As the wider market slowly recovers from recent global shocks.

While the mortgage market showed signs of improvement at the start of this month, first-time buyers continue to “bear the brunt” of recent turmoil, according to Rachel Springall, Finance Expert at Moneyfactscompare.co.uk.

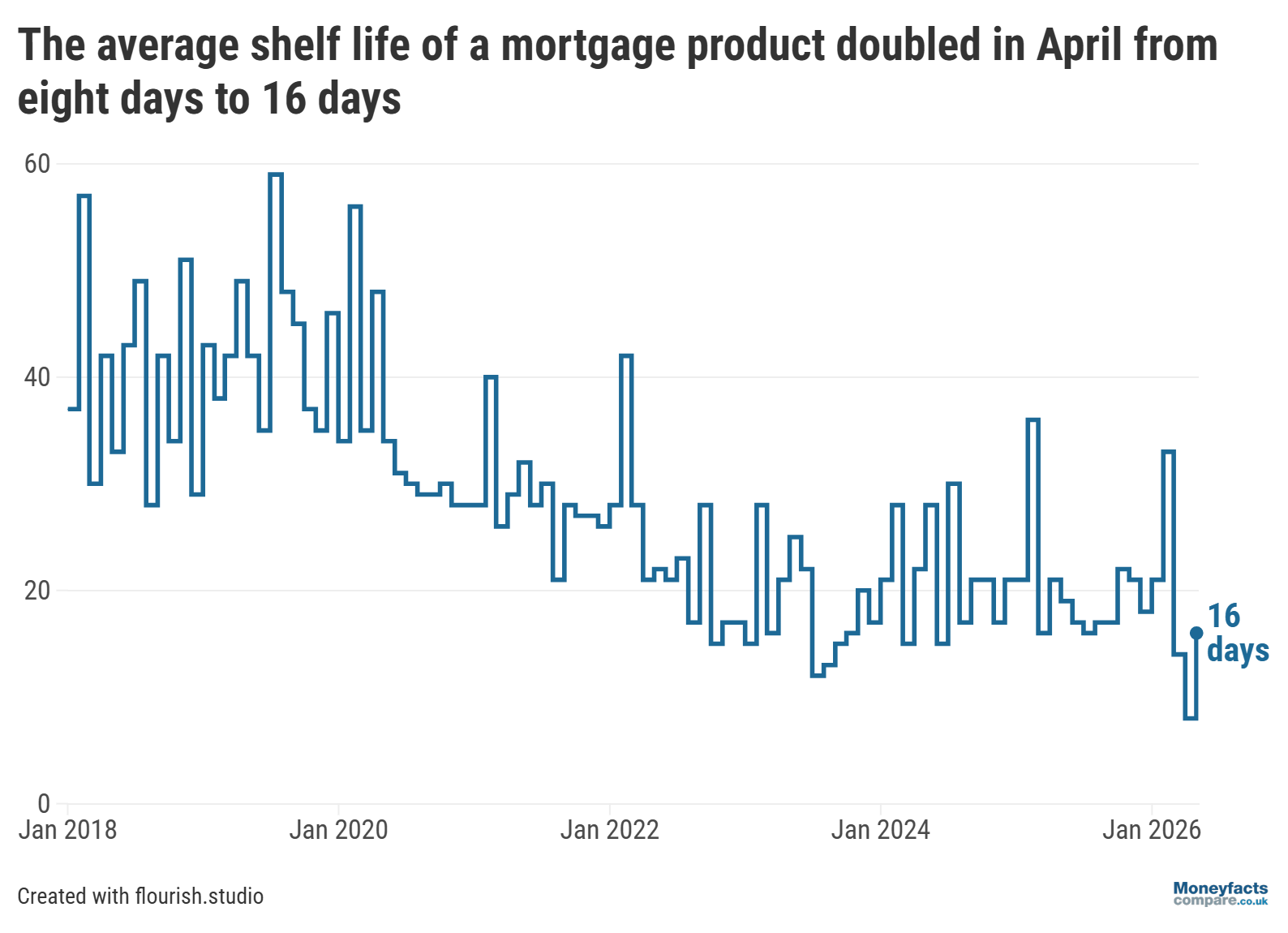

“The global pressures caused by the conflict in the Middle East completely flipped the expected path of inflation and future rate setting, which caused lenders to pull deals and hike fixed rates,” Springall explained. However, the latest Moneyfacts UK Mortgage Trends Treasury Report revealed product turnover has since eased considerably – with the average shelf-life of a mortgage doubling from a record-low of eight days in April to 16 days by May.

UK Mortgage Trends: Graph showing average mortgage shelf-life between 2018 and May 2026.

But, even though it found more than 500 deals have returned to the market over the past month, this represents less than half of those withdrawn between March and April. Overall product choice is still down by around 10% since the beginning of March; in particular, there are approximately 200 fewer deals available at 90% and 95% loan-to-value (LTV) – much to the dismay of first-time buyers with small deposits.

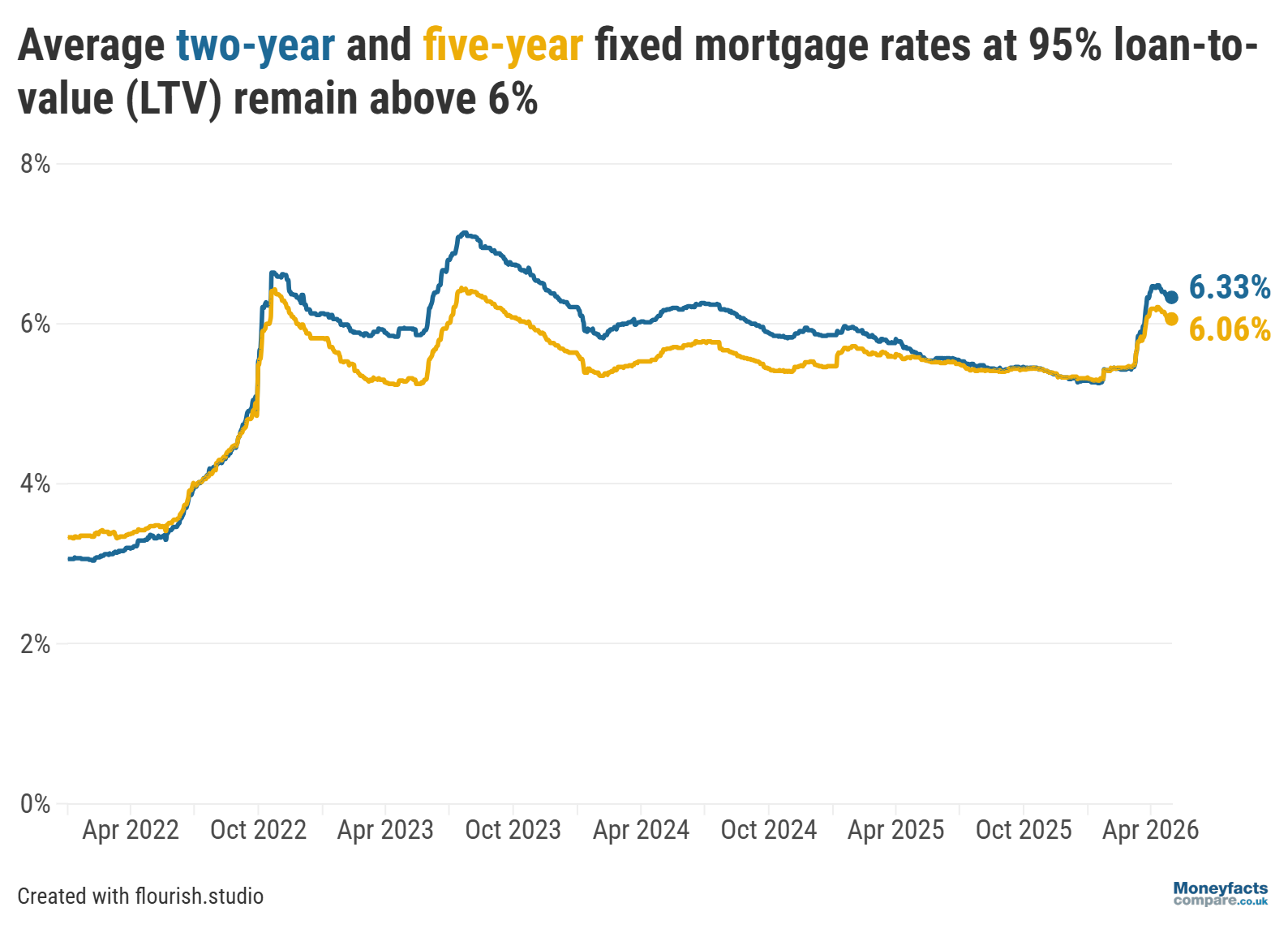

To make matters worse, the average two- and five-year fixed rates charged by 95% LTV mortgage deals remained elevated above 6% at the beginning of May (despite having fallen slightly). By contrast, the typical rate charged by a two- and five-year fixed mortgage (across all LTVs) cooled to 5.78% and 5.68%, respectively.

UK Mortgage Trends: Average two- and five-year fixed mortgage rates at 90% and 95% LTV between 2022 and May 2026.

Our charts are regularly updated throughout the day so you can discover some of the lowest mortgage rates currently available.

But, keep in mind the cheapest-priced deal may not be the most cost-effective for your circumstances and it’s important to consider other factors, such as fees and incentives. That’s why our weekly mortgage roundup includes some Moneyfacts Best Buy alternatives based on their overall true cost, while also providing details on some of the week’s lowest fixed rates.

As well as less choice and higher interest rates, first-time buyers must also contend with a lack of affordable housing and a potential spike in the cost of living.

“It is understandable to see why affordability for borrowers continues to be stretched,” said Springall, adding that “incomes are not stretching far enough to acquire a mortgage and those trapped in the rental cycle struggle to build a sizeable deposit”.

Those determined to get on the property ladder may find they need to borrow larger amounts. Indeed, Springall highlighted data from the Financial Conduct Authority (FCA) which showed the proportion of lending to a single borrower at four times’ income reached its highest level since 2021 in the final quarter of last year.

“As may be obvious, securing a mortgage can be more of a challenge for those going alone, which means any relaxation to loan-to-income rules, such as with building societies like Nationwide with its Helping Hand mortgage at six times’ income, can make all the difference,” said Springall. She added that “support and innovation from lenders will be vital to keep the market moving”.

Meanwhile, borrowers searching for more affordable options could consider taking out a longer-term mortgage (of 35 or 40 years) to lower their initial payments. However, Springall flagged that “this means paying more interest overall, so making overpayments where possible to reduce the debt and mortgage term is wise”. She also encouraged “seeking advice from a broker” to “keep abreast of the latest deals and get invaluable advice on affordability constraints”.

Mortgage brokers remove a lot of the paperwork and hassle of getting a mortgage, as well as helping you access exclusive products and rates that aren’t available to the public. Mortgage brokers are regulated by the FCA and are required to pass specific qualifications before they can give you advice.

MAB is the preferred mortgage broker of Moneyfactscompare.co.uk

![]()

Get friendly, expert advice free of charge as a visitor of Moneyfactscompare.co.uk

Mortgage Advice Bureau have 1,600 UK advisers with 200 awards between them.

Speak to an award-winning mortgage broker today.

Call 0800 031 8553 or request a callback

Mortgage Advice Bureau offers fee free mortgage advice for Moneyfactscompare.co.uk visitors that call on 0800 031 8553. If you contact Mortgage Advice Bureau outside of these channels you may incur a fee of up to 1%. Lines are open Monday to Friday 8am to 8pm and Saturday 9am to 1pm excluding bank holidays. Calls may be recorded.

Your home may be repossessed if you do not keep up repayments on your mortgage.

All of our newsletters are available free by email to all Moneyfactscompare.co.uk users.

Send me Weekend Moneyfactscompare, Savers Friend, and Companies Friend.

Information is correct as of the date of publication (shown at the top of this article). Any products featured may be withdrawn by their provider or changed at any time. Links to third parties on this page are paid for by the third party. You can find out more about the individual products by visiting their site. Moneyfactscompare.co.uk will receive a small payment if you use their services after you click through to their site. All information is subject to change without notice. Please check all terms before making any decisions. This information is intended solely to provide guidance and is not financial advice. Moneyfacts will not be liable for any loss arising from your use or reliance on this information. If you are in any doubt, Moneyfacts recommends you obtain independent financial advice.

Moneyfactscompare.co.uk will never contact you by phone to sell you any financial product. Any calls like this are not from Moneyfacts. Emails sent by Moneyfactscompare.co.uk will always be from news@moneyfacts-news.co.uk. Be ScamSmart.

Moneyfactscompare.co.uk will never contact you by phone to sell you any financial product. Any calls like this are not from Moneyfacts. Emails sent by Moneyfactscompare.co.uk will always be from news@moneyfacts-news.co.uk. Be ScamSmart.

Moneyfactscompare.co.uk will never contact you by phone to sell you any financial product. Any calls like this are not from Moneyfacts. Emails sent by Moneyfactscompare.co.uk will always be from news@moneyfacts-news.co.uk. Be ScamSmart.

Moneyfactscompare.co.uk will never contact you by phone to sell you any financial product. Any calls like this are not from Moneyfacts. Emails sent by Moneyfactscompare.co.uk will always be from news@moneyfacts-news.co.uk. Be ScamSmart.

Moneyfactscompare.co.uk will never contact you by phone to sell you any financial product. Any calls like this are not from Moneyfacts. Emails sent by Moneyfactscompare.co.uk will always be from news@moneyfacts-news.co.uk. Be ScamSmart.

Moneyfactscompare.co.uk will never contact you by phone to sell you any financial product. Any calls like this are not from Moneyfacts. Emails sent by Moneyfactscompare.co.uk will always be from news@moneyfacts-news.co.uk. Be ScamSmart.