How could this affect the Bank of England’s next steps?

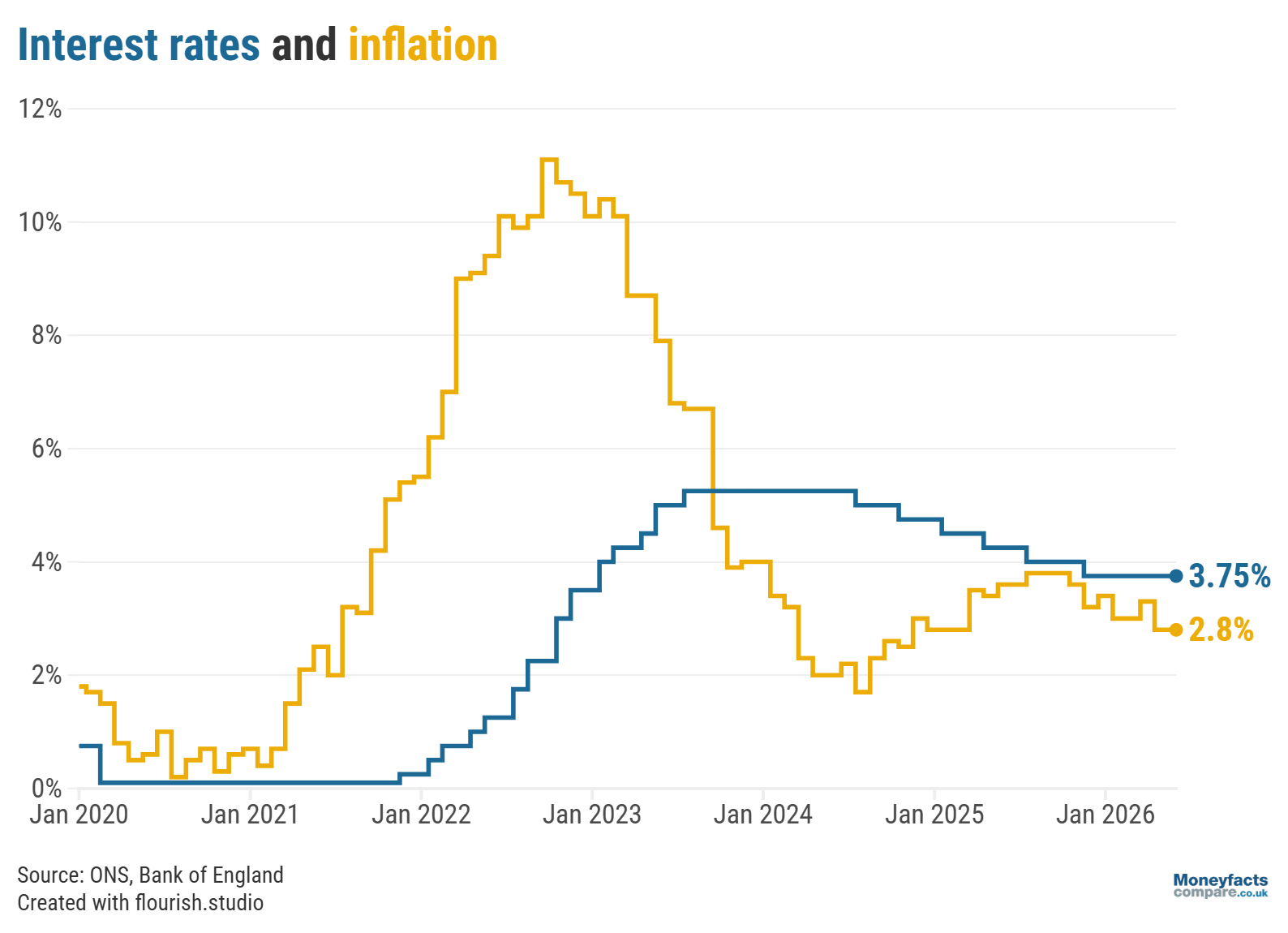

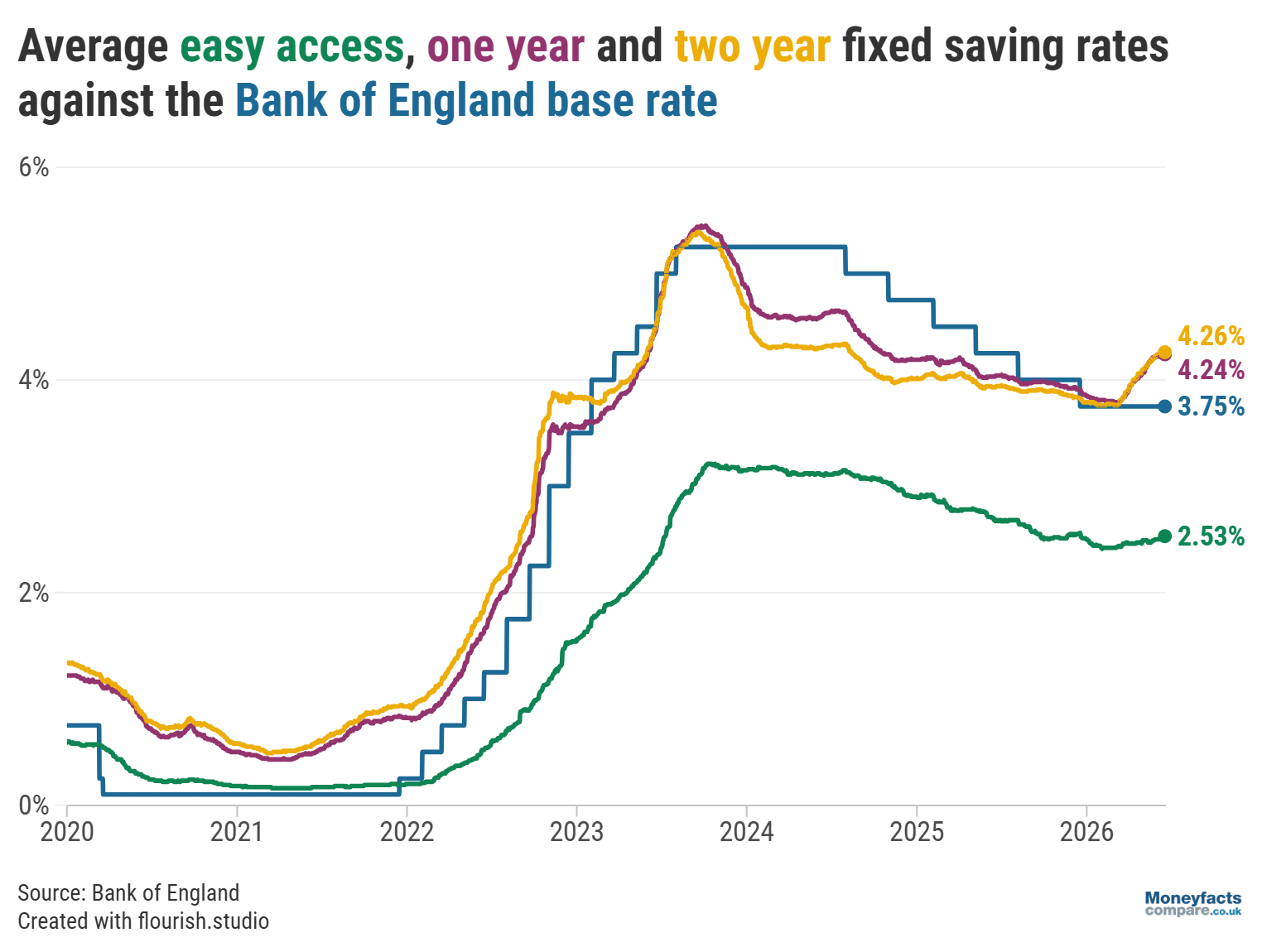

With a majority of 7 to 2, the Bank of England’s Monetary Policy Committee (MPC) voted to hold the base rate at 3.75% at its latest meeting.

The UK’s central interest rate has been at this level since December 2025 and, although the European Central Bank recently decided to raise its interest rate for the first time in almost three years, the nine-person MPC decided not to follow suit.

This outcome was widely predicted, especially after the latest figures from the Office for National Statistics (ONS) showed that the annual rate of inflation stayed at 2.8% in May. The conflict in the Middle East was initially expected to push up the cost of living but, so far, the figures indicate that prices have risen at a slower pace than forecast.

UK Finance Trends: The Bank of England base rate vs the rate of inflation between 2020 and June 2026.

However, even though the US and Iran have now signed an initial peace deal which could bring an end to the war in the Middle East, the fallout from recent global events may still affect the UK over the coming months. It seems likely that inflation will continue to rise in 2026, particularly due to higher energy prices, which means a base rate hike later in the year isn’t off the table.

But, at the moment, it seems the MPC doesn’t yet think it necessary to take action. The Bank of England will closely monitor events in the UK and further afield when making future decisions about the central interest rate, trying to strike a balance between curbing inflation and stimulating economic growth.

The base rate is the UK’s central interest rate set by the Bank of England and is used as a tool to influence spending. It affects how much it costs banks, building societies and other providers to borrow money, as well as how much interest they earn on any money held with the Bank.

This affects consumers because the base rate is a crucial factor that determines the interest rate providers pay on your savings and the interest they charge on mortgages, for example. Find out more about what the base rate means for your money.

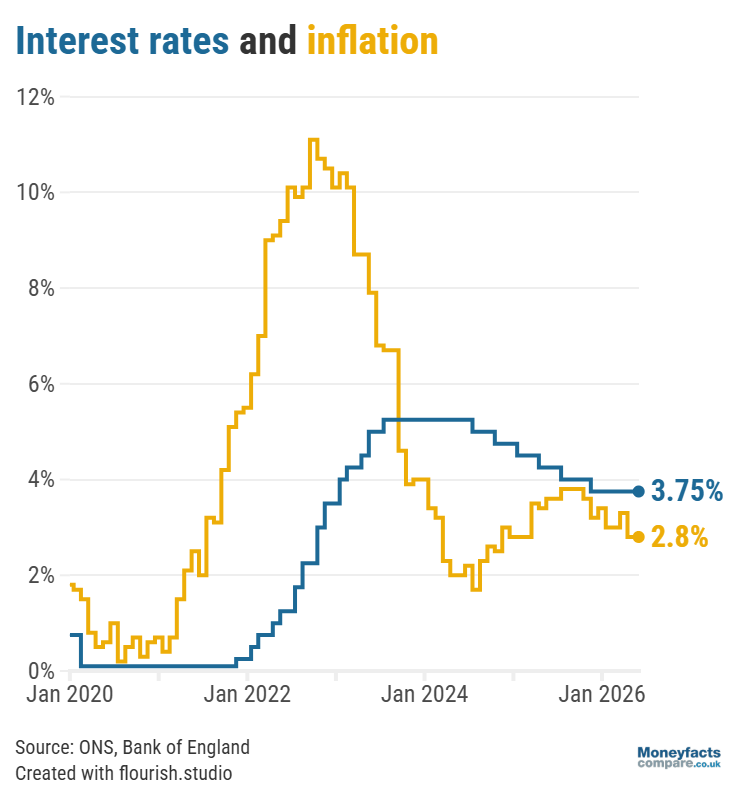

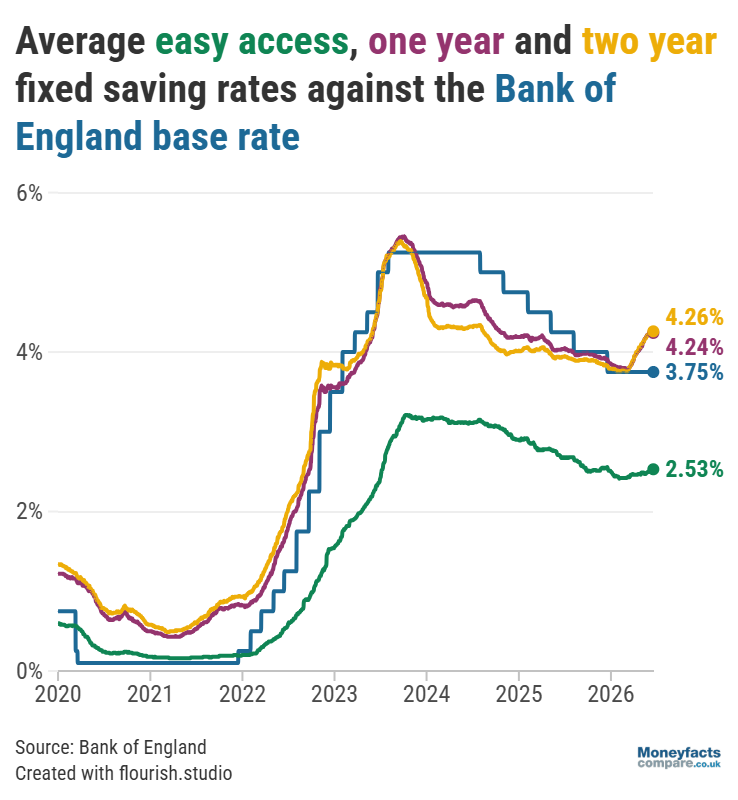

While the base rate has remained unchanged for around six months, savers have benefited from more competitive options as many savings providers have increased returns on their accounts. As a result, the Moneyfacts Average Savings Rate has risen to 3.57%, its highest point since May 2025.

This trend is particularly evident in the fixed bond market, with the average one-year fixed savings rate rising from 3.79% in March 2026 to 4.24%, whereas the typical easy access savings rate increased from just 2.42% to 2.53% over the same period.

“Much of this change to fixed rates is down to speculation that interest rates will remain higher for longer, and providers working hard to draw in funds,” Rachel Springall, Finance Expert at Moneyfactscompare.co.uk, explained.

UK Savings Trends: The average easy access, one-year and two-year fixed savings rates between 2020 and June 2026, against the Bank of England base rate.

However, savers will only benefit from these competitive rates if they actively review their existing accounts and move to a different provider if they can get a better return elsewhere.

“You can’t blame savers for feeling apathetic, but it’s important to review rates every six months or so at the bare minimum,” Springall urged.

“Savers blinded by loyalty or failing to check their easy access accounts regularly could be earning a paltry rate. Even if savers have a small amount saved, a pot out of sight means it is out of mind,” she added.

Moreover, Springall points out that challenger banks and building societies are often the providers that offer the best returns on the market.

“Convenience comes at a cost, so savers who keep their pots with a high street bank, or even in a current account, are not making their money work as hard as it could,” she warned.

There is a range of competitive savings accounts, including easy access options and fixed rate bonds, that can offer an attractive return on your money; see the latest interest rates on our savings charts. Or, if you want to earn a tax-free return on your money, find out today’s top ISA rates.

You can also stay up to date with the latest developments in the savings and ISA markets with our weekly Savers Friend newsletter.

The peace talks between the US and Iran may be welcomed by those looking to remortgage or buy a home in the near future, as they may hope that predictions of higher interest rates won’t materialise.

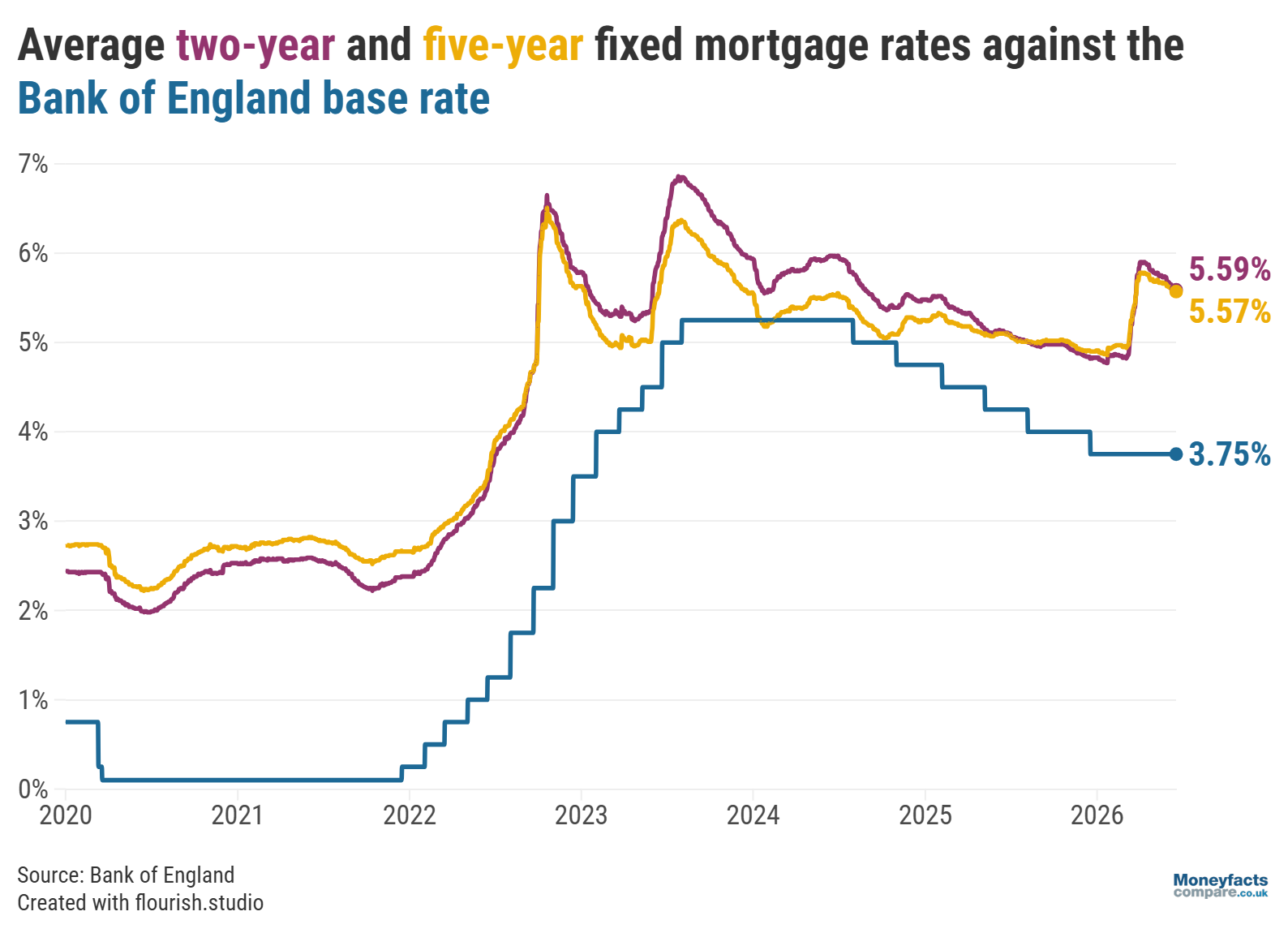

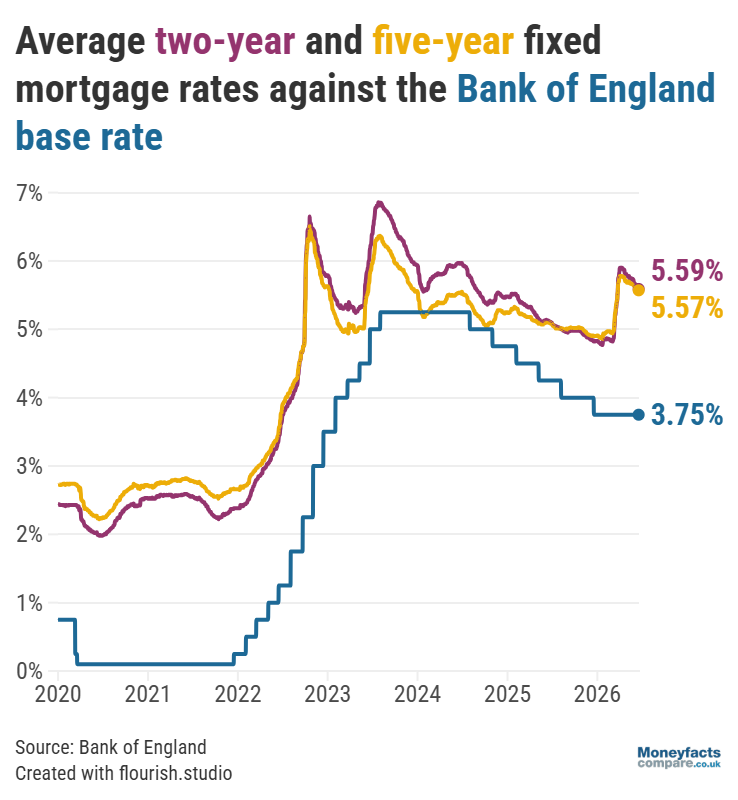

Mortgage lenders hiked rates in the weeks following the outbreak of conflict in the Middle East but, after peaking in April, fixed mortgage rates have since declined (although they remain higher than at the start of March).

“While there was no change to the base rate today, it seems that some lenders have been taking proactive steps to price their products more sensibly following a knee-jerk reaction to recent global events,” Oliver Dack, Spokesperson at Mortgage Advice Bureau, commented.

This is likely to be “encouraging news for borrowers”, but Dack cautions that those coming to the end of a fixed term who are tempted to wait for rates to fall before locking into a new deal may find “that this could take some time and there are never any guarantees”.

Indeed, Springall points out that a lot could change as “economists expect global markets to remain unsettled”.

“It is highly unlikely that lenders will make substantial cuts in the months ahead until there is a clearer path for future rate setting. The cost of living is expected to worsen in the coming months which puts pressure on the Monetary Policy Committee at the Bank of England to consider a rate increase,” she explained.

UK Mortgage Trends: The average two- and five-year fixed mortgage rates from 2020 to June 2026 against the Bank of England base rate.

But, although the future path of the mortgage market is far from certain, “indecisiveness could be the biggest enemy for borrowers this year”, Springall warned.

“New buyers who hesitate to make the leap onto the property ladder could get hit by higher repayments”, she explained, calculating that a 0.25% increase to the base rate could see mortgage payments rise by around £450 per year. Based on a £250,000 mortgage with a 25-year term, assuming the typical rate rises from 5.50% to 5.75%.

Meanwhile, homeowners who are about to remortgage may want to consider locking into a new fixed deal three to six months before their existing mortgage ends, either with their current lender or a new lender.

Even though borrowers coming off a cheaper fix may be unenthusiastic about locking into a more expensive deal, Springall calculates that this could save them around £2,800 than if they reverted to their lender’s Standard Variable Rate (SVR)*.

MAB is the preferred mortgage broker of Moneyfactscompare.co.uk

![]()

Get friendly, expert advice free of charge as a visitor of Moneyfactscompare.co.uk

Mortgage Advice Bureau have 1,600 UK advisers with 200 awards between them.

Speak to an award-winning mortgage broker today.

Call 0800 031 8553 or request a callback

Mortgage Advice Bureau offers fee free mortgage advice for Moneyfactscompare.co.uk visitors that call on 0800 031 8553. If you contact Mortgage Advice Bureau outside of these channels you may incur a fee of up to 1%. Lines are open Monday to Friday 8am to 8pm and Saturday 9am to 1pm excluding bank holidays. Calls may be recorded.

Your home may be repossessed if you do not keep up repayments on your mortgage.

Whether you’re looking to remortgage, move house or buy your first home, our mortgage charts are updated throughout the day to show the latest rates currently available.

But bear in mind those deals with the lowest rates may not always be the most suitable option or provide the best value. Our weekly mortgage roundup highlights deals that feature as Moneyfacts Best Buys based on their overall “true” cost, in addition to those products that charge the lowest rates.

* Average standard variable rate (SVR) is currently 7.13%. Calculations based on a £250,000 mortgage over a 25-year term on a repayment basis. SVR repayment £1,787 per month, versus £1,553 per month on 5.62% two-year fixed rate, monthly difference of £234, which is £2,808 over 12 months.

All of our newsletters are available free by email to all Moneyfactscompare.co.uk users.

Send me Weekend Moneyfactscompare, Savers Friend, and Companies Friend.

Information is correct as of the date of publication (shown at the top of this article). Any products featured may be withdrawn by their provider or changed at any time. Links to third parties on this page are paid for by the third party. You can find out more about the individual products by visiting their site. Moneyfactscompare.co.uk will receive a small payment if you use their services after you click through to their site. All information is subject to change without notice. Please check all terms before making any decisions. This information is intended solely to provide guidance and is not financial advice. Moneyfacts will not be liable for any loss arising from your use or reliance on this information. If you are in any doubt, Moneyfacts recommends you obtain independent financial advice.

Moneyfactscompare.co.uk will never contact you by phone to sell you any financial product. Any calls like this are not from Moneyfacts. Emails sent by Moneyfactscompare.co.uk will always be from news@moneyfacts-news.co.uk. Be ScamSmart.

Moneyfactscompare.co.uk will never contact you by phone to sell you any financial product. Any calls like this are not from Moneyfacts. Emails sent by Moneyfactscompare.co.uk will always be from news@moneyfacts-news.co.uk. Be ScamSmart.

Moneyfactscompare.co.uk will never contact you by phone to sell you any financial product. Any calls like this are not from Moneyfacts. Emails sent by Moneyfactscompare.co.uk will always be from news@moneyfacts-news.co.uk. Be ScamSmart.

Moneyfactscompare.co.uk will never contact you by phone to sell you any financial product. Any calls like this are not from Moneyfacts. Emails sent by Moneyfactscompare.co.uk will always be from news@moneyfacts-news.co.uk. Be ScamSmart.

Moneyfactscompare.co.uk will never contact you by phone to sell you any financial product. Any calls like this are not from Moneyfacts. Emails sent by Moneyfactscompare.co.uk will always be from news@moneyfacts-news.co.uk. Be ScamSmart.

Moneyfactscompare.co.uk will never contact you by phone to sell you any financial product. Any calls like this are not from Moneyfacts. Emails sent by Moneyfactscompare.co.uk will always be from news@moneyfacts-news.co.uk. Be ScamSmart.