What does this mean for someone trying to get on the property ladder?

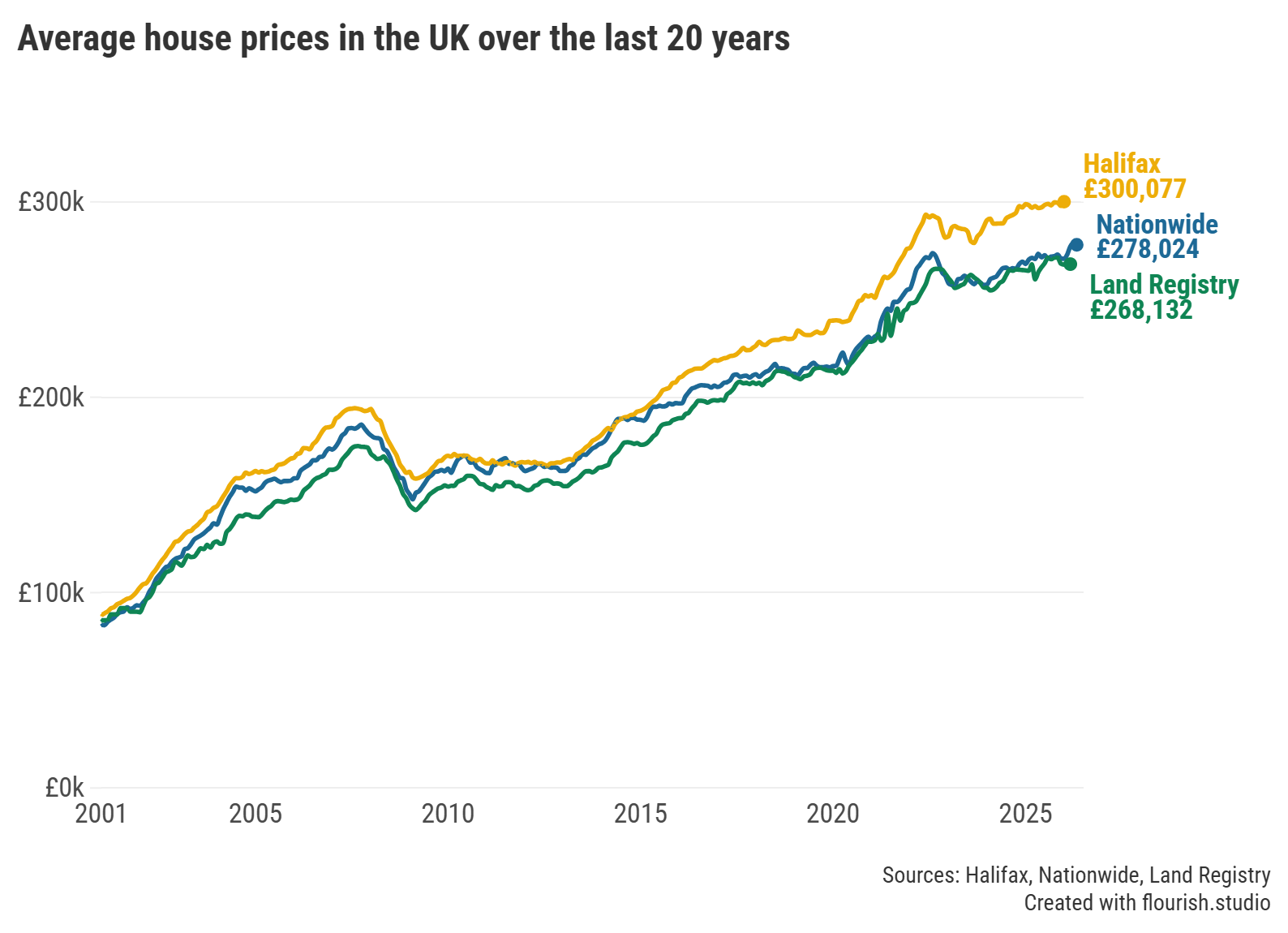

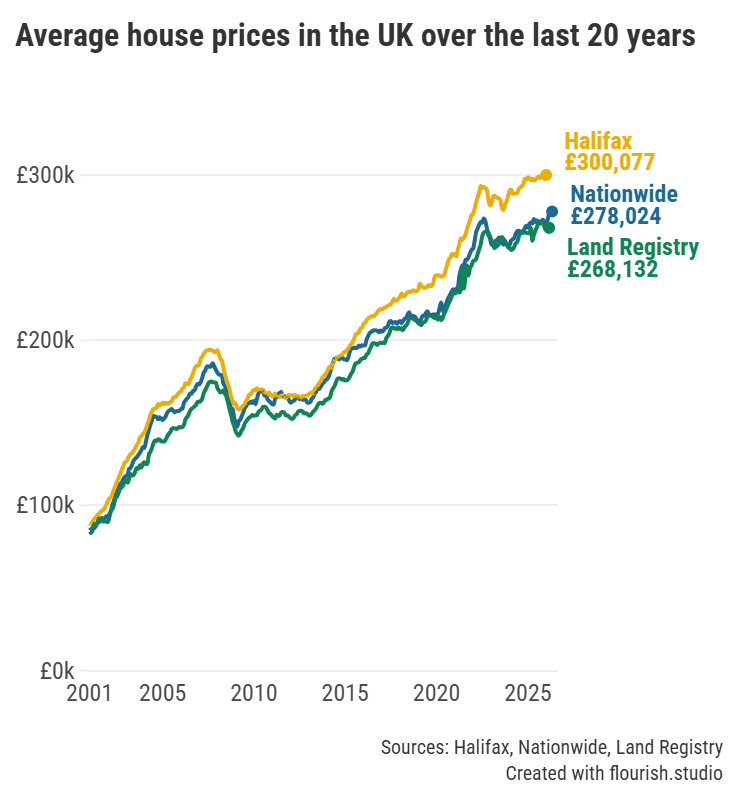

UK house prices fell for the first time this year as far-reaching consequences of conflict in the Middle East continue to stifle buyer demand. This is according to latest figures released today by one of the country’s biggest mortgage lenders, Nationwide BS, that revealed the average price of a property in the UK shrank by 0.6% (around £900) month-on-month to £278,024 in May.

UK Housing Market: Graph showing average house prices over the past 20 years.

"Given the uncertainty caused by developments in the Middle East and the subsequent rise in energy prices and market interest rates," Robert Gardner, Chief Economist at Nationwide BS, said “some loss of momentum was to be expected”.

Related article: Slight reprieve for households as inflation slows to 2.8% in April

“Consumer confidence has weakened noticeably since the start of the conflict,” Gardner explained, adding that GfK’s Consumer Confidence Index increased only marginally last month after dropping to an over two-year low in April 2026.

Furthermore, Gardner said that “measures of housing market sentiment have also deteriorated”, with the Royal Institution of Chartered Surveyors (RICS) reporting “a sharp fall in new buyer enquiries in March, taking the index to its weakest reading since 2023”. Despite a very slight improvement in April, enquiries remained “deep in negative territory in April”, he continued.

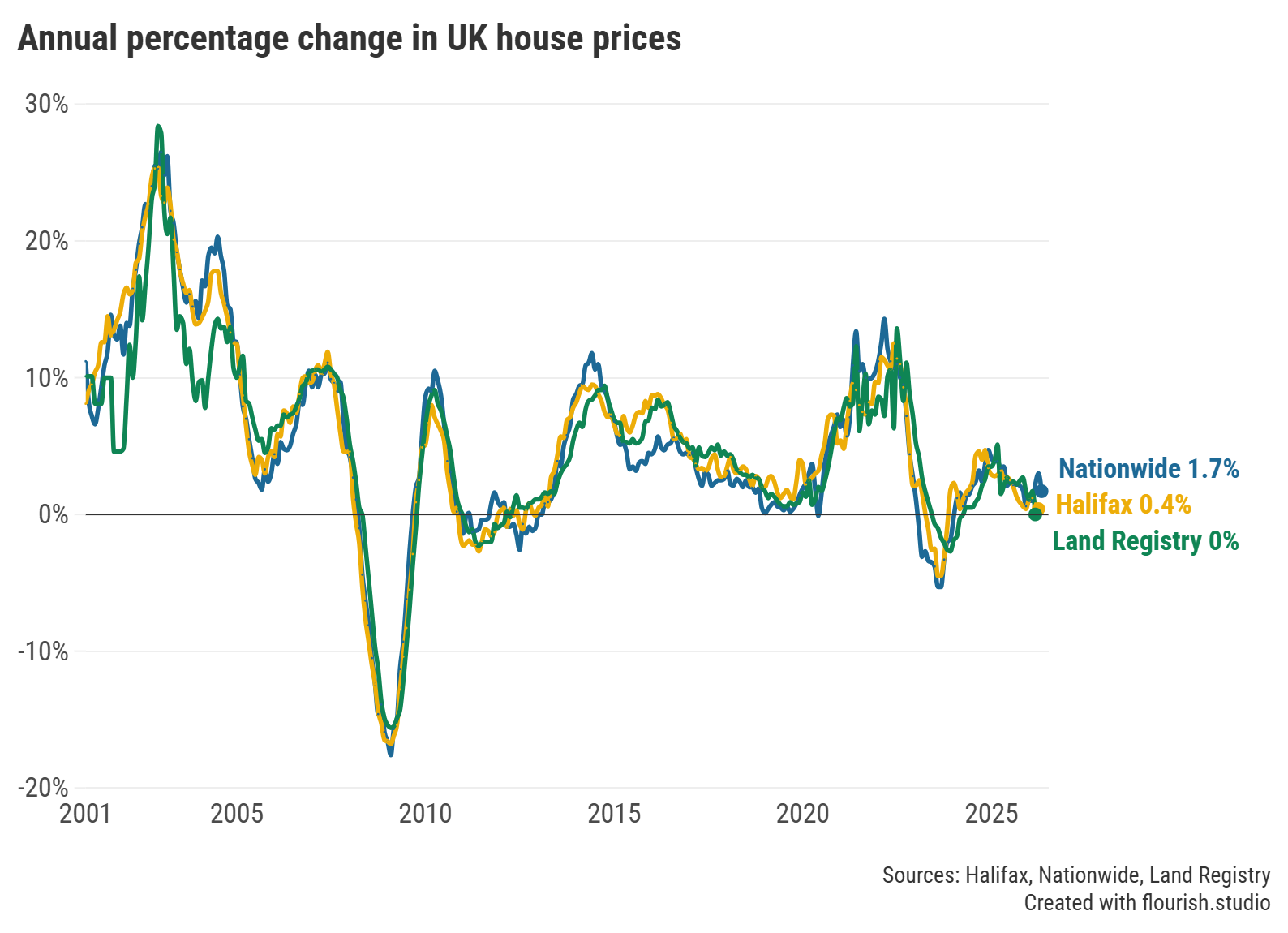

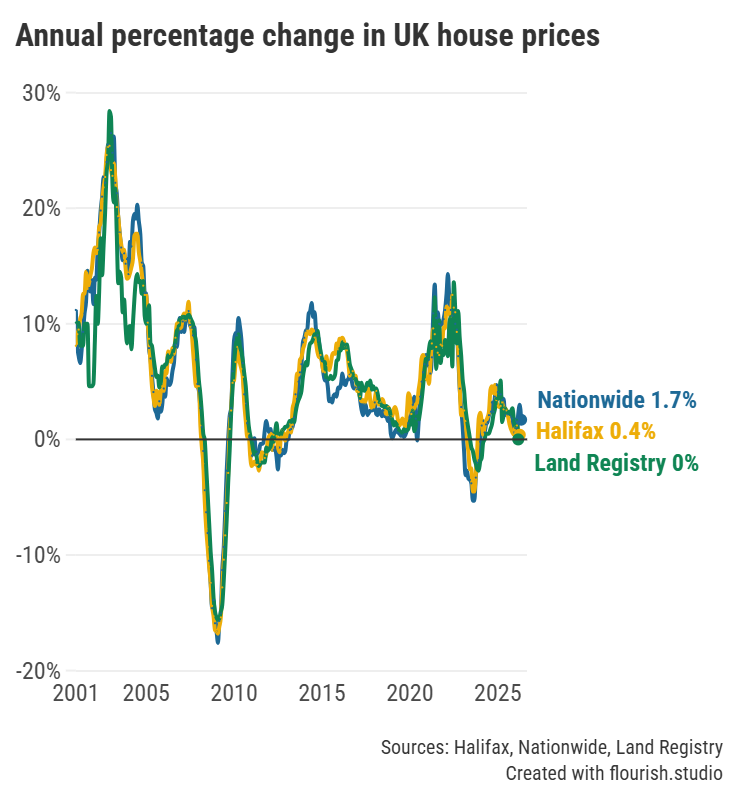

Nationwide BS’s House Price Index (HPI) also showed the rate at which property prices have risen over the course of a year slowed to 1.7% in May (from 3.0% in April). As a result, a typical UK home is now worth almost £5,000 more than a year ago.

UK Housing Market: Graph showing annual percentage change in UK house prices over the past 20 years.

But, while the lull in annual property price growth may dismay existing homeowners, it could offer a sliver of opportunity to those struggling to get a foot on the ladder.

“Affordability remains a key issue for would-be buyers. Not only have house prices risen by almost £14,000 over the past two years alone, but higher mortgage rates, inflationary pressures and a lack of affordable housing create a challenging environment,” said Rachel Springall, Finance Expert at Moneyfactscompare.co.uk. However, she added that “buyers who can afford a mortgage … will have bargaining power on their side”.

Those currently searching for a mortgage deal may feel some relief that more than a dozen lenders made cuts last week – including the likes of Barclays Mortgage and NatWest. What’s more, others could soon follow suit.

“Lenders continue to reprice their offers in reaction to volatile swap rates,” said Springall, adding that with two- and five-year swap rates trending at 30-day lows, “this typically creates a more tolerant lean towards making further rates cuts than rises”.

“It will be vital to keep momentum in the mortgage market at a time when fears over the rise in the cost of living continue to weigh overhead. Relaxing loan-to-income rules allows buyers to secure their dream home, such as with Nationwide’s Helping Hand mortgage, and supports first-time buyers who remain the lifeblood of the market,” she concluded.

Our mortgage charts are updated throughout the day so you can easily discover some of the lowest rates currently available.

But remember that the cheapest-priced deal may not be the most cost-effective for your circumstances and it’s important to consider other factors, such as fees and incentives. That’s why our weekly mortgage roundup includes some Moneyfacts Best Buy alternatives based on their overall true cost as well as providing a summary of deals charging some of the lowest fixed rates.

Alternatively, you could speak to a broker for help exploring your options and finding the best mortgage deal for your needs.

Speak to an award-winning mortgage broker today

Mortgage brokers remove a lot of the paperwork and hassle of getting a mortgage, as well as helping you access exclusive products and rates that aren’t available to the public. Mortgage brokers are regulated by the Financial Conduct Authority (FCA) and are required to pass specific qualifications before they can give you advice.

MAB is the preferred mortgage broker of Moneyfactscompare.co.uk

![]()

Get friendly, expert advice free of charge as a visitor of Moneyfactscompare.co.uk

Mortgage Advice Bureau have 1,600 UK advisers with 200 awards between them.

Speak to an award-winning mortgage broker today.

Call 0800 031 8553 or request a callback

Mortgage Advice Bureau offers fee free mortgage advice for Moneyfactscompare.co.uk visitors that call on 0800 031 8553. If you contact Mortgage Advice Bureau outside of these channels you may incur a fee of up to 1%. Lines are open Monday to Friday 8am to 8pm and Saturday 9am to 1pm excluding bank holidays. Calls may be recorded.

Your home may be repossessed if you do not keep up repayments on your mortgage.

All of our newsletters are available free by email to all Moneyfactscompare.co.uk users.

Send me Weekend Moneyfactscompare, Savers Friend, and Companies Friend.

Information is correct as of the date of publication (shown at the top of this article). Any products featured may be withdrawn by their provider or changed at any time. Links to third parties on this page are paid for by the third party. You can find out more about the individual products by visiting their site. Moneyfactscompare.co.uk will receive a small payment if you use their services after you click through to their site. All information is subject to change without notice. Please check all terms before making any decisions. This information is intended solely to provide guidance and is not financial advice. Moneyfacts will not be liable for any loss arising from your use or reliance on this information. If you are in any doubt, Moneyfacts recommends you obtain independent financial advice.

Moneyfactscompare.co.uk will never contact you by phone to sell you any financial product. Any calls like this are not from Moneyfacts. Emails sent by Moneyfactscompare.co.uk will always be from news@moneyfacts-news.co.uk. Be ScamSmart.

Moneyfactscompare.co.uk will never contact you by phone to sell you any financial product. Any calls like this are not from Moneyfacts. Emails sent by Moneyfactscompare.co.uk will always be from news@moneyfacts-news.co.uk. Be ScamSmart.

Moneyfactscompare.co.uk will never contact you by phone to sell you any financial product. Any calls like this are not from Moneyfacts. Emails sent by Moneyfactscompare.co.uk will always be from news@moneyfacts-news.co.uk. Be ScamSmart.

Moneyfactscompare.co.uk will never contact you by phone to sell you any financial product. Any calls like this are not from Moneyfacts. Emails sent by Moneyfactscompare.co.uk will always be from news@moneyfacts-news.co.uk. Be ScamSmart.

Moneyfactscompare.co.uk will never contact you by phone to sell you any financial product. Any calls like this are not from Moneyfacts. Emails sent by Moneyfactscompare.co.uk will always be from news@moneyfacts-news.co.uk. Be ScamSmart.

Moneyfactscompare.co.uk will never contact you by phone to sell you any financial product. Any calls like this are not from Moneyfacts. Emails sent by Moneyfactscompare.co.uk will always be from news@moneyfacts-news.co.uk. Be ScamSmart.