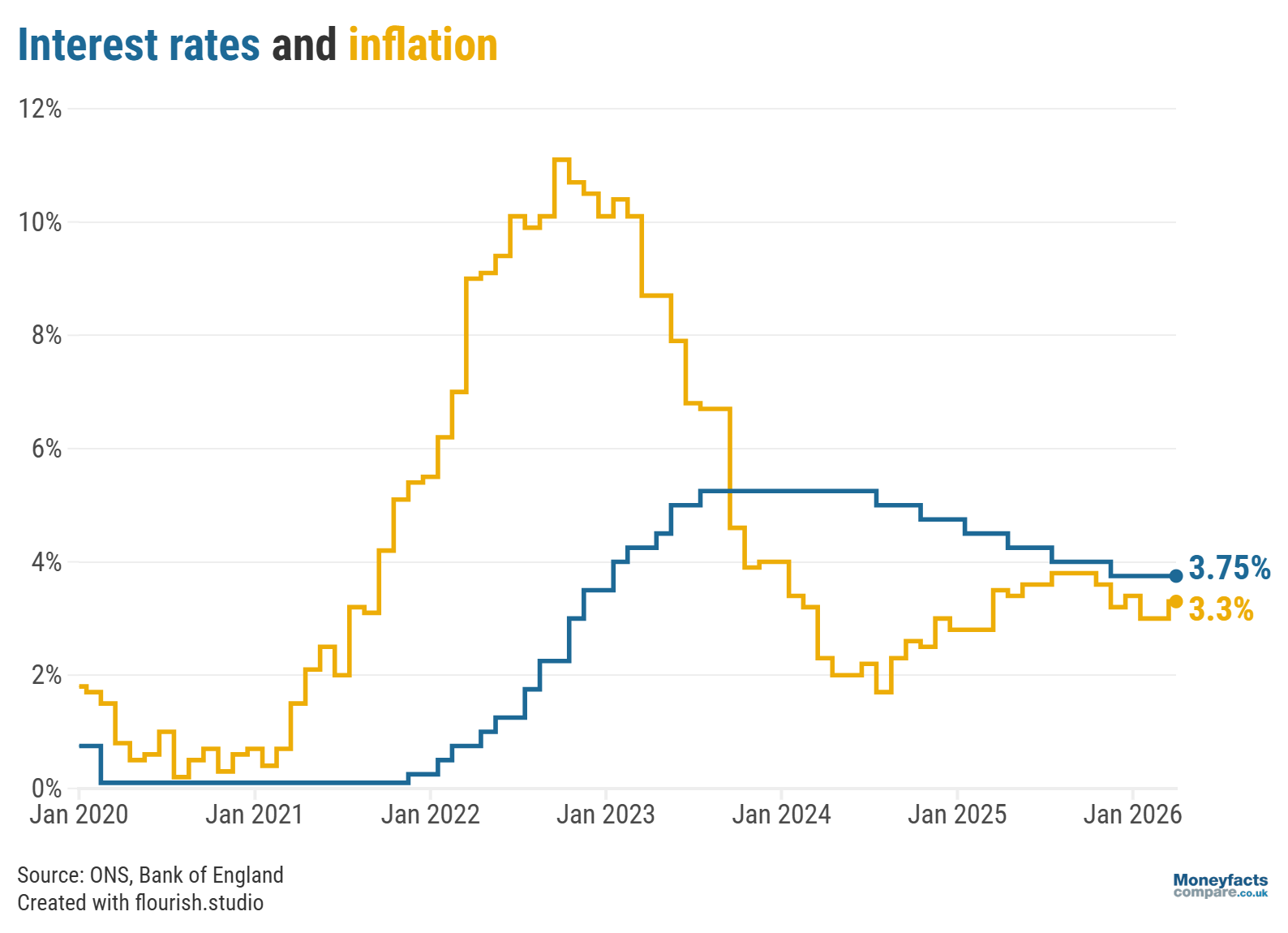

The Bank seems to be adopting a “wait and see” approach.

As the UK starts to feel the effects of the conflict in the Middle East, the Bank of England’s Monetary Policy Committee (MPC) announced that it had voted 8 to 1 in favour of maintaining the base rate at 3.75%. Many experts had predicted this outcome after the unanimous vote to hold it in March, and after Andrew Bailey, Governor of the Bank of England, said they wouldn’t be rushing any decisions.

The International Monetary Fund (IMF) recently cautioned central banks against making any hasty increases to interest rates, and the Bank appears to have taken note of this warning. Although inflation rose to 3.3% in March and is expected to climb even higher over the coming months, there is still a lot of uncertainty over how global events will affect the UK which could make the Bank cautious about raising the base rate.

However, it may feel forced to take action later in the year, depending on how long the conflict persists and how seriously it impacts inflation and other areas of the economy.

UK Finance Trends: The Bank of England base rate vs the rate of inflation between 2020 and April 2026.

The base rate is the UK’s central interest rate, which determines how much banks, building societies and other providers are charged to borrow money from the Bank of England. It is used as a tool to help control inflation in the UK or stimulate growth, depending on the state of the economy.

This affects consumers as the base rate influences the rate that lenders charge on mortgages and other forms of credit, as well as the interest that providers pay on their savings products. Read more on the base rate and what it means for your money.

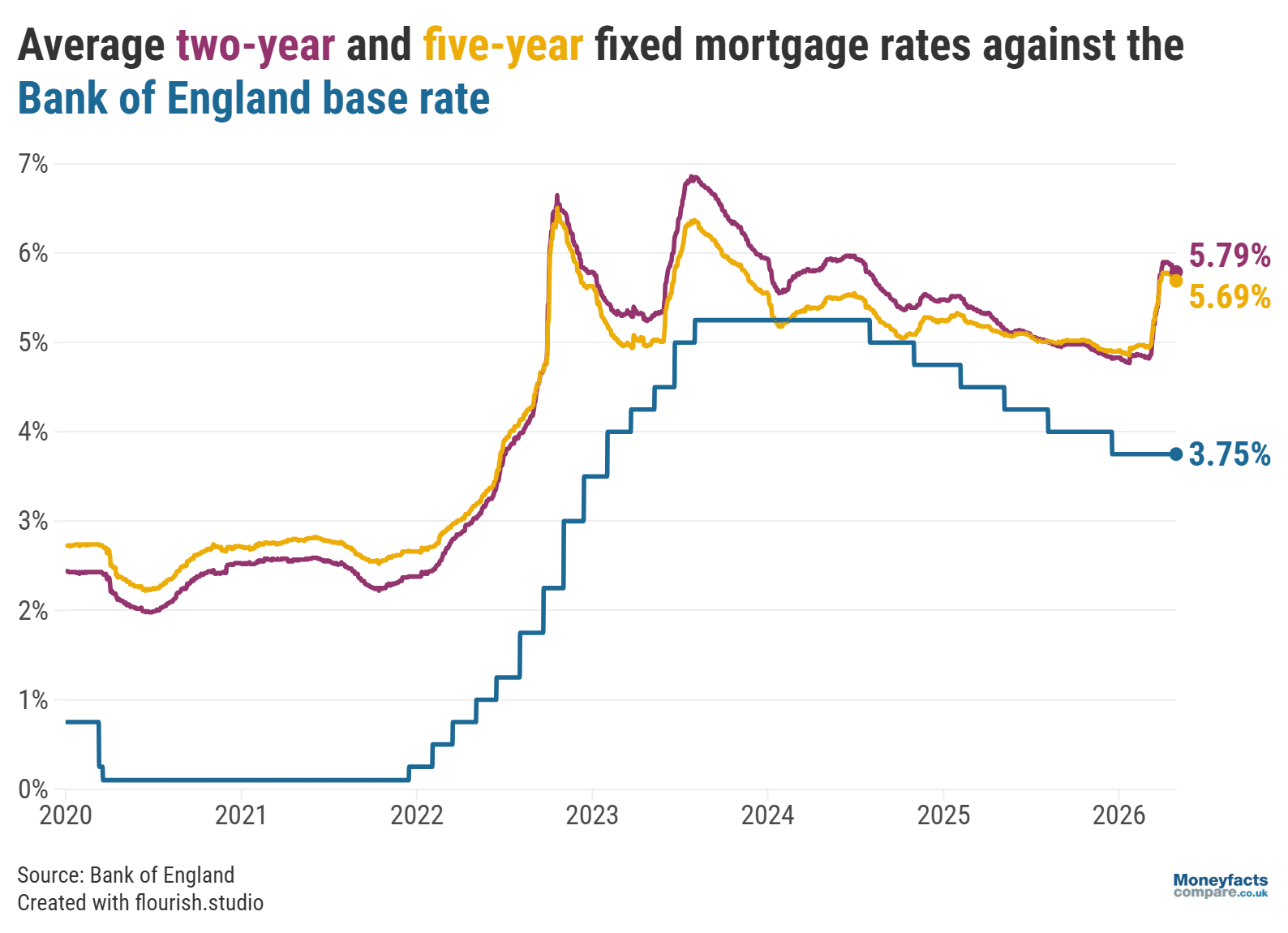

Expectations that the base rate will remain higher for longer prompted mortgage lenders to hike rates in the weeks following the outbreak of the conflict in the Middle East. As a result, the Moneyfacts Average Mortgage Rate rose from 4.90% to 5.72% between the start of March and the start of April, its largest monthly rise since July 2023.

While the pace of increases has eased, with several major lenders even reducing rates over the past couple of weeks, the market remains volatile.

UK Mortgage Trends: The average two- and five-year fixed mortgage rates between 2022 and April 2026, against the Bank of England base rate.

“Borrowers have been left in limbo as it is difficult to know whether they should rush to lock into a fixed deal or wait and see if lenders make more sizeable cuts,” Rachel Springall, Finance Expert at Moneyfactscompare.co.uk, noted.

She adds that, even though borrowers will be hoping that the “mortgage mayhem” seen in recent weeks will calm down, a rise in monthly payments will be inevitable for most borrowers coming off a cheap fix. Nevertheless, Springall calculated that borrowers could still save almost £2,500 a year by moving from an expensive revert rate to a two-year fixed deal.*

“The past couple of months have been a stark reminder that the mortgage market is vulnerable to global shocks, and the future direction of interest rates is never guaranteed. Even if conditions improve, it could still be some time before we see a substantial drop in rates,” Oliver Dack, Spokesperson at Mortgage Advice Bureau, commented.

“In the meantime, borrowers should take stock of their current circumstances and act accordingly. Crucially, those coming to the end of a fixed term mustn’t delay finding a new deal or they risk sleepwalking onto an expensive Standard Variable Rate,” he urged.

Whether borrowers are ready to remortgage, are planning to move house or are hoping to buy their first home, it may be wise to seek advice from a mortgage broker for more support in navigating the market and finding a suitable deal.

MAB is the preferred mortgage broker of Moneyfactscompare.co.uk

![]()

Get friendly, expert advice free of charge as a visitor of Moneyfactscompare.co.uk

Mortgage Advice Bureau have 1,600 UK advisers with 200 awards between them.

Speak to an award-winning mortgage broker today.

Call 0800 031 8553 or request a callback

Mortgage Advice Bureau offers fee free mortgage advice for Moneyfactscompare.co.uk visitors that call on 0800 031 8553. If you contact Mortgage Advice Bureau outside of these channels you may incur a fee of up to 1%. Lines are open Monday to Friday 8am to 8pm and Saturday 9am to 1pm excluding bank holidays. Calls may be recorded.

Your home may be repossessed if you do not keep up repayments on your mortgage.

Want to discover today’s top mortgage rates? Our mortgage charts are updated throughout the day to show the latest range of deals available on the market.

However, it’s important to note that the mortgages with the lowest rates won’t necessarily be the best option for all borrowers. This is why our weekly mortgage roundup highlights some alternative “Moneyfacts Best Buy” options that may be worth considering based on their overall cost and value, in addition to the deals charging the lowest rates.

The hold to the Bank of England base rate, and the quickly diminishing chances of any cuts this year, may be welcomed by savers as this could lead savings rates to remain more competitive for longer.

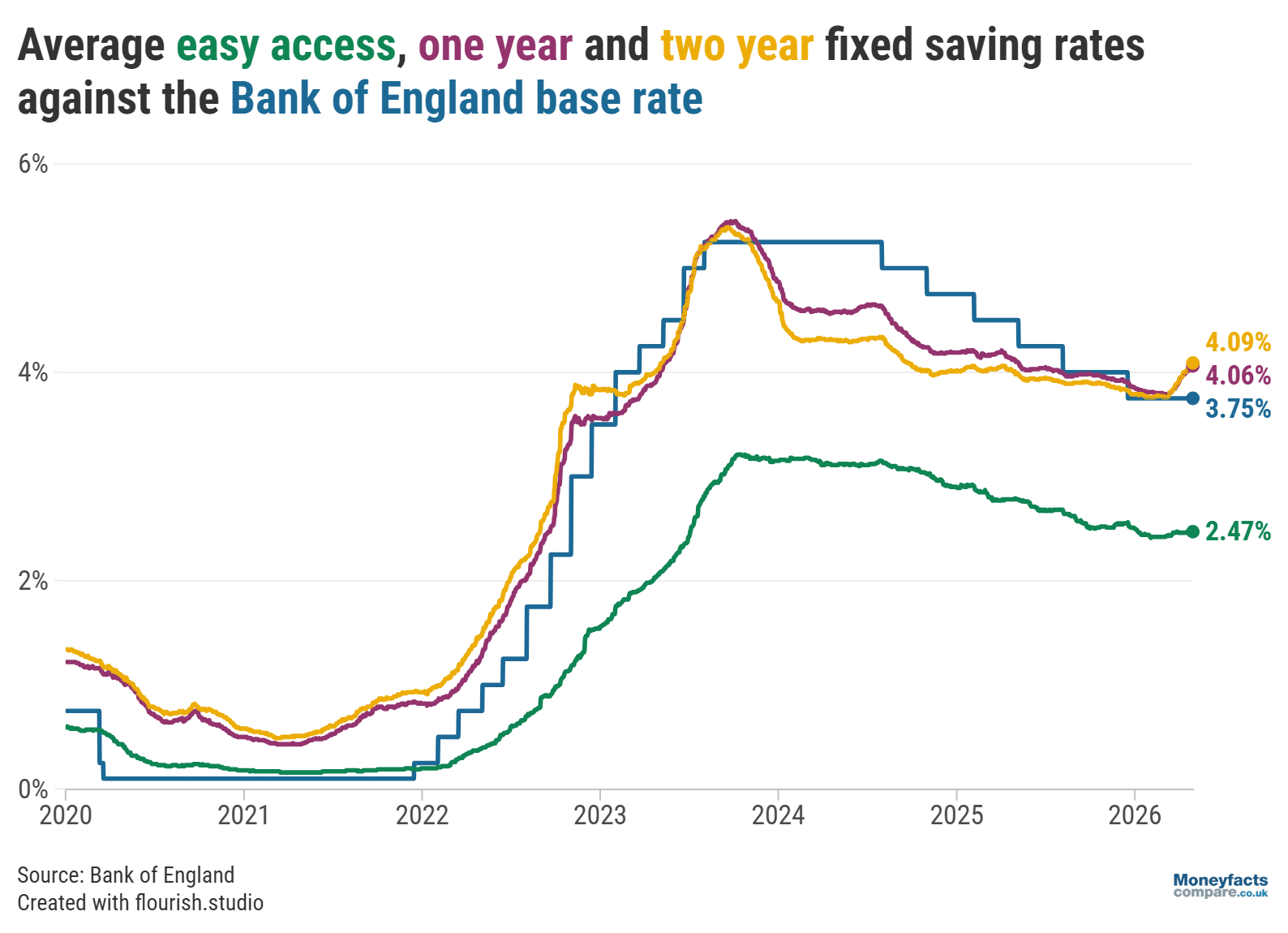

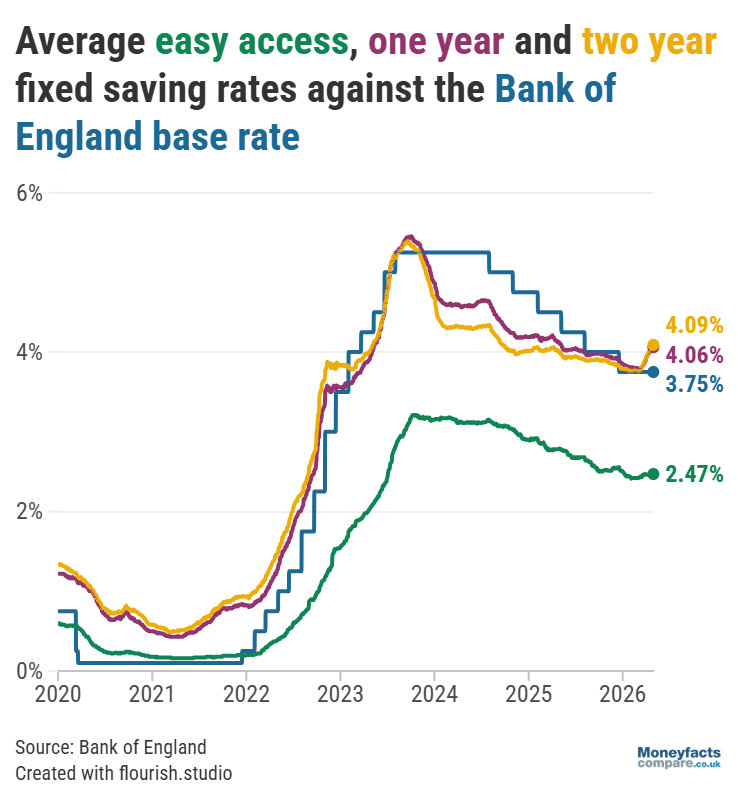

Many of the average savings rates improved between the start of March and April, with the Moneyfacts Average Savings Rate recording its largest month-on-month rise since September 2023 as it increased from 3.32% to 3.40%.

Fixed savings and fixed ISA rates saw particularly attractive rises, as the average one-year fixed savings rate increased from 3.79% to 3.91% while the average one-year fixed ISA rate soared from 3.76% to 4.01%.

UK Savings Trends: The average easy access, one-year and two-year fixed savings rates between 2020 and April 2026, against the Bank of England base rate.

However, to benefit from these higher rates, savers need to be proactive about switching accounts. Indeed, Springall warned that savers “must escape the apathy trap” and “should not hesitate to chase down a better deal”, especially as the risk of rising prices threatens to eat away at the purchasing power of our money.

This is particularly significant for those who have money sitting in a closed savings account (one which is no longer available to new customers), as these typically pay lower interest rates than accounts that are still on sale.

For example, the average rate on easy access savings accounts that could be opened at the start of April 2026 stood at 2.47% AER, compared to an average of 2.39% AER paid on closed accounts. For easy access ISAs, the difference between open and closed accounts was even more stark, standing at 2.75% AER and 2.49% AER respectively.

“Savers who have their nest egg in a closed account could be missing out on more than they realise, and they could see the real value of their cash diminish should inflation spike. However, they could hold out for longer with real returns by proactively switching to on sale accounts, offered by providers who breathe life into the savings market,” Springall explained.

“Apathy is dangerous when it comes to maximising interest returns, so savers need to feel inspired to shop around to take advantage of top rates,” she concluded.

If you haven’t reviewed your savings or switched accounts recently, you may be missing out on the potential of higher returns. Around half of UK savings accounts currently pay above the current base rate of 3.75% so, to see if you could earn a more competitive rate on your money, compare the latest rates on our savings charts.

Or, to stay up to date with the latest changes in the savings market, you can read our weekly ISA roundup and savings roundup or subscribe to our free Savers Friend newsletter.

* Average standard variable rate (SVR) is currently 7.13%. Calculations based on a £250,000 mortgage over a 25-year term on a repayment basis. SVR repayment £1,787 per month, versus £1,581 per month on 5.81% two-year fixed rate, monthly difference of £206, which is £2,472 over 12 months.

All of our newsletters are available free by email to all Moneyfactscompare.co.uk users.

Send me Weekend Moneyfactscompare, Savers Friend, and Companies Friend.

Information is correct as of the date of publication (shown at the top of this article). Any products featured may be withdrawn by their provider or changed at any time. Links to third parties on this page are paid for by the third party. You can find out more about the individual products by visiting their site. Moneyfactscompare.co.uk will receive a small payment if you use their services after you click through to their site. All information is subject to change without notice. Please check all terms before making any decisions. This information is intended solely to provide guidance and is not financial advice. Moneyfacts will not be liable for any loss arising from your use or reliance on this information. If you are in any doubt, Moneyfacts recommends you obtain independent financial advice.

Moneyfactscompare.co.uk will never contact you by phone to sell you any financial product. Any calls like this are not from Moneyfacts. Emails sent by Moneyfactscompare.co.uk will always be from news@moneyfacts-news.co.uk. Be ScamSmart.

Moneyfactscompare.co.uk will never contact you by phone to sell you any financial product. Any calls like this are not from Moneyfacts. Emails sent by Moneyfactscompare.co.uk will always be from news@moneyfacts-news.co.uk. Be ScamSmart.

Moneyfactscompare.co.uk will never contact you by phone to sell you any financial product. Any calls like this are not from Moneyfacts. Emails sent by Moneyfactscompare.co.uk will always be from news@moneyfacts-news.co.uk. Be ScamSmart.

Moneyfactscompare.co.uk will never contact you by phone to sell you any financial product. Any calls like this are not from Moneyfacts. Emails sent by Moneyfactscompare.co.uk will always be from news@moneyfacts-news.co.uk. Be ScamSmart.

Moneyfactscompare.co.uk will never contact you by phone to sell you any financial product. Any calls like this are not from Moneyfacts. Emails sent by Moneyfactscompare.co.uk will always be from news@moneyfacts-news.co.uk. Be ScamSmart.

Moneyfactscompare.co.uk will never contact you by phone to sell you any financial product. Any calls like this are not from Moneyfacts. Emails sent by Moneyfactscompare.co.uk will always be from news@moneyfacts-news.co.uk. Be ScamSmart.