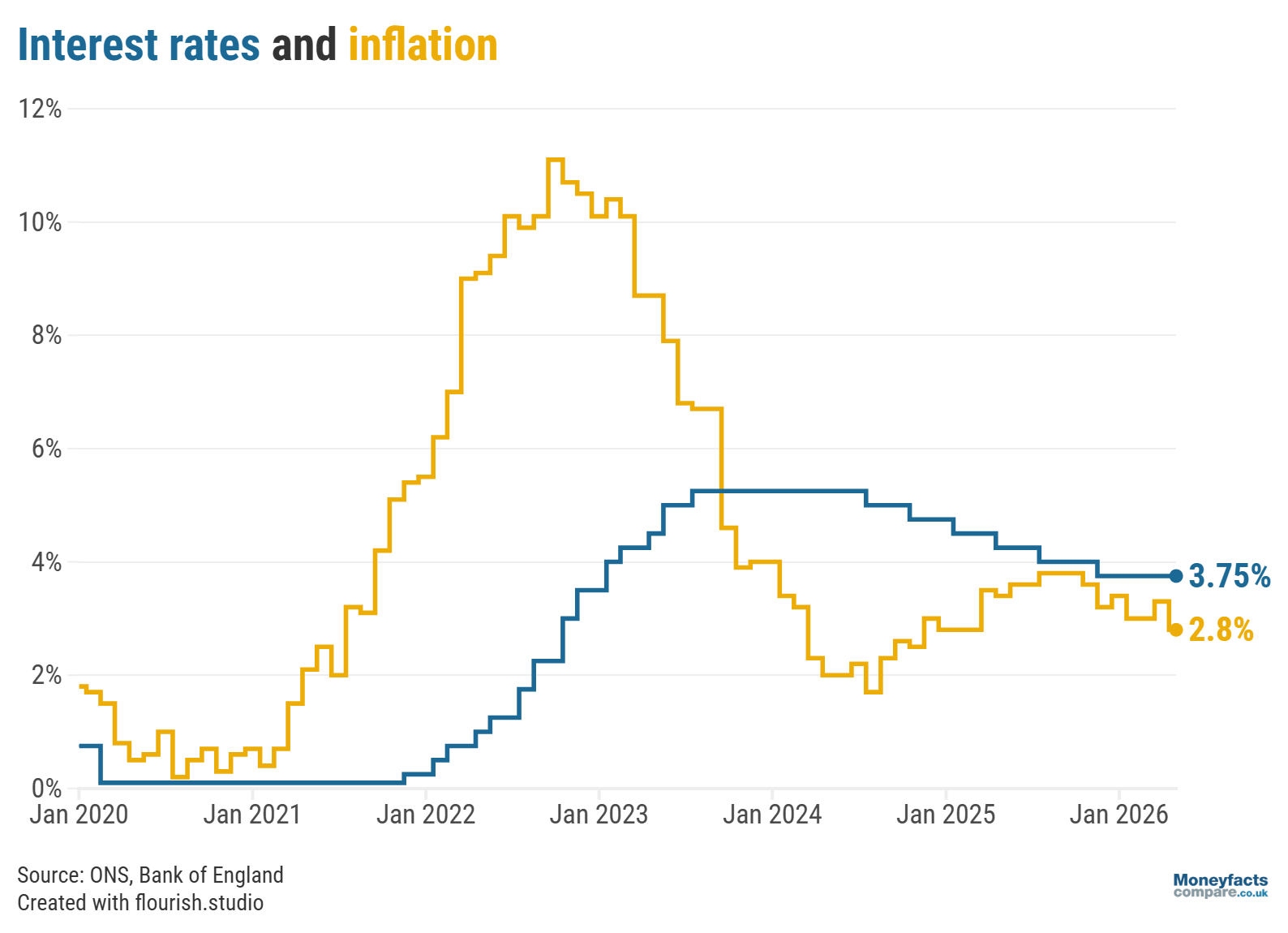

The annual rate of UK inflation fell from 3.3% in March 2026 to 2.8% in April 2026, the Office for National Statistics (ONS) revealed today (20 May).

This is the lowest this figure has been in over a year and, while experts had predicted a marginal drop in April due to lower gas and electricity prices, it slowed by much more than many had predicted.

Even though April’s inflation figure is lower than the previous month, the cost of goods and services have still risen year-on-year. The Consumer Price Index (CPI) looks at thousands of prices to calculate how much they have changed over the past 12 months and, in April, they increased by 2.8%.

In general, prices are more expensive than one year ago, and with experts predicting that inflation will accelerate over the coming months, see our guide to find out more about how inflation could affect your money.

Unfortunately for households, this drop in inflation is likely to be short-lived. As the unrest in the Middle East continues, affecting many aspects of the UK economy, the rate of inflation is expected to increase and move further away from the Bank of England’s target of 2% in 2026.

The Bank of England will be closely monitoring the rate of rising prices, as well as the overall UK economy, to decide whether it needs to take action to try to curb inflation. Its Monetary Policy Committee (MPC) can use the UK’s central interest rate (or base rate) to influence household spending and, consequently, inflation, but it’s a difficult balancing act to strike as there are many factors it needs to consider.

The MPC will make its next announcement on 18 June, the day after May’s inflation figure is released. Read more on how the base rate works and how it affects our finances.

UK Finance Trends: The Bank of England base rate and the rate of inflation between January 2020 and April 2026.

A major reason for the slower rate of inflation was a fall in gas and electricity prices, partly due to Ofgem lowering the price cap in April and the Government’s additional support to help with energy costs. Electricity prices plummeted by 8.4% in April 2026 (compared to a rise of 2.9% one year ago), while gas prices dropped by 4.4%, compared to a rise of 7.5% the previous year.

Costs in the recreation and culture sector also rose by a slower rate than one year ago, particularly package holidays. Part of this may be explained by when data was gathered as April 2025’s inflation figures were collected during the Easter holidays when prices are typically more expensive, whereas 2026’s data collection date fell outside the main holiday period.

Consumers may be encouraged to see that prices in the food and non-alcoholic beverages category rose by just 3.0% in the 12 months to April, down from March’s annual rate of 3.7%. However, due to the fallout from the conflict in the Middle East, the cost of fuel continued to rocket and put strain on households’ finances.

The average price of petrol rose by 16.6 pence per litre between March and April 2026 to reach 156.8 pence per litre, its highest level since November 2022. Diesel prices saw an even more notable increase as they soared by 31.3 pence per litre in the month to April. Now at 190.0 pence per litre, the cost of diesel is the most expensive it has been since July 2022.

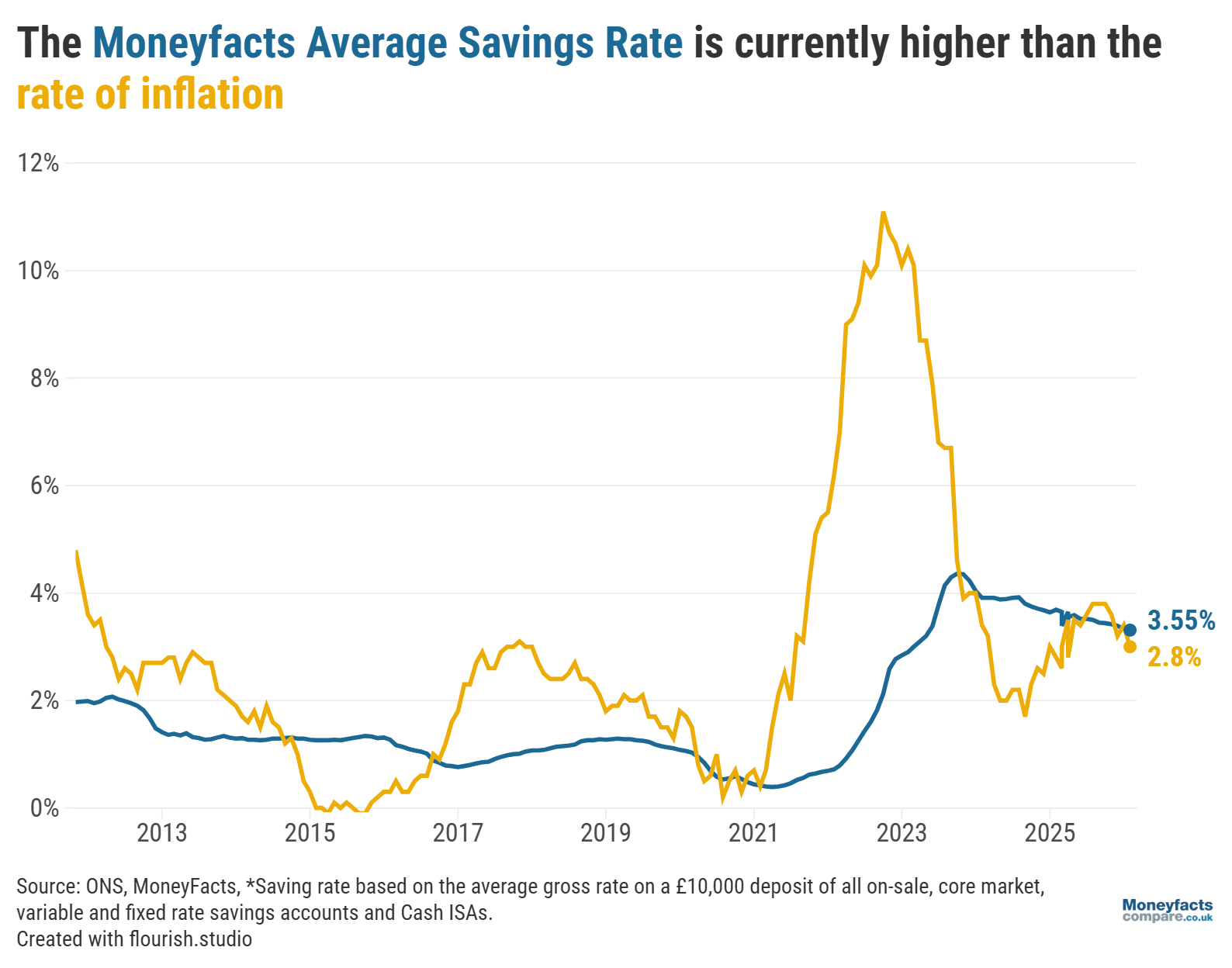

Inflation can eat away at the purchasing power of our savings as, due to rising prices, the same sum of money can buy less than it did before. Even if savers have been diligent about putting their money into a competitive savings account, they won’t necessarily have shielded it from the eroding effects of inflation.

For example, savers who deposited £10,000 into a five-year bond in May 2021, at what was then a top rate of 1.40%, would have earned around £700 in interest. However, Caitlyn Eastell, Personal Finance Analyst at Moneyfactscompare.co.uk, calculated that average inflation worked out at around 4.6% per year over this period, which meant the real value of the investment would have fallen to around £8,600. This equates to a real-term loss of around £1,400 over five years.

“While savings rates now sit far higher than in the ultra-low era, and as the top rates are moving in a positive direction, it remains crucial for savers to focus on true value instead of attractive headline rates,” Eastell urged.

UK Savings Trends: How the Moneyfacts Average Savings Rate has compared to the rate of UK inflation since 2011.

In its latest Monetary Policy Report, the Bank of England outlined several ways inflation could change, and, in the worst-case scenario, it forecast that inflation could reach 5.6% in Q2 of 2027. If this materialises, savers could see the real return on their money suffer, even with today’s higher savings rates.

“To avoid the same fate of inflation-battered returns, savers need to take a more proactive approach by reviewing deals frequently, making use of their tax-free cash ISA wrappers and avoiding apathy with long standing accounts that pay below average returns,” Eastell explained.

At the time of the latest ONS announcement, 1,806 savings accounts and ISAs paid interest above inflation. Whether you want the flexibility of an easy access account, the guaranteed returns offered by a fixed bond or the tax-free benefits of a cash ISA, there are plenty of opportunities to find an inflation-beating account.

Even though mortgage rates seem to have settled down in recent weeks after the upheaval immediately following the outbreak of conflict in the Middle East, Eastell warns that “the mortgage market remains highly reactive to ongoing shocks”.

Moreover, she adds that “swap rates have continued to spike following escalating tensions in the Middle East and the uncertainty around the UK’s political landscape”, which could be bad news for borrowers.

“Interest rates remaining higher for longer will quickly burden borrowers, squeezing their budgets and how much they can afford. Millions of households are due to remortgage, but those coming off an ultra-low five-year fixed rate should be prepared to see their repayments spike by more than £5,400 a year,” Eastell noted.

While tracker mortgages can offer more competitive rates than fixed deals, Eastell points out that “they leave borrowers more exposed to volatility, as any change in the Bank of England base rate is directly passed through to monthly repayments”.

All of our newsletters are available free by email to all Moneyfactscompare.co.uk users.

Send me Weekend Moneyfactscompare, Savers Friend, and Companies Friend.

Information is correct as of the date of publication (shown at the top of this article). Any products featured may be withdrawn by their provider or changed at any time. Links to third parties on this page are paid for by the third party. You can find out more about the individual products by visiting their site. Moneyfactscompare.co.uk will receive a small payment if you use their services after you click through to their site. All information is subject to change without notice. Please check all terms before making any decisions. This information is intended solely to provide guidance and is not financial advice. Moneyfacts will not be liable for any loss arising from your use or reliance on this information. If you are in any doubt, Moneyfacts recommends you obtain independent financial advice.

Moneyfactscompare.co.uk will never contact you by phone to sell you any financial product. Any calls like this are not from Moneyfacts. Emails sent by Moneyfactscompare.co.uk will always be from news@moneyfacts-news.co.uk. Be ScamSmart.

Moneyfactscompare.co.uk will never contact you by phone to sell you any financial product. Any calls like this are not from Moneyfacts. Emails sent by Moneyfactscompare.co.uk will always be from news@moneyfacts-news.co.uk. Be ScamSmart.

Moneyfactscompare.co.uk will never contact you by phone to sell you any financial product. Any calls like this are not from Moneyfacts. Emails sent by Moneyfactscompare.co.uk will always be from news@moneyfacts-news.co.uk. Be ScamSmart.

Moneyfactscompare.co.uk will never contact you by phone to sell you any financial product. Any calls like this are not from Moneyfacts. Emails sent by Moneyfactscompare.co.uk will always be from news@moneyfacts-news.co.uk. Be ScamSmart.

Moneyfactscompare.co.uk will never contact you by phone to sell you any financial product. Any calls like this are not from Moneyfacts. Emails sent by Moneyfactscompare.co.uk will always be from news@moneyfacts-news.co.uk. Be ScamSmart.

Moneyfactscompare.co.uk will never contact you by phone to sell you any financial product. Any calls like this are not from Moneyfacts. Emails sent by Moneyfactscompare.co.uk will always be from news@moneyfacts-news.co.uk. Be ScamSmart.